Related Insights

New York Fed President John Williams signalled that the Fed will likely keep rates unchanged at the January 28 FOMC meeting. He argued that the latest rate cuts have brought risks back into better balance with monetary policy closer to neutral. He did not expect a rapid deterioration in the labour market, which he saw stabilizing and strengthening, as 2026 growth runs above trend at 2.5-2.75%. Williams also estimated that tariffs would add about 0.5% to inflation, peaking in the first half of this year before easing back toward the 2% target.

Attention also shifted to Fed leadership succession. US President Donald Trump said he was done with interviews and has someone in mind to replace Fed Chair Jerome Powell when his term ends in May. Former Fed Governor Kevin Warsh has emerged as the clear frontrunner after Trump expressed a preference to keep Kevin Hassett in his current role as National Economic Council Director. Warsh is considered easier to confirm by the Senate because he is not viewed as part of Trump’s inner circle and seen as institutionally orthodox. The January 2026 subpoenas of Powell sparked a backlash, with some Republican senators, including Thom Tillis and Lisa Murkowski, threatening to block any nominee until the situation was resolved. Warsh is viewed as the candidate best suited to "de-escalate" these tensions because of his reputation for protecting the Fed's traditional autonomy. The Supreme Court’s hearing on Fed Governor Lisa Cook underscored the importance of the Fed’s independence by expressing deep concerns over granting the President unchecked powers to remove Fed officials.

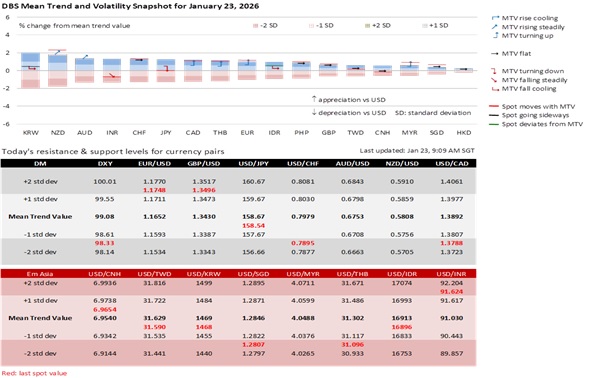

USD/CNY rose for a second day by 0.1% to 6.9708 on Thursday, hinting that the CNY’s appreciation over the past 1-2 months may lose momentum. According to a Xinhua news interview, People’s Bank of China Governor Pan Gongsheng reiterated that monetary policy will remain accommodative in 2026, downplaying the recent inflation uptick as temporary. Policy will remain focused on supporting growth and ensuring ample liquidity through further interest rate cuts and reductions in the reserve requirement ratio, while maintaining the exchange rate at a “basically stable” level and guarding against overshooting risks.

AUD/USD surged by 0.8% to 0.6814 on Wednesday, its highest closing level since early October 2025. Markets see a divergence in the dual mandates, with the Reserve Bank of Australia more focused on inflation, and the Fed alert to labour market risks. The futures market is pricing a 58.9% probability of a 25-bps RBA hike to 3.85% at the February 3 meeting. Australia’s unemployment rate fell to 4.1% in December, defying expectations for it to hold at November’s 4.3% level. On January 28, CPI and trimmed mean inflation are expected to remain elevated at 3.3% YoY in December, above the medium-term inflation target band of 2-3%. Real GDP growth expanded above 2% for the first time in two years, with domestic demand contributing 1.1% out of the 2.1% growth in 3Q25.

Yesterday’s 0.4% decline in the DXY Index reflected an unwinding of the geopolitical risk premium about escalation risks around Greenland. Attention will likely shift back to the Fed, where guidance points to a January hold with policy closer to neutral. Greater clarity on Fed leadership succession has reduced near-term risk about its independence. Against this backdrop, we are cautious about the market’s bet that the appreciation momentum of the AUD and CNY will continue unbated.

Quote of the Day

“The saddest aspect of life right now is that science gathers knowledge faster than society gathers wisdom.”

Isaac Asimov

January 23 in history

The first successful treatment with insulin was given to a diabetic in 1922.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.