Related Insights

- Malaysia: BNM stood pat; preserving monetary ammunition in 2026 23 Jan 2026

- Focus returns to the Fed 23 Jan 2026

- Xiaomi Corp23 Jan 2026

Across Asia, fiscal trajectories are becoming an increasingly important driver of rates performance and FX outcomes. China is best positioned to outperform the region on a total return basis, as fiscal expansion remains measured, monetary policy retains flexibility, and external balances continue to improve. In contrast, several regional peers face rising fiscal slippage risks alongside weaker currencies.

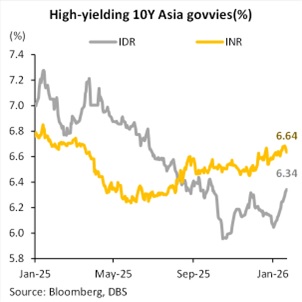

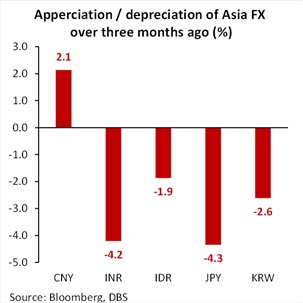

Fiscal concerns in India are re-emerging (see: India’s Budget to align with strategic objectives). Net tax receipts are missing budget estimates, while expenditure compression is still underway. Ongoing CAPEX investment in infrastructure and strategic sectors is calling for further bond issuance. These factors are keeping yields biased higher despite easing headline inflation. At the same time, FX depreciation risks are rising amid tariff-related uncertainties and a stronger USD backdrop. While the RBI has turned dovish, it remains reluctant to deliver outright rate cuts. This combination is capping bond total returns. Likewise, Indonesia’s fiscal risks are gaining attention (see: Indonesia markets: Domestic catalysts strengthen bearish pressure on rupiah). Its deficit trajectory is moving closer to the statutory 3% budget cap. Although Bank Indonesia arguably has room to stay dovish to accommodate fiscal expansion, IDR depreciation is likely to stall the pace of rate cuts. Beyond fiscal considerations, concerns over Bank Indonesia’s policy independence are also weighing on exchange rate performance.

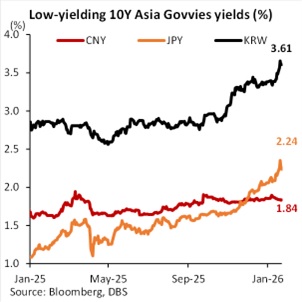

North Asian government bonds are not immune from the same risks. In Korea, the government is leaning toward fiscal expansion. A supplementary budget for 2025 has already been implemented, and a record-high 2026 budget of KRW 728tn (+8.1% YoY versus the initial plan) has been approved. The net fiscal deficit is projected to widen to 4.0% of GDP from 2.8%. That said, monetary policy flexibility remains constrained. A weak KRW, combined with elevated property and equity valuations, leaves the Bank of Korea little room to cut rates aggressively. Despite some stabilization after the initial sell-off, Japan is still facing renewed fiscal expansion risks following political turnover and snap election dynamics.

In contrast, China’s fiscal expansion remains moderate. Incremental investment is focusing on AI and advanced manufacturing, which are less capex-intensive than past property or infrastructure cycles. Credit demand stays weak amid anti-involution campaign, which aims at curbing excessive investment and production. On the monetary policy front, the PBOC is likely to stay on course with its easing stance until PPI returns to positive territory. The RMB is also strengthening, supported by strong trade performance. China has achieved trade surpluses exceeding USD 1tn for two consecutive years despite tightening trade tensions. Taken together, these dynamics underpin China’s superior total return outlook relative to the rest of Asia.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related Insights

- Malaysia: BNM stood pat; preserving monetary ammunition in 2026 23 Jan 2026

- Focus returns to the Fed 23 Jan 2026

- Xiaomi Corp23 Jan 2026

Related Insights

- Malaysia: BNM stood pat; preserving monetary ammunition in 2026 23 Jan 2026

- Focus returns to the Fed 23 Jan 2026

- Xiaomi Corp23 Jan 2026