Related Insights

- Research Library13 Jul 2026

- Taiwan: AI cycle and 2H outlook13 Jul 2026

- Bracing for Warsh’s hearings and US CPI data13 Jul 2026

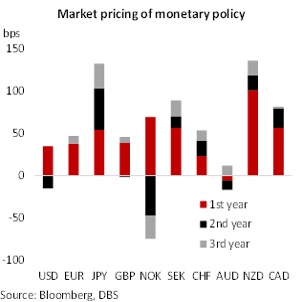

Within the G10, the BOJ and RBNZ are the two laggards that are likely to maintain a hawkish stance beyond their counterparts. This could significant impact from an RV perspective across rates and FX. The RBNZ hiked for the first time in this cycle last week to 2.50%. The economy had been facing considerable headwinds and there was a need to drive policy setting below neutral. Expectations are now building that the further normalization is needed, especially with the cash rate neutral widely expected to be closer to 3%. if so, the hike path for the RBNZ is clearer than the other G10 central banks who have maintained a more hawkish stance. Some curve flattening for the NZD curve is likely.

Ditto for Japan. The BOJ has maintained a slow pace of tightening. However, between persistent yen weakness and an outsized 7% YoY spike in PPI, Finance Minister Katayama has become more assertive in her comments. In particular, there are indications that the GPIF may tweak the portfolio allocation more heavily towards domestic assets. This implies greater repatriation flows and at the least, new monies are more likely to be deployed into domestic assets. Accordingly, JPY assets may be outperform. From a JGB / rates perspective, investors may finally draw some comfort that long-end JGB yields are very attractive in absolute terms. Between further BOJ hikes and demand for long-end JGBs, curve flattening is likely.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.

Related Insights

- Research Library13 Jul 2026

- Taiwan: AI cycle and 2H outlook13 Jul 2026

- Bracing for Warsh’s hearings and US CPI data13 Jul 2026

Related Insights

- Research Library13 Jul 2026

- Taiwan: AI cycle and 2H outlook13 Jul 2026

- Bracing for Warsh’s hearings and US CPI data13 Jul 2026