Related Insights

- Research Library13 Jul 2026

- Taiwan: AI cycle and 2H outlook13 Jul 2026

- DM Rates: Flattening the JGB & NZGB curves13 Jul 2026

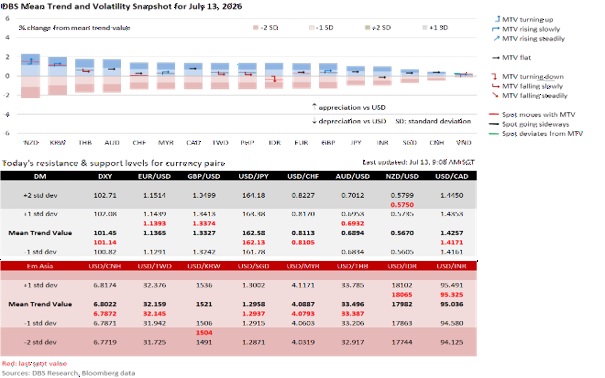

The DXY Index has been trapped between 100.5 and 102 for three weeks, awaiting more clarity on whether the Fed will proceed with the potential rate hike it flagged at the June FOMC meeting later this year.

Fed Chairman Kevin Warsh’s congressional hearings this week are shaping up as a clash between the Fed’s new operating philosophy and Congress’s mandate for oversight. He will first testify to the House Financial Services Committee on July 14, and next to the Senate Banking Committee on July 15.

At the June 16-17 FOMC meeting, Warsh pivoted away from forward guidance by radically shortening the FOMC statement, stripping out the Committee’s previous easing bias and language detailing the balance of risks. Warsh also refused to provide his personal projections for interest rates in the dots, and trajectories for GDP growth, PCE inflation, and the unemployment rate in the Summary of Economic Projections. Despite 9 of the 18 Fed participants predicting at least one hike in 2026, there was a notable dialling back of speeches and public comments by Fed officials after the FOMC.

Lawmakers who value transparency will be concerned that less communication inherently reduces Congress’s ability to review, understand, and check the Fed’s rationale.

Warsh has assembled five external task forces to overhaul Fed operations, which lawmakers, especially Democrats, worry may make the Fed less accountable to Congress and American voters. If a task force is structured as an informal or external advisory group rather than a formal federal advisory committee, it may not be subject to the Federal Advisory Committee Act (FACA). They are not legally required to hold open meetings, take public minutes, or make their internal emails and draft documents available to Congress. Public officials can be removed if they fail the public, but private advisers are insulated from consequences. Fed Governors must be vetted and confirmed by the Senate. These task force members were hand-picked by Warsh. Lawmakers never had the chance to question them under oath about their conflicts of interest before they took the role.

In the end, markets will likely separate political theatre from trading. They are unlikely to lose as much sleep over constitutional mandates as they do the terminal rate and the timing of the next rate move. Markets had given Warsh the benefit of the doubt because of his remark that the Fed has the capability and commitment to return inflation to the 2% target.

Yet, President Trump has made it very clear that he expects Warsh to support his pro-growth agenda. At the European Central Forum in Sintra on July 1, Warsh stated that inflation expectations and inflation risks had come down in recent weeks. Democrats worry that, by launching 9- to 12-month task-force reviews, Warsh is stalling to avoid raising rates before the November midterms.

Hence, markets will focus on Warsh’s reaction to the June CPI data on July 14. Headline inflation is widely expected to decline by 0.1% MoM in June, contrasting sharply from May’s 0.5% rise, due to the plunge in oil prices back to pre-war levels. However, the real test will likely be core inflation, which is expected to remain sticky and unchanged at the same 0.2% MoM (2.9% YoY) level as the previous month. Warsh must prove that his elimination of forward guidance was not a political smokescreen to keep rates unchanged but rather a strategic pivot to restore the Fed’s data-dependent agility.

Quote of the Day

“The ball is round, the game lasts ninety minutes, and everything else is just theory.”

Sepp Herberger

July 13 in history

The first-ever FIFA World Cup kicked off in 1930 in Uruguay, which also won the tournament by beating Argentina 4-2 in the finals.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.

Related Insights

- Research Library13 Jul 2026

- Taiwan: AI cycle and 2H outlook13 Jul 2026

- DM Rates: Flattening the JGB & NZGB curves13 Jul 2026

Related Insights

- Research Library13 Jul 2026

- Taiwan: AI cycle and 2H outlook13 Jul 2026

- DM Rates: Flattening the JGB & NZGB curves13 Jul 2026