Related insights_tr

Expect volatility into today’s US nonfarm payrolls which Bloomberg consensus expects will slow to 300k in August from 528k in July. Upside surprises are possible because initial jobless claims fell to 232k in the 27 August week; consensus had expected a rise to 248k from 237k (revised from 243k). On a 4-week moving average basis, claims slowed to 241.5k in August from 247.5k in July. The ISM manufacturing employment index also turned positive in August (54.2 actual vs 49.5 consensus) for the first month since April. However, services employment accounts for most of NFP. Regardless of its relevance, the revamped ADP Employment did surprise on the downside in August (132k actual vs 232k consensus). Hence, we cannot rule out downside surprises too. If NFP disappoints, this could prompt speculators to take profits on their long USD positions. It remains to be seen if USD/JPY will end the week above 140. Next week will be about the central meetings in Canada, UK, and the Eurozone. The US CPI will come a fortnight later, on 13 September.

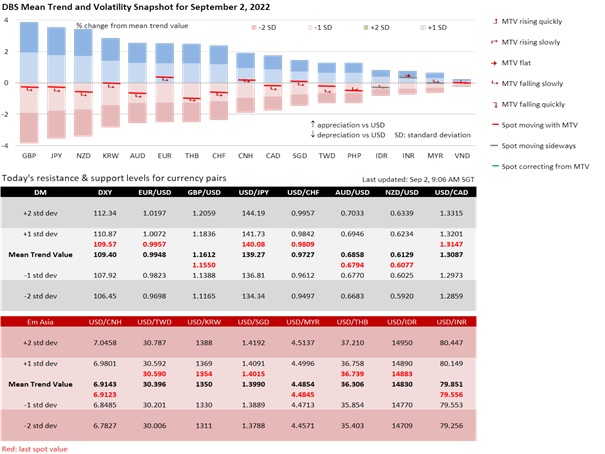

DXY appreciated 0.8% from last Friday to 109.67, its highest close since June 2002. DXY hit an intra-session high of just below 110 on the positive ISM manufacturing employment index taking the US Treasury 2Y yield to a high of almost 3.55%. However, the 2Y yield returned below 3.51% on the ISM manufacturing prices paid index plunging from 60 in July to 52.5 in August, its weakest level since June 2020. Apart from nonfarm payrolls, the US CPI data will also determine if the Fed hikes by 50 or 75 bps at the FOMC meeting on 21 September.

GBP rebounded to 1.1545 after touching 1.1499 near the lowest close (1.1485) during the Covid-19 outbreak in March 2020. GBP is more vulnerable to USD strength because of UK’s weak economic outlook and political-policy uncertainties. Bloomberg Consensus has pencilled a mild technical recession in 4Q22-1Q23, in line with the Bank of England’s guidance. The Queen will swear in the new British Prime Minister on 6 September. As per Politico’s Poll of Polls, Foreign Secretary Liz Truss is leading former Chancellor Rishi Sunak 57% to 31%. Ironically, many consider Sunak a better bet than Truss at wooing the public at the next general elections. Also, more than 60% of Tory members prefer Boris Johnson to Truss or Sunak. Assuming Truss becomes prime minister, observers believe she is too weak not to call a general election. Lawmakers are likely to resist her proposed tax cuts to support the economy on inflationary grounds and her push to review the BOE’s mandate, seen by some as a move to blame the central bank for the cost-of-living crisis.

BOE Governor Andrew Bailey will defend the central bank’s independence when he testifies to the Parliament’s Treasury Committee on 7 September. Bailey will be accompanied by Chief Economist Huw Pill, members Catherine Mann and Silvana Tenreyro. With UK CPI inflation hitting a 40-year high of 10.1% YoY in July, markets expect the BOE to deliver a second 50 bps hike to 2.25% at its meeting on 15 September. After all, the mild US technical recession in 1H22 (worse than the consensus expected for the UK in 4Q22-1Q23) did not prevent the Fed from delivering outsized hikes totalling 225 bps in March-July. Gilt yields rose faster than US Treasuries this week; 2Y rose 26.4 bps to 3.08% and 10Y by 27.7 bps to 2.88%. GBP has priced in a lot of bad news, begging the question if it deserves to head into uncharted territory below 1.15.

Quote of the day

“Beware of false knowledge; it is more dangerous than ignorance.”

George Bernard Shaw

2 September in history

US Congress established the US Treasury in 1789.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.