Related Insights

- Asia ex-Japan Equities02 Feb 2026

- Research Library02 Feb 2026

- PepsiCo 02 Feb 2026

We are not reading too much into the market’s reaction on the final session of January, following US President Donald Trump’s nomination of Kevin Warsh as the next Fed Chair, when Jerome Powell’s term ends on May 15. The sharp 9% sell-off in gold on January 31 came after a spectacular 30% rally earlier in the month, while the DXY Index rebounded 1.7% after falling nearly 4% over January 19-27. In both cases, the moves look more like position-driven profit-taking than the start of a durable trend reversal.

The Fed’s independence remains in question, with Kevin Warsh likely to face a challenging Senate confirmation process. Republican Senator Thom Tillis has vowed to oppose any Fed Chair nomination until the Department of Justice’s legal case against Powell is fully and transparently resolved. Centrist Republicans are uneasy over Trump’s attempts to gain influence over the Fed through four out of the seven Fed Governors. The three governors that markets see aligned with the President are Christoper Waller (one of Trump’s finalists for Powell’s job), Michele Bowman (a critic of Fed overreach), and Stephen Miran (Chairman of the Council of Economic Advisers). Powell is expected to serve out the remainder of his term as Governor until January 31, 2028, limiting scope for an immediate shift in Board control even after his Chair term ends on May 15. Miran will likely give up his seat after Warsh is confirmed.

Although the regional Fed Presidents were confirmed in December, control of the Board of Governors remains the critical battleground, one that goes beyond interest rate decisions. Warsh and Treasury Secretary Scott Bessent are advocating for reform of the Fed that would rein in the Fed’s expanded regulatory role, promote closer coordination with the Treasury, and increase executive influence over monetary conditions. Their argument that a smaller Fed balance sheet would allow interest rates to fall without fuelling inflation implicitly elevates price stability over employment, narrowing the Fed’s dual mandate in practice. Rather than removing political risk, Trump’s nomination of Warsh keeps it firmly in play. With Fed independence still in question, the credibility of future monetary policy remains vulnerable, leaving the USD biased lower, not stabilised.

AUD: Reassessing its upside potential

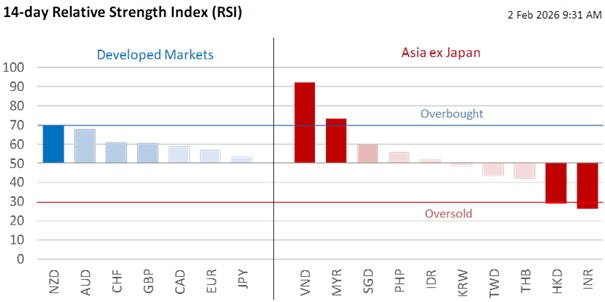

AUD was the second best-performing currency in January, gaining 4.4% against the USD. Apart from USD weakness, the AUD also strengthened on expectations (70% odds) for a 25-bps hike to 3.85% at the Reserve Bank of Australia meeting on February 3, at a time when other central banks are likely to stand pat at their first meeting of the year. CPI inflation has rebounded from 1.9% YoY in June to 3.8% YoY in December, reopening a public debate. The blame for higher inflation is falling more on fiscal policy than on monetary policy.

RBA Governor Michele Bullock is likely to characterise monetary policy as restrictive and frame Tuesday’s hike as an insurance move, rather than a series of hikes, to ensure that inflation returns to the 2-3% target range. The RBA will likely revise up 2026 GDP growth to more than 2% in its Statement of Monetary Policy, up from 1.9% in November. Markets are reassessing the AUD’s upside potential after it tested the 0.70 resistance level for the first time in three years.

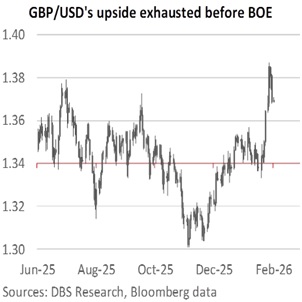

GBP: Rally paused ahead of BOE

GBP/USD should hold a dovish bias within a 1.36-1.3730 range this week. The pair corrected lower to 1.3686 last Friday after USD weakness drove a four-day rally from 1.34 to 1.3850 over January 22-27.

Focus should return to the Bank of England meeting on February 5, where the bank rate is expected to remain unchanged at 3.75%, near the estimated neutral rate range of 3.25-3.50%. Following the 25-bps cut in December, BOE Governor Andrew Bailey cautioned that future easing decisions would be closer calls and data-dependent. Nonetheless, the OIS market sees the next cut in April, driven by the BOE’s guidance that inflation will decline to the 2% target in April-May, from 3.4% YoY in December.

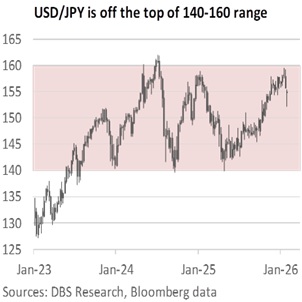

JPY: Can the LDP win a standalone majority?

A victory by Japanese Prime Minister Sanae Takaichi at the February 8 snap election no longer automatically signals JPY weakness, nor does defeat guarantee a sustained rally. USD/JPY’s sharp retreat from 160 has been driven less by Japanese politics than by fears of FX intervention – with or without US cooperation – and by growing unease over USD debasement as President Trump openly favours a weaker greenback.

Takaichi has pledged to resign if the Liberal Democratic Party-led coalition fails to secure a majority at the February 8 snap election. Opinion polls show the LDP regaining a standalone majority, with at least 233 out of 465 seats in the Lower House of Representatives. Although voters are sceptical about Takaichi’s fiscal stimulus addressing cost-of-living issues, they are receptive to her proposal to cut or suspend the consumption tax on food, her tougher stance on immigration, and her national security posture against China. Despite the formation of a Central Reform Alliance, voters are unconvinced that the opposition is united enough to govern or deliver a coherent economic programme. Going by how USD/JPY rose after the LDP lost its majority in the lower house election in October 2024 and the upper house in June 2025, we cannot rule out a lower USD/JPY if the LDP regains its lower house majority.

FX forecast revisions

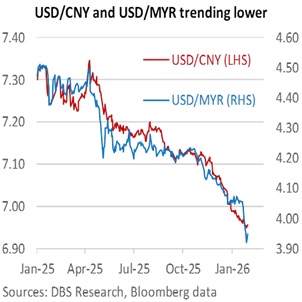

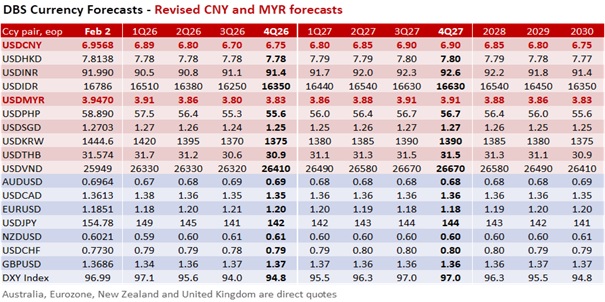

We have revised down our 3Q26 USD/CNY forecast to 6.70. The daily fixing for USD/CNY has been declining below 7.00 since January 23, when the USD sold off on US President Trump’s lack of concern over its decline, mounting unease over the threats to Fed independence, and his abrupt TACO on EU tariff threats over Greenland. Since December, when China first reported its USD1 trillion trade surplus, the onshore spot rate has consistently traded below the daily fixing, a notable break from its earlier pattern of fluctuating in the upper half of the trading band after July 2023. On February 1, Chinese President Xi Jinping also called for the CNY to become a “powerful” global currency that could be “widely used in international trade, investment and foreign exchange markets, and attain reserve currency status.”

We have lowered our 3Q26 forecast for USD/MYR to 3.80, the level it unpegged from the USD in July 2005. USD/MYR traded below 4.00 last week, for the first time since June 2018. The MYR was Asia’s top performing currency in 2025, chalking a 10.1% gain against the USD. The first episode was a relief rally, driven by America’s trade truce after Liberation Day; USD/MYR dropped from 4.50 to 4.20 in April-May, where it stayed until November. The second episode followed Malaysia’s successful hosting of the ASEAN Summit in late October, which reinforced the appeal of foreign investors and sent USD/MYR tumbling below 4.20, towards 3.90, in November-January.

Quote of the Day

“Experience is a good school. But the fees are high.”

Heinrich Heine

February 2 in history

The first Groundhog Day observed at Gobbler's Knob, Punxsutawney, Pennsylvania, in 1887.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related Insights

- Asia ex-Japan Equities02 Feb 2026

- Research Library02 Feb 2026

- PepsiCo 02 Feb 2026

Related Insights

- Asia ex-Japan Equities02 Feb 2026

- Research Library02 Feb 2026

- PepsiCo 02 Feb 2026