Related Insights

- Implications of the Venezuela Conflict 08 Jan 2026

- Research Library08 Jan 2026

- Macro Insights Portal, DEER: Credibility risks for the overvalued USD 08 Jan 2026

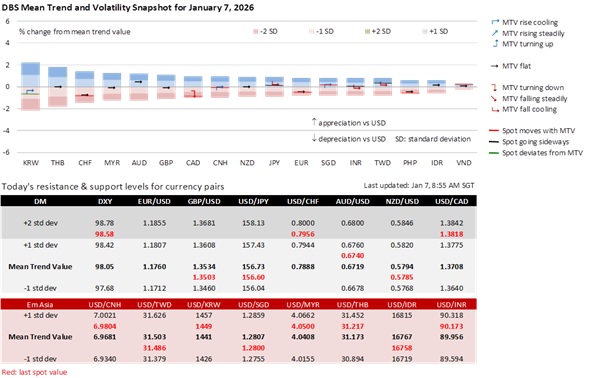

Barring a further slide in the greenback, we expect USD/SGD’s downside to be limited to around 1.2780. Per our model, the SGD NEER has already risen from the mid-point to near the ceiling of its policy band over the past 1-2 months, consistent with Singapore’s stronger-than-expected GDP growth and signs that inflation may have bottomed. The Ministry of Trade and Industry (MTI) revised up 3Q25 GDP growth from 2.9% YoY to 4.2% and reported a further growth acceleration to 5.7% in 4Q25. CPI inflation rose alongside growth and rebounded to 1.2% YoY in October-November after slowing to an average of 0.6% in 3Q25.

However, we caution against some market expectations that the Monetary Authority of Singapore (MAS) will tighten its SGD NEER policy at this month’s monetary policy review. Despite the growth rebound in 2H25, MTI maintained its 2026 GDP growth forecast at 1-3%, which the MAS expected would narrow the positive output gap to around 0% this year. In his 2026 New Year message, Prime Minister Lawrence Wong cautioned that sustaining 2025’s strong pace of growth will be challenging amid a more fragmented global economy, deeper geopolitical tensions, and structural shifts in trade and supply chains. He stressed that Singapore “cannot simply do more of the same” and must rethink, reset, and refresh its economic strategies to remain competitive. A mid-term report for the Economic Strategy Review (launched in Aug 2025) is expected around the Budget 2006 announcement scheduled for February 12. The review aims to push annual GDP growth toward the higher end of the projected 2-3% range for the next decade, with potential peaks of 4% in strong years.

On Monday, we cautioned that exchange rates are likely to be mixed than trending in January. The USD’s December sell-off was driven by monetary policy divergences in the futures/OIS markets, i.e., more Fed cuts vs. rate hikes in some Developed Market economies in 2026. However, markets also expected all central banks to stand pat at their first policy meeting this year. Until US President Donald Trump nominates a Fed Chair to succeed Powell, economic data will likely be in the driver’s seat, raising questions about asymmetric interest rate movements across countries.

For example, on Monday, weaker-than-expected US ISM data reversed the USD’s haven appeal, driven by the Trump administration’s intervention in Venezuela’s domestic politics. However, the DXY rebounded by 0.3% to 98.58 on Tuesday. EUR/USD tanked from the session’s high of 1.1743 to 1.1687 after Germany’s December CPI inflation fell below 2% again to 1.8% YoY from 2.3% in November. Today’s Eurozone CPI inflation will be closely watched for signs of Euro-Area disinflation resuming. AUD/USD’s rally stalled at 0.6740 following this morning’s lower-than-expected decline in Australia CPI inflation. During the US session, the US ADP Employment report and ISM Services employment may surprise on the upside, challenging the weak US labour market narrative that has been weighing on the greenback.

We remain mindful of the tight relationship between USD/SGD and the DXY Index, reflecting Singapore’s status as a price-taker economy. Our view remains that USD/SGD will trade in a 1.25-1.30 range in 2026, consistent with our forecast for the DXY to trade in a 95-100 range. The USD’s downside risks for 2026 remain intact, as markets brace for a potentially more dovish Fed Chair nominee under Trump, reigniting concerns over Fed independence.

Quote of the Day

“Opportunities are like sunrises. If you wait too long, you miss them.”

William Arthur Ward

January 7 in history

Brunei became the sixth member of ASEAN in 1984.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related Insights

- Implications of the Venezuela Conflict 08 Jan 2026

- Research Library08 Jan 2026

- Macro Insights Portal, DEER: Credibility risks for the overvalued USD 08 Jan 2026

Related Insights

- Implications of the Venezuela Conflict 08 Jan 2026

- Research Library08 Jan 2026

- Macro Insights Portal, DEER: Credibility risks for the overvalued USD 08 Jan 2026