- Distress amongst mainland developers has deepened with mortgage boycotts and a growth slowdown

- But additional policy support and signs of firmer prices could imply a base in home buyer demand

- Hong Kong developers may be better positioned than mainland developers to capitalize on this…

- … given their stronger financial positions, greater credibility, and lift from commercial rentals.

Related insights_tr

Opportunity amid distress in China real estate

The Chinese real estate sector is entering a phase where distress has become more prevalent. This may open up development opportunities for other non-mainland-based developers, and Hong Kong developers could be poised to benefit. This is particularly so if Chinese homebuyer demand improves amid a slew of policy support measures.

Risks deepen, but policy support steps up

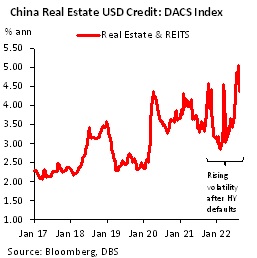

Defaults among large HY-rated developers that began in late 2021 has snowballed into a significant rise in concern over the financial health of even the largest, better rated developers. Offshore credit spreads had both risen sharply and turned more volatile. If this trend is sustained, it implies prohibitively high financing costs for even major Chinese developers.

The latest bout of offshore credit volatility was due to the emergence of mortgage boycotts. It highlights the problem of prolonged construction halts and under-finished properties to homebuyers—an unexpected fallout from developers’ liquidity crunch. While mortgage boycotts are manageable for the financial sector (see China Bank Credit: Buffers amid headwinds, 22 Jul 22), the impact on homebuyers’ confidence of project delivery has been chilling. July’s residential property sales declined by 58% (m/m), sharper than the typical seasonal weakness. Our seasonally adjusted m/m decline in July records the worst monthly outturn since 2011, excluding the month of April 2022 where sales plummeted in a one-off fashion due to the Shanghai lockdown. \

\

Despite weak sales, support is ramping up to lift demand. One, China has stepped up policy support to the housing sector to restore confidence. On 20 Aug, the authorities announced that policy banks could provide special loans to resume housing project, which reported could amount to CNY200bn. China’s 5y Loan Prime Rate was also cut by a larger than expected 15bps on 22 Aug, which should result in similar sized cuts to mortgage rates. Two, residential property primary sale pricing may already be bottoming, particularly for the Eastern region. The pace of decline has slowed noticeably since May, as lockdown restrictions ease while a reduction in down-payments since February has also stirred demand. That said, pricing in the Central region is still weak, especially compared to year ago levels. This may explain why mortgage boycotts are most prevalent in the central China provinces of Henan, Hunan, and Hubei, as homebuyers may be sitting uncomfortably on losses.

Given new policy support measures and stabilizing prices, homebuyer demand may improve. But already distressed developers may find it hard to capitalize on this if homebuyers continue to steer away from their presales due to low confidence. Elevated funding costs could also force a paring of assets.

Instead, non-mainland developers may be the one to reap benefits from a demand recovery, as they still enjoy the confidence of homebuyers and lower funding costs. Among various options, these developers could scoop up projects and land from already distressed developers at good prices, or increase their JV stakes. There is no question that mainland developers have to execute more asset sales and deleverage to regain credit market access. Furthermore, non-mainland developers could also set better prices relative to projects from riskier developers. Home buyers are likely to differentiate between riskier developers and their accompanying risks of poorly finished projects, vs financially solid developers. We think a crisis for some may well turn to be an opportunity for others.

Disparate financial positions across developers

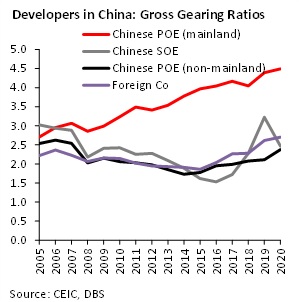

An aggregate financial analysis of mainland POE, SOE, and non-mainland POE developers reveals widely disparate financial positions. Gearing ratios (defined as liabilities to equity) are strikingly wide between mainland POE vs Hong Kong POEs, and much wider than what net debt to equity ratios indicate. The gap in gearing between mainland POEs and the others has steadily widened over the years, with their aggregate gross gearing ratio ramping up sharply from a normal 2.7 in 2005 to reach an extremely elevated 4.5 in 2020. In contrast, gearing ratios had remained stable around the usually safe 1.5 to 3.0 range for SOEs, non-mainland POEs, and also foreign developers.

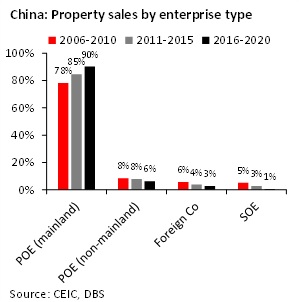

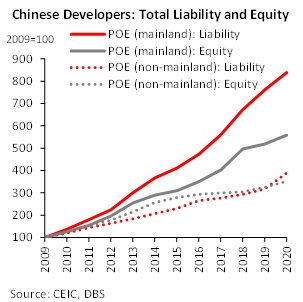

Such high gearing has been a major driver behind the sharp equity and sales growth for mainland POEs, on top of their better cost and execution efficiency. Chinese POEs successfully expanded their market share from 78% in 2006-2010 to 90% a decade later. Shareholders’ equity also jumped by a stellar 5.6 times from 2009 to 2020. In contrast, non-mainland POEs’ shareholders’ equity saw a mundane rise of 3.5 times in the same period.

But high gearing implies risks. Equity gains had been ploughed back to accumulate more debt, so liabilities for the mainland POEs climbed at an even faster pace than equity, unlike their non-mainland peers. Only with a regulatory clampdown through the “three red lines” debt limits in late 2020 were the brakes engaged. Without meaningful asset sales, such large deviations from gearing norms have proven difficult to close for mainland POEs, leading to liquidity strains, defaults, and a loss of home buyers’ and investors’ confidence that make them poorly positioned for a market recovery.

Hong Kong developers see lesser volatility

Given the precarious negative feedback loop for mainland POEs, where liquidity is impacted by sales and vice versa, it will be difficult to pick winners and losers. Media reports of potential SOE credit guarantees are likely too small to backstop the entire short-term debt of the sector, and any undercapitalized debt insurer also poses their own credit risks. We expect volatility to continue for credit of mainland POEs, without a broader debt resolution.

The beneficiaries amid such liquidity worries could be the non-mainland developers with lower gearing. If Chinese homebuyers’ demand recovers on the back of policy relaxation measures, Hong Kong-based developers should have the financial wherewithal to acquire assets and expand market share.

Even in the event of a longer than expected downturn, it is an opportune time for Hong Kong developers to increase their land bank at modest costs, raise the share of their JV projects, or even take over distressed projects as a “white knight”. Most Hong Kong developers also concentrate projects and landbanks in the wealthier Eastern region. Correspondingly, they have smaller exposure across regions where local property markets are under strong adverse pressure. Given these factors, and with Hong Kong’s property market conditions also improving (see Hong Kong: Rising lending rates and credit implications, 22 Aug 22), we expect greater resilience amongst Hong Kong real estate developers.

To read the full report, click here to Download the PDF.

Topic

Explore more

E & S FlashGENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Completed Date: 29 Aug 2022 10:21:42 (SGT)

Dissemination Date: 29 Aug 2022 10:21:42 (SGT)

Sources for all charts and tables are DBS Bank unless otherwise specified

GENERAL DISCLOSURE/DISCLAIMER

This report is prepared by DBS Bank Ltd. This report is solely intended for the clients of DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd, its respective connected and associated corporations and affiliates only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii) redistributed without the prior written consent of DBS Bank Ltd.

The research set out in this report is based on information obtained from sources believed to be reliable, but we (which collectively refers to DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd, its respective connected and associated corporations, affiliates and their respective directors, officers, employees and agents (collectively, the “DBS Group”) have not conducted due diligence on any of the companies, verified any information or sources or taken into account any other factors which we may consider to be relevant or appropriate in preparing the research. Accordingly, we do not make any representation or warranty as to the accuracy, completeness or correctness of the research set out in this report. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This document is for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate independent legal or financial advice. The DBS Group accepts no liability whatsoever for any direct, indirect and/or consequential loss (including any claims for loss of profit) arising from any use of and/or reliance upon this document and/or further communication given in relation to this document. This document is not to be construed as an offer or a solicitation of an offer to buy or sell any securities. The DBS Group, along with its affiliates and/or persons associated with any of them may from time to time have interests in the securities mentioned in this document. The DBS Group, may have positions in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking services for these companies.

Any valuations, opinions, estimates, forecasts, ratings or risk assessments herein constitutes a judgment as of the date of this report, and there can be no assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk assessments. The information in this document is subject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed, it may not contain all material information concerning the company (or companies) referred to in this report and the DBS Group is under no obligation to update the information in this report.

This publication has not been reviewed or authorized by any regulatory authority in Singapore, Hong Kong or elsewhere. There is no planned schedule or frequency for updating research publication relating to any issuer.

The valuations, opinions, estimates, forecasts, ratings or risk assessments described in this report were based upon a number of estimates and assumptions and are inherently subject to significant uncertainties and contingencies. It can be expected that one or more of the estimates on which the valuations, opinions, estimates, forecasts, ratings or risk assessments were based will not materialize or will vary significantly from actual results. Therefore, the inclusion of the valuations, opinions, estimates, forecasts, ratings or risk assessments described herein IS NOT TO BE RELIED UPON as a representation and/or warranty by the DBS Group (and/or any persons associated with the aforesaid entities), that:

(a) such valuations, opinions, estimates, forecasts, ratings or risk assessments or their underlying assumptions will be achieved, and

(b) there is any assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk assessments stated therein.

Please contact the primary analyst for valuation methodologies and assumptions associated with the covered companies or price targets.

Any assumptions made in this report that refers to commodities, are for the purposes of making forecasts for the company (or companies) mentioned herein. They are not to be construed as recommendations to trade in the physical commodity or in the futures contract relating to the commodity referred to in this report.

ANALYST CERTIFICATION

The research analyst(s) primarily responsible for the content of this research report, in part or in whole, certifies that the views about the companies and their securities expressed in this report accurately reflect his/her personal views. The analyst(s) also certifies that no part of his/her compensation was, is, or will be, directly or indirectly, related to specific recommendations or views expressed in the report. The research analyst (s) primarily responsible for the content of this research report, in part or in whole, certifies that he or his associate[1] does not serve as an officer of the issuer or the new listing applicant (which includes in the case of a real estate investment trust, an officer of the management company of the real estate investment trust; and in the case of any other entity, an officer or its equivalent counterparty of the entity who is responsible for the management of the issuer or the new listing applicant) and the research analyst(s) primarily responsible for the content of this research report or his associate does not have financial interests[2] in relation to an issuer or a new listing applicant that the analyst reviews. DBS Group has procedures in place to eliminate, avoid and manage any potential conflicts of interests that may arise in connection with the production of research reports. The research analyst(s) responsible for this report operates as part of a separate and independent team to the investment banking function of the DBS Group and procedures are in place to ensure that confidential information held by either the research or investment banking function is handled appropriately. There is no direct link of DBS Group's compensation to any specific investment banking function of the DBS Group.

[1] An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

[2] Financial interest is defined as interests that are commonly known financial interest, such as investment in the securities in respect of an issuer or a new listing applicant, or financial accommodation arrangement between the issuer or the new listing applicant and the firm or analysis. This term does not include commercial lending conducted at arm's length, or investments in any collective investment scheme other than an issuer or new listing applicant notwithstanding the fact that the scheme has investments in securities in respect of an issuer or a new listing applicant.