- Tariff risks cast a shadow but monetary easing and fiscal stimulus by China would provide support

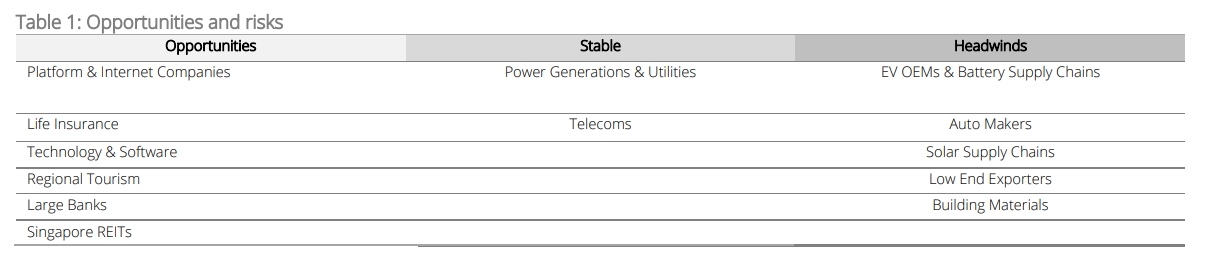

- Banks, S-REITs, technology supply chains, and tourism plays continue to be bright spots

- Falling global rates, stable corporate profitability, and steep valuation discounts support the longer-term trend

- Asia ex-Japan and China have inherent fundamentals and compelling outlooks

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

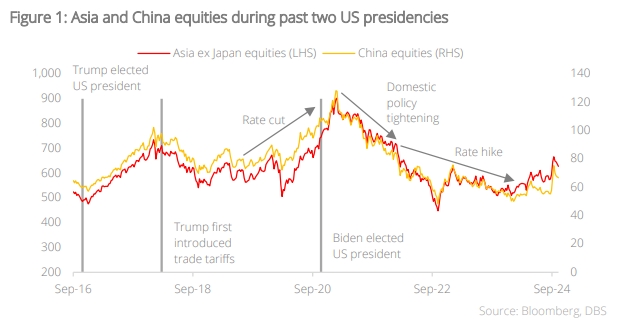

The outcome of the US presidential election has cast a shadow of uncertainty across Asia, with the Trump presidency threatening further expansion of draconian trade policies. However, trade tariffs and selective import limitations during Trump’s (2017) and Biden’s administrations showed no major bearing on the overall returns of China equities.

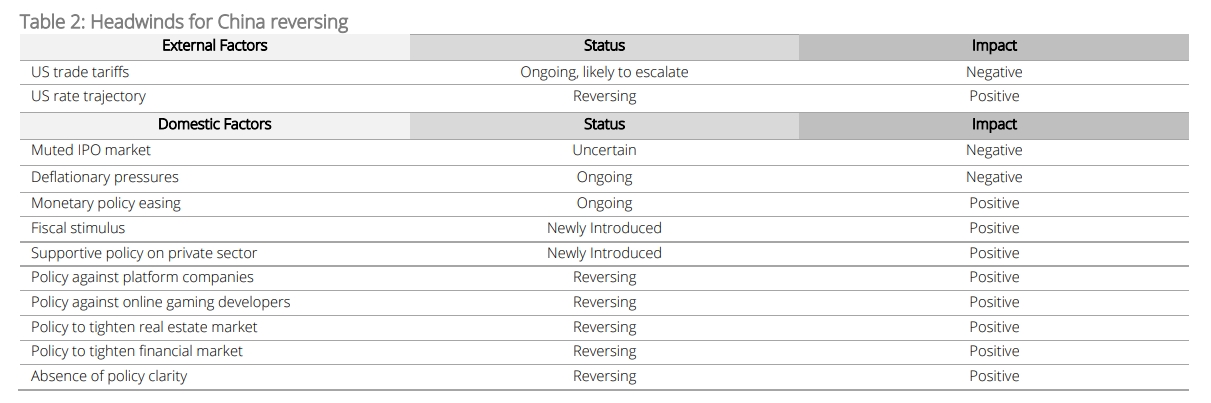

Rather, it is a combination of internal factors that have weighed more heavily on China’s equity markets since 2019. These include domestic policy tightening, the real estate sector debacle, a downturn caused by Covid lockdowns, and deflationary pressures.

While the US presidential election has created volatility within regions and trade bodies, we expect long-term dynamics to normalise over time, as with previous cycles. With the dust gradually settling over time, there presents a backdrop for better policy certainties for Asia and China going forward.

So far, the markets have been largely conditioned to expect additional tariffs or controls on exports to the US. Thanks to the continued diversification of supply chains, the impact of any new tariffs on corporate confidence is likely to be less severe.

Asia is expected to deepen regional integration and collaboration, seeking new trade ties in Europe, the Middle East and Latin America to mitigate the effects of US-China trade tensions.

Meanwhile, ASEAN is expected to benefit from further Fed easing as companies seek to diversify their supply chains in Southeast Asia amid ongoing trade tensions. This will drive further FDI flows into the region under the China+1 strategy, with China itself among the major contributors of these inflows. At the same time, ASEAN’s large domestic market is relatively more insulated from tariff risks, while lower labour costs, proximity to China, regional supply chain efficiency, and government incentives are expected to continue driving FDI into the region.

Targeted monetary easing and select fiscal support will remain major elements in supporting domestic demand and growth momentum in China. These measures are expected to uplift investor expectations. While we do not expect the region’s underweight position among global funds to reverse in the near term, the narrowing of underweight positions can deliver upside from current levels.

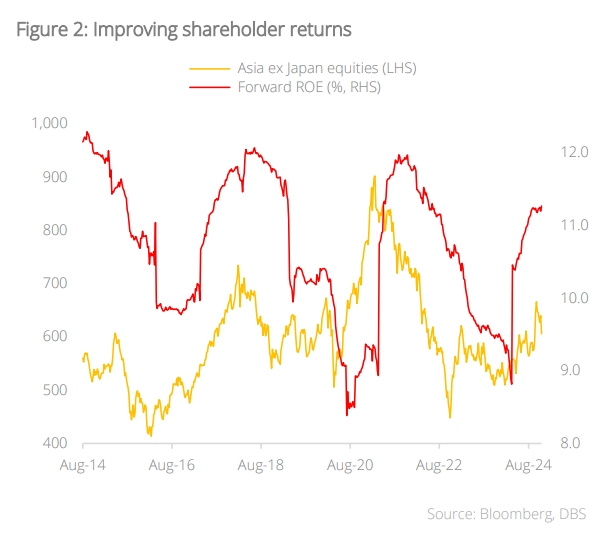

The performance of Asian assets as a whole is historically inversely correlated to global rates. With rates moving in favour of the region, there is room for the re-rating of Asian equities, which have underperformed. In particular, index heavyweights and rate-sensitive asset classes should begin outperforming.

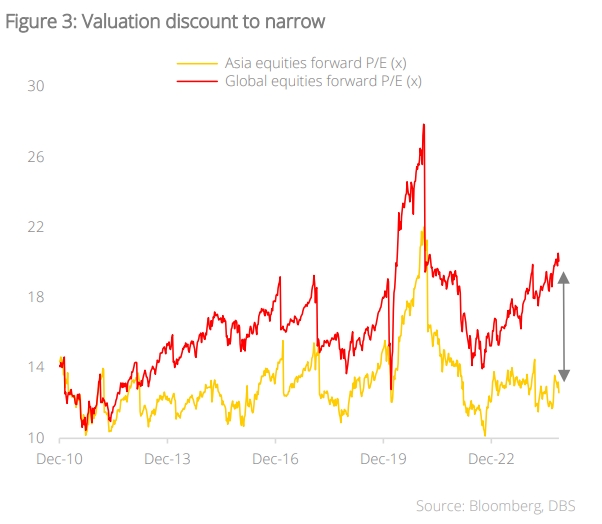

There are three tailwinds supporting the longer-term trend in AxJ:

a) Falling global rates

b) Stabilising corporate profitability

c) Steep valuation discounts

A lower interest rate environment will channel capital into high-growth markets, which positions Asia ex Japan as an attractive region for investors seeking both growth and yield. The long term narrative to stay constructive in the region remains intact.

Taking into consideration the US presidential elections and with it the possibility of new trade policies, the start of rate cutting cycles, rising trade flows within Asia, and stimulus policy initiatives by China, we have come up with a list of prevalent themes and the corresponding outlook for each one.

China

The PBOC buoyed the market in September in an unexpected move: a blitz of monetary easing measures, reductions in the reserve requirement ratio (RRR), as well as cut to policy and mortgage rates – all meant to bolster the economy and buoy a waning stock market.

Further announcements were made at the National People’s Congress (NPC) to address the long standing debt burden of local government funding vehicles (LGFV). These include a program offering CNY12tn of debt swaps, special bond issuance, and guarantees.

While the market response was muted, we expect the Chinese government to add more comprehensive measures to expedite growth. These are likely to provide a floor for valuations, offering support for the China equity market.

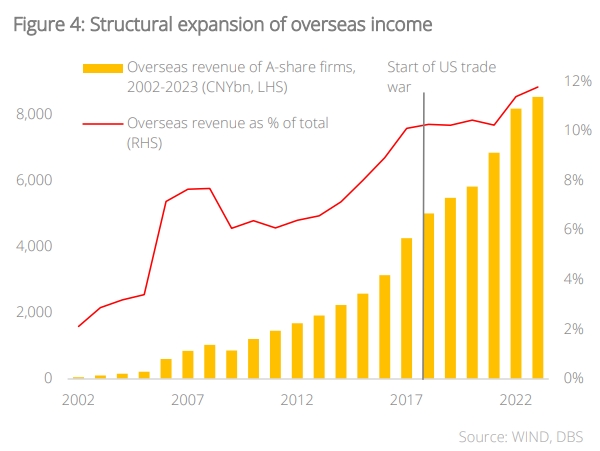

Over time, China companies have enriched their income diversity and earnings quality. For instance, overseas income rose to 12% of total contributions to revenue in 2023, from a mere 2% at the turn of the millennium. Notably, overseas income expanded further despite the start of trade tariffs in early 2018. We expect overseas contributions to continue rising as China firms enhance revenue resilience to external risks through diversifying into outward investments, securing global supply chains, localising production, and accessing emerging markets for both production efficiency and demand.

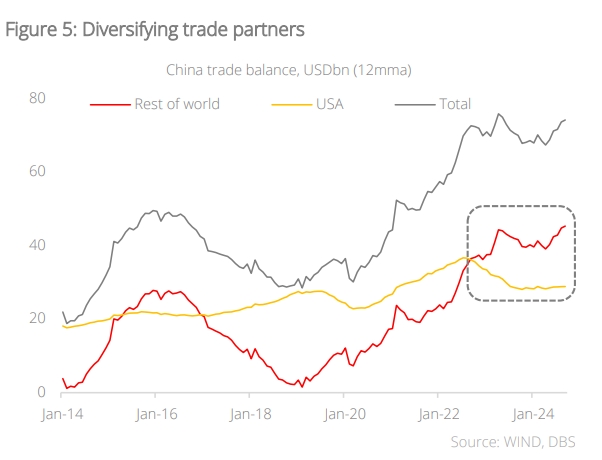

Even after the US imposed trade tariffs on China’s exports and restrictions what it can import, China has successfully diversified its trade, broadened its trade income, and reduced reliance on any single market. End 2022 marked the watershed moment when China’s trade balance with the rest of the world surpassed what it has with the US.

We advise investors to stay engaged with the markets in Asia ex Japan and China, as the inherent fundamentals and outlook are compelling.

With its recent guidance, the Chinese government has demonstrated commitment to address the longstanding LGFV debts. Ultimately, this will free up resources and provide wider policy options for local governments and financial institutions, enabling them to focus on growth, productive capital expenditure, repayment of commercial debts, salary disbursement, and improving financial strength. Such actions could provide a more stable and predictable regulatory environment, which is crucial for boosting investor confidence.

With its recent guidance, the Chinese government has demonstrated commitment to address the longstanding LGFV debts. Ultimately, this will free up resources and provide wider policy options for local governments and financial institutions, enabling them to focus on growth, productive capital expenditure, repayment of commercial debts, salary disbursement, and improving financial strength. Such actions could provide a more stable and predictable regulatory environment, which is crucial for boosting investor confidence.

Capital injections and the addressing of LGFV debts are positive developments for the banking sector as they relieve uncertainty over balance sheets, freeing up resources for more productive and concrete growth areas.

ASEAN and India overcoming US elections volatility

The ASEAN equity market is expected to adopt a cautious stance as investors await the 20 January inauguration of President Trump and any subsequent policy announcements. To provide context, while optimism surged in emerging markets, including ASEAN, following the Federal Reserve’s rate cuts and China’s stimulus plans, this enthusiasm waned after Trump’s US presidential election Notably, ASEAN markets appear to have priced in fewer interest rate cuts, particularly in light of rising yields and a strengthening dollar. This is evidenced by a climb in 10Y yields to 4.422% and the DXY index reaching 106.1, contributing to ASEAN’s underperformance relative to US markets. Despite this, ASEAN has outperformed China this year and would serve as a diversifier for exposure to the Asia market, supported by strong-performing sectors within the region. ASEAN is likely to benefit more from the China+1 strategy as supply-chain diversification becomes necessary amid increasing trade tensions. These can be played through the following key investment ideas:

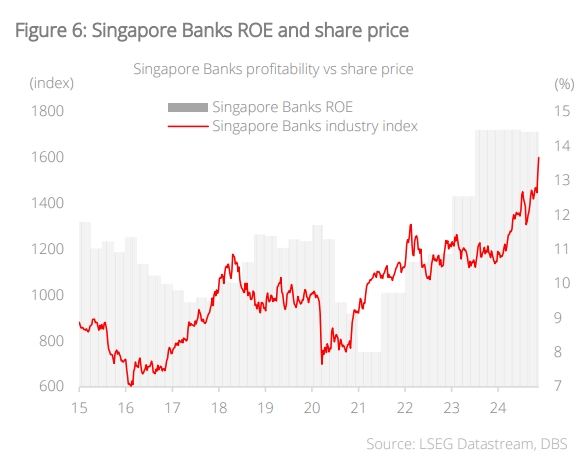

- Banks as beneficiaries of stable economies. We forecast ASEAN economies to remain stable in 2025 despite cyclical headwinds. In particular, Singapore banks should stay resilient, supported by 5% dividend yields and steady earnings growth potential. NIM could surprise on the upside with fewer rate cuts expected, and deposit rates could fall faster due to ample liquidity in the system. Strong momentum in fee income will continue as wealth activities continue to proliferate alongside improved trading and investment income. Indonesia banks continue to report steady asset quality amid improving NPL, falling credit costs, and lower liquidity-at-risk (LaR) with stable loan growth.

- S-REITs: While S-REITs experienced losses when Trump’s win drove 10Y US bond yields up to 4.4% – declining c.10% over the past month – it is worth noting that the normalisation of Fed rates remains underway. Since S-REITs typically borrow on shorter-term debt, they stand to benefit from lower interest costs, potentially supporting a gradual recovery in distribution trends. The sector is currently trading at FY25F yield in excess of 6%, preserving an attractive yield spread of around 3.5% over 10-year Singapore government bonds.

- Thailand is the only economy we forecast where growth could accelerate in 2025. Thailand’s GDP growth is projected to accelerate to 3.5% in 2025, up from 2.7% this year amid more stimulus to be announced beyond the first phase of digital wallet handouts worth THB145bn. Politics, however, are likely to be a market overhang as there are ongoing investigations into the ruling party. We continue to like beneficiaries of the China+1 phenomenon, stimulus measures, and potential rate cuts.

India opportunities arise with Trump 2.0 The Sensex recently fell to a five-month low, 10% below its record high on 26 Sep. This is amid tepid earnings, foreign investor outflows, and concerns over persistent inflationary pressures. The impact of Trump’s election victory has disrupted the market rally with a strengthening US dollar and rising bond yields. Looking ahead, more palatable valuations, robust domestic liquidity, and the possibility of the RBI cutting rates as food-driven cyclical inflation subsides present further opportunities. As a major IT outsourcing hub, India stands to gain from another Trump presidency and sustained US economic exceptionalism. Furthermore, India’s large industrial firms are likely to benefit from sustained infrastructure investments, while small- and mid-caps will benefit from digitalisation.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025