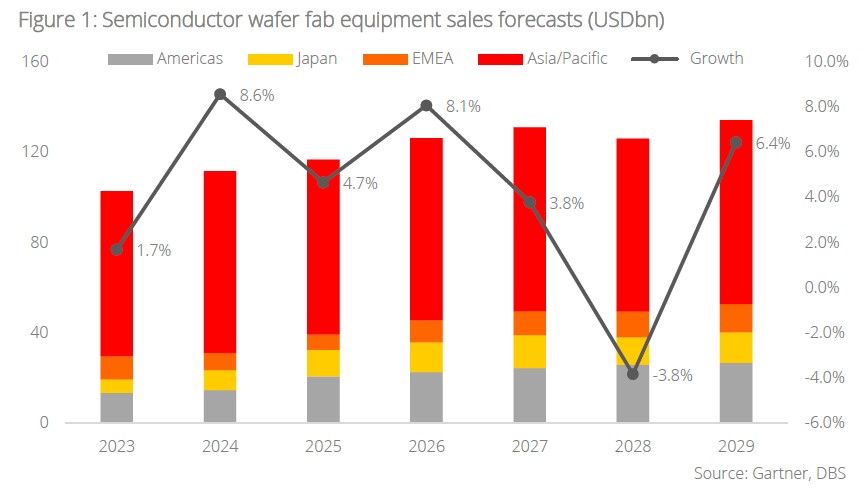

- The global semiconductor equipment maker market is projected to experience stable growth of 4.7% in 2025 and 8.1% in 2026

- Positive backdrop for equipment makers driven by reshoring efforts and global capacity expansion

- Easing US-China tensions buoyed market sentiment, especially for companies with significant exposure to China

- US policy tailwinds, including semiconductor tariffs and rollback of export restrictions on EDA, support growth in US and benefit globally diversified equipment makers

- Frontend equipment makers remain key for growth amid sustained demand for advanced nodes, while backend players are gaining momentum as market recovers

Related Insights

- FX Tactical Ideas: Momentum to Drive USD Higher26 Jun 2026

- Research Library26 Jun 2026

- USD and HKD Rates: Safe-haven demand for USD and HIBOR volatility 26 Jun 2026

WFE growth momentum set to continue. The wafer fab equipment (WFE) market recorded strong growth of 8.6% y/y, reaching USD111.6bn in 2024. This positive momentum is expected to persist into 2025 and 2026, driven primarily by continued investment in Artificial Intelligence (AI) infrastructure. While AI remains the core driver of industry growth, the broader semiconductor recovery, particularly among previously lagging segments such as backend equipment and outsourced semiconductor assembly and test (OSAT) providers, should support a more balanced and resilient industry expansion. The global semiconductor equipment maker market is hence projected to grow 4.7% in 2025 and another 8.1% in 2026.

Favourable outlook for equipment makers. The landscape for semiconductor equipment makers remains constructive, underpinned by reshoring efforts and global capacity expansion plans. Recent signs of easing US-China tensions, notably the reversal of the export ban on Nvidia’s H20 chip, have further buoyed market sentiment, especially for companies with significant exposure to China. Additionally, the newly announced 100% semiconductor tariff for exports to the US, while having 0% tariffs for those with investments in the US, is positive for equipment makers in the US as more fabs are built there. Adding to this positive momentum, the US lifted export restrictions on Electronic Design Automation (EDA) tools to Chinese customers in early July, effectively rescinding licensing requirements introduced in May. These regulatory rollbacks enhance the operating environment for globally diversified equipment players.

Frontend leads, but backend is catching up as advanced packaging becomes critical. While frontend equipment makers, which focus on early fabrication processes like lithography, deposition, and etching, remain a key growth driver amid sustained demand for advanced nodes, backend players are beginning to catch up as the market recovers. Teradyne’s 2Q25 earnings exceeded consensus expectations and its forward guidance points to a robust second half, supported by AI-driven demand for semiconductor testing. Kulicke & Soffa, another backend semiconductor company, also reported results above expectations and is anticipating a better quarter ahead. Advanced packaging is increasingly viewed as a strategic necessity, and no longer optional, with technologies like chiplets and 3D ICs becoming key enablers for AI, HPC, 5G, and edge computing. This shift has increased the importance of backend processes and positioning these companies for renewed growth.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- FX Tactical Ideas: Momentum to Drive USD Higher26 Jun 2026

- Research Library26 Jun 2026

- USD and HKD Rates: Safe-haven demand for USD and HIBOR volatility 26 Jun 2026

Related Insights

- FX Tactical Ideas: Momentum to Drive USD Higher26 Jun 2026

- Research Library26 Jun 2026

- USD and HKD Rates: Safe-haven demand for USD and HIBOR volatility 26 Jun 2026