- US: Powell’s non-committal stance makes a September Fed rate cut uncertain; weakness in labour market and continued well-behaved inflation are needed for rate cuts

- Eurozone: US and EU struck a preliminary trade deal at 15% tariffs on EU goods; eurozone 2Q GDP growth beats expectations

- India: Facing 25% tariffs, India will seek new markets, including UK, EU, and New Zealand

- ASEAN-6: We expect the bloc to see average real GDP growth of 4.8% from 2025 to 2040 with domestic and trade catalysts despite ongoing geopolitical uncertainties

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

US: FOMC’s September cut is not assured. The FOMC decision to not move on 30 Jul did not surprise us or the markets, but its forward guidance, as non-committal as it was, did. Coming into this meeting, we had expected the Fed’s messaging to move firmly toward the labour market with a clear signal that room for a September rate cut was emerging. On the contrary, the 29-30 Jul meeting’s concluding statement and Fed Chair Powell’s subsequent press conference were reflective of persistent uncertainty, along with a lack of immediacy in changing the policy stance. The Fed’s official analysis was characterised by a recognition that the US economy has shown remarkable resilience to the trade shocks thus far, with production, jobs, and prices all in well-behaved territory. Two Fed governors dissented with the July pause decision, favouring a rate cut instead, but there was a dose of political posturing associated with their votes. This remains Powell’s FOMC, Trump’s incessant pushback notwithstanding.

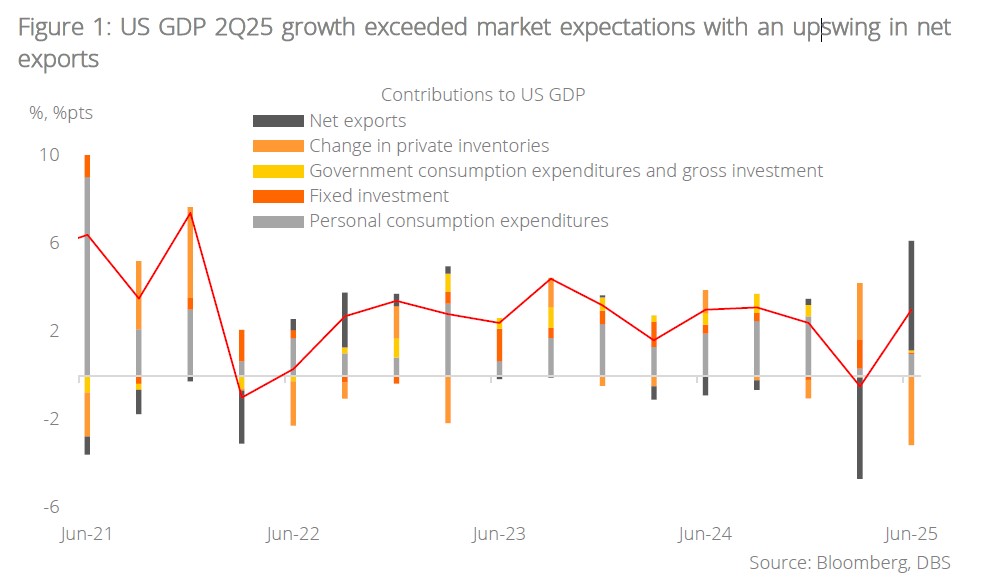

The FOMC statement reflected virtually no change in its take on the economy. The terms used to describe inflation ("somewhat elevated"), unemployment ("low"), and labour market ("solid") are the same as before. Although the upswing in net exports has led to stronger-than-expected 3% q/q sa US GDP growth in 2Q25, 1H25 growth has moderated due to a slowdown in consumer spending.

There will be a good amount of data released between now and the mid-September meeting with two more employment and two more months of inflation reports. Regarding Friday’s US jobs report, Powell emphasised that the main data to watch is unemployment rate which is expected to rise to 4.2% in July after its drop to 4.1% in June. However, markets will still be sensitive to nonfarm payrolls which is projected to decline to 104K in July from 147k in June.

Tariff-related uncertainty may not dissipate, but would likely decline somewhat by then, in our view. Odds of a policy easing in September, given Powell’s signals, are no more than 50-50. We would need to see material weakness in the labour market, along with a continuation of well-behaved inflation outturns, for the Fed to cut.

Following the finalisation of major trade deals by the 1 Aug tariff pause deadline, Trump will likely renew his attacks on Powell. While markets have been disappointed by the higher tariffs embedded in the so-called trade deals, they should take some relief that these agreements signal a temporary closure to this month’s trade tensions. The careful management of US-China trade relations through extending the tariff truce should reinforce this stability, even if risks remain.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025