- We maintain our cautious view on the luxury sector due to anticipated slowdown in consumer spending across US, China, and Japan

- Earnings growth has been revised down significantly since Liberation Day and the sector is unlikely to benefit from the recent EU-US tariff relief

- We favour companies with less US exposure, strong pricing power and brand desirability, and robust underlying fundamentals

- Selective investment opportunities on Quiet Luxury brands remain, as they are better positioned to withstand the current climate given their superior quality, heritage, and exclusivity

- Spending by affluent consumers, which is more bolstered against economic headwinds, should further support the Quiet Luxury market

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

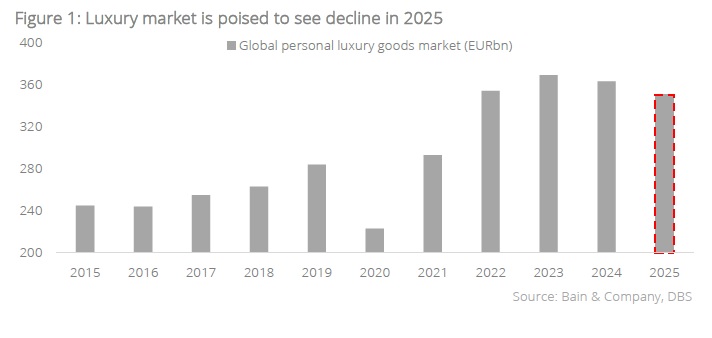

Cautious stance on weakening luxury market. A sense of caution pervades the luxury sector, with Bain & Company forecasting a contraction of 2-5% in 2025. This anticipated downturn is primarily attributed to the weakening of consumer discretionary spending across key markets, notably the US and China, as ongoing economic uncertainty weighs on consumer confidence. Even the resilient Japanese luxury market, which performed strongly in 2024, is experiencing a slowdown this year due to declining tourist spending, especially from Chinese, impacted by a strengthening yen.

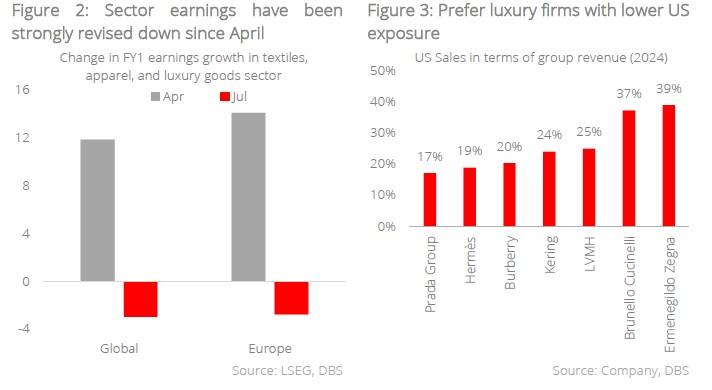

15% tariffs on EU goods still pose a meaningful risk. The EU and US have agreed on 15% US tariffs on EU imports, with EU goods already facing a 10% levy since Liberation Day. While the tariffs are lower than Trump’s 30% threats earlier this month, the luxury sector is unlikely to benefit from this relief and will continue to face demand pressures amid a deteriorating global outlook. Accordingly, global luxury sector earnings growth forecast has been revised down to -3% from +12% at the start of April.

Sector-specific exemptions are unlikely due to limited manufacturing capacity within the US. Luxury brands may respond by raising prices in the US, prompting tourism to Europe. Shifting production overseas will be limited due to specialised craftmanship and skilled labour shortage. However, fully passing the increased costs to US consumers is also unlikely given the weak consumer sentiment.

Given this outlook, we favour luxury companies with i) lower exposure to the US market, ii) strong pricing power and brand desirability, allowing them to capture a structurally growing ultra-high-end demand, and iii) robust underlying fundamentals as they are better equipped to weather near-term pressures.

Quiet Luxury prevails. As highlighted on our report Luxury, Redefined, Quiet Luxury brands are better positioned to withstand the current environment given its quality excellence, strong brand heritage, and product offering exclusive to the most affluent clients. The luxury market has been experiencing shifts in consumer preferences where consumers are desiring Quiet Luxury aesthetics and exclusivity, and timeless, investment-grade jewelleries. In 2024, demand for jewellery remained robust with 2% market growth, as reported by Bain & Company, while the leather goods market weakened by 5%.

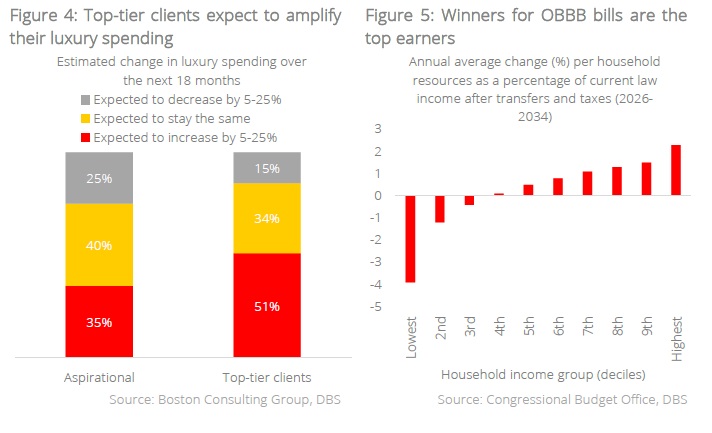

Affluent individuals continue to spend. This market’s resilience stems from the fact that high-net worth individuals’ spendings are more bolstered by economic headwinds. The most affluent clientele may only represent less than 1% of the global luxury market, but are responsible for a remarkable 23% of the total value in 2024. Boston Consulting Group indicates that 85% of these top-tier customers anticipate maintaining or increasing their spending in the near future. In contrast, a more cautious outlook prevails among aspirational customers, who comprise 60% of global luxury market. 65% expect to maintain or reduce their spending levels, reflecting a sluggish outlook for the loud luxury market.

OBBB a tailwind for Quiet Luxury. Trump's "One Big Beautiful Bill" (OBBB) has sparked market concerns about its potential to dampen US consumer spending. The Congressional Budget Office has highlighted the bill's uneven distribution of benefits, projecting that the wealthiest individuals will enjoy annual savings of 2.3%, while those with the lowest earnings could face annual losses of 3.9%. This disparity raises concerns about the bill's impact on overall consumer confidence and spending. However, we anticipate that the financial repercussions for high-net-worth individuals will be minimal, bolstering the continued demand for Quiet Luxury.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025