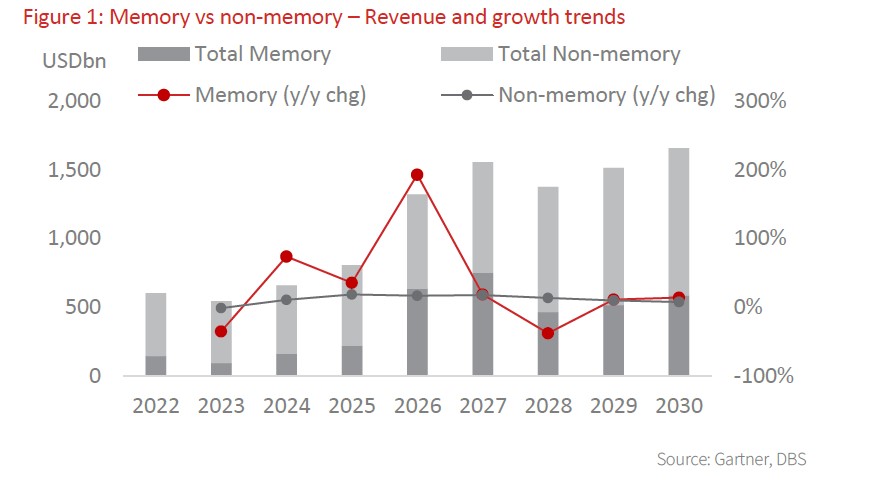

- AI is driving a structural memory supercycle, lifting memory’s revenue share in semiconductors to c.48% in 2026

- HBM/advanced DRAM demand is lifting pricing, profitability, and capex across the semiconductor sector with the cycle projected to sustain beyond 2028

- TurboQuant has further enhanced the upcycle and the efficiency gains will accelerate AI adoption, supporting HBM/DRAM demand

- Guidance from industry leaders reinforces durable and tight-supply conditions, signalling strong pricing power and a multi-year AI-led demand into and after 2027

Related Insights

- China Chartbook: Dual speed growth28 May 2026

- Fixed Income Weekly: Peace Hopes Drive Rates Relief28 May 2026

- Research Library28 May 2026

AI is driving a structural memory supercycle, with memory’s share of global semiconductor revenue set to jump sharply from 27% in 2025 to around 48% in 2026. This is underpinned by accelerating demand for high bandwidth memory (HBM) and advanced DRAM to support large scale AI training and inference workloads. Robust AI server deployment is lifting pricing, profitability, and capital investment across the broader semiconductor value chain. The cycle is expected to sustain through 2026 and extend beyond 2028/2029. The momentum is driven by sustained AI server build-outs and structurally higher DRAM & NAND content per system, boosting the upcycle beyond current expectations.

Is TurboQuant a real threat to the memory supercycle? Google’s TurboQuant, launched in end Mar 2026, has sparked short-term market fears but is unlikely to derail the AI-driven memory supercycle as it improves the efficiency of inference workloads instead of reducing the structural memory demand. While the technology can compress runtime memory and lower cost per inference, the resulting productivity gains are more likely to accelerate AI adoption and expand total workloads, ultimately sustaining demand for HBM and advanced DRAM. Thus, TurboQuant is better viewed as a cycle extender rather than a cycle breaker as it improves efficiency but does not eliminate core memory demand.

Strong guidance signals durable AI-led memory cycle. Recent results from Micron, SK Hynix, and Samsung collectively point to a structurally strong AI-led memory cycle with tight supply conditions likely to persist beyond 2027, underpinned by accelerating demand for HBM and AI server infrastructure. Micron delivered record revenue and guided for another step-up in margins and sales, signalling sustained pricing power and continued capacity expansion to support hyperscaler demand. Meanwhile, Samsung expects a strong surge in profit, driven by strong AI memory demand and limited supply while continuing aggressive investment in next-generation DRAM and HBM capacity to capture the cycle. SK Hynix remains a key beneficiary of the AI build-out as the demand for advanced memory remains robust.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- China Chartbook: Dual speed growth28 May 2026

- Fixed Income Weekly: Peace Hopes Drive Rates Relief28 May 2026

- Research Library28 May 2026

Related Insights

- China Chartbook: Dual speed growth28 May 2026

- Fixed Income Weekly: Peace Hopes Drive Rates Relief28 May 2026

- Research Library28 May 2026