- US banking CEOs warn of potential headwinds from US commercial real estate; their concerns are valid

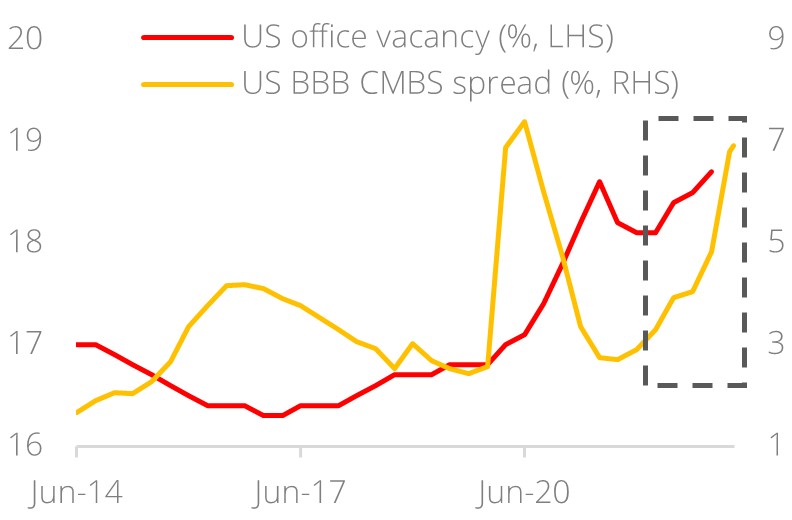

- US office vacancy on the rise amid rising adoption of remote work

- c.USD1.5t worth of debt are set to mature by end-2025 and companies will find it challenging to refinance in the current environment

- Rising recession risks and diverging buyer-seller expectations translate to lower visibility in real estate valuation; the latter deters banks from extending new loans

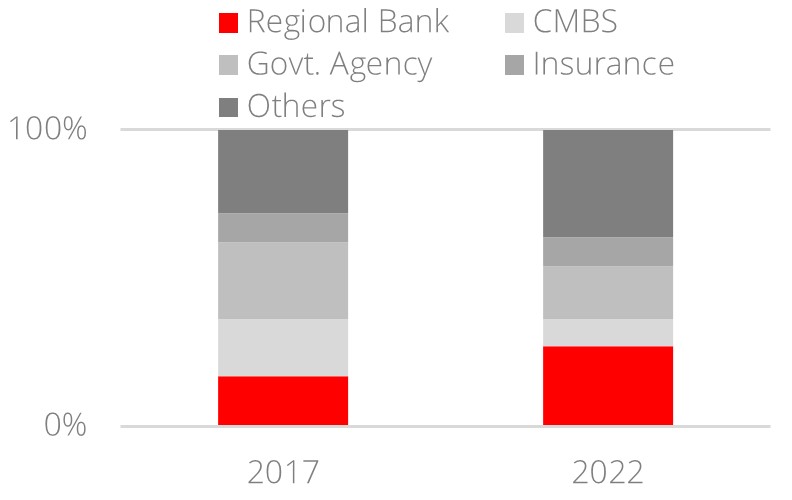

- US regional banks most at risk as exposure to commercial real estate has increased sharply

Related insights_tr

Double whammy: Rising remote work and refinancing risks. After the recent US regional banking fiasco, another storm brews in US commercial real estate. Indeed, judging from comments issued by US banks (Wells Fargo and Morgan Stanley) in the current earnings season, it is clear that the c.USD20.7t commercial real estate space is the next major headwind.

US office vacancy in metro areas is on the rise. From a pre-pandemic level of 16.8% in Dec 2019, it has since increased to 18.7% in Dec 2022. This has, in turn, coincided with widening option-adjusted spreads for US BBB commercial mortgage-backed securities, from 257 bps to 483 bps. The challenges are both structural and cyclical:

- Structural challenge – rising adoption of remote work: Since the Covid-19 pandemic, adoption of remote work has risen, translating to lower occupancy rates for US offices. Evidently, this structural trend is here to stay. According to McKinsey, American employees embrace remote work, with 87% of survey respondents taking up the offer when given the option.

- Cyclical challenge – rising refinancing risks: The rise in bond yields complicates the matter, both from a refinancing and valuation perspective.

An estimated USD1.5t worth of commercial real estate debts are set to mature by end-2025, most of which were financed in an era where bond yields were close to zero. Accordingly, companies will find it challenging to refinance in the current environment where the cost of capital is high.

Above all, the rise in bond yields also broadly translates to higher cap rates which in turn suppresses commercial real estate valuation.

Rising recession risks and the creation of a doom loop? According to Bloomberg Economics, the probability of a US recession within the next six months is 99.9%. In other words, recession is a given and the only unknown is how severe it will be. Rising recession risk adds another layer of complexity to this commercial real estate issue.

As the cost of financing rises and funding becomes scarce, the gap between buyers’ and sellers’ expectations will diverge. This, set against a background of rising recession risks, will translate to lower visibility in real estate valuation. Banks are hesitant to extend new loans under such conditions, thus creating a doom loop which can become self-reinforcing.

US Regional Banks: Most exposed to commercial real estate lending. According to MSCI, regional banks account for the largest share of commercial real estate lending in 2022 at 27%, a marked increase from 17% in 2017. In contrast, the share of government agencies’ exposure fell from 26% to 18%. As stresses in commercial real estate intensify, regional banks will incrementally limit their exposure to this space, leading to further scarcity in funding.

CIO Barbell Strategy: Zero direct equity exposure to US commercial real estate and regional banks. Our CIO Barbell Strategy is relatively shielded from any potential upheaval in US commercial real estate given the absence of direct equity exposure. Instead, our preferred commercial real estate exposure is via Singapore REITs given their defensiveness and attractive dividend profile.

Meanwhile, the prevalence of US commercial real estate concerns will weigh on the performance of US regional banks, triggering further flight to quality. The CIO Barbell Strategy does not have any exposure to US regional banks. We reiterate our preference for US large banks in the financials space.

Figure1: Widening CMBS spreads

Figure2: Commercial real estate lending

Source: Bloomberg, MSCI, DBS

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.