Related Insights

- China Healthcare: From Derivative to Definitive25 Mar 2026

- US Hotels: Souring Year as Geopolitical Tensions Bite25 Mar 2026

- Research Library25 Mar 2026

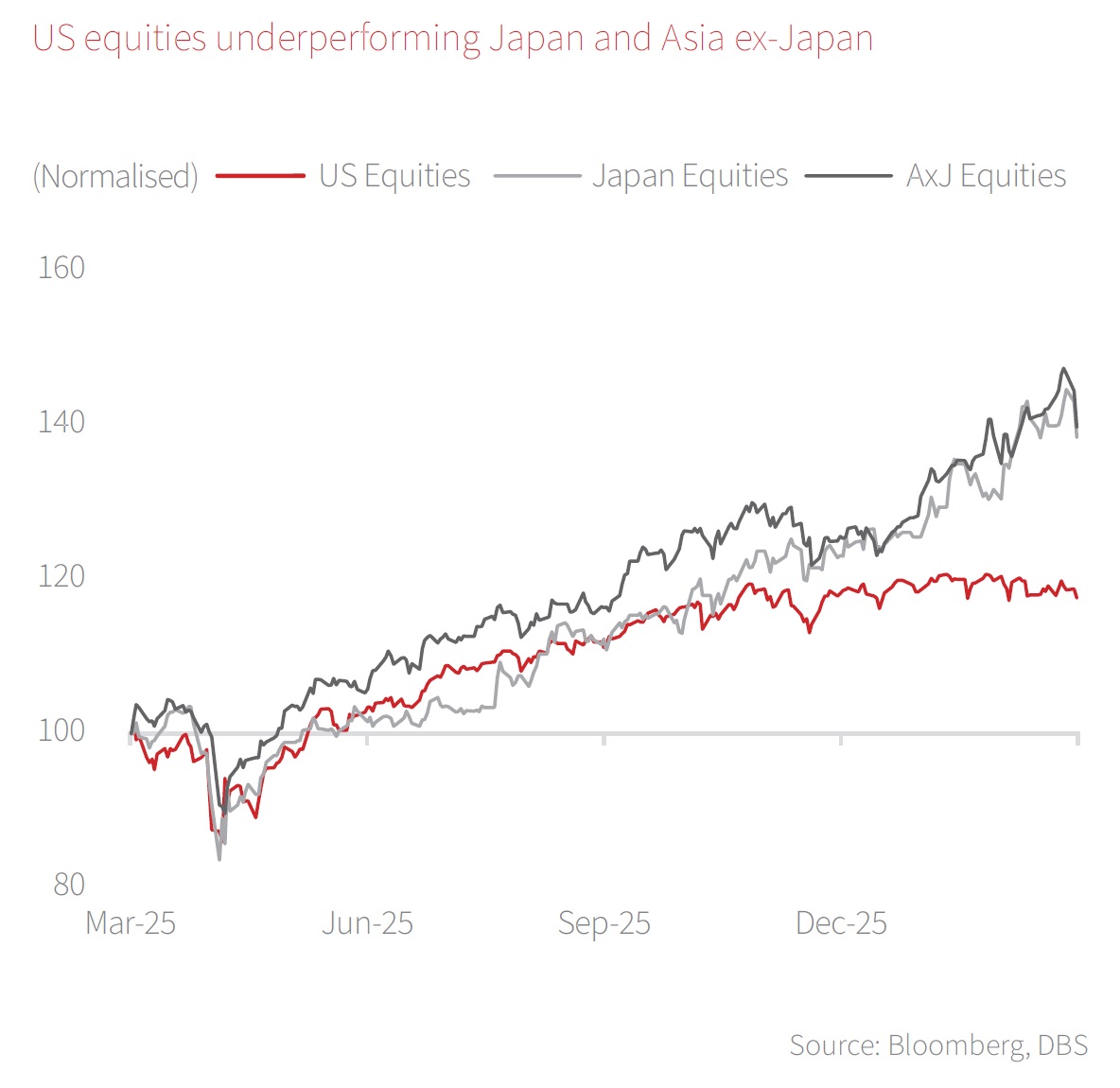

Winds of change as rotational shifts gather momentum. The performance of global equities this year unveils two trends. First, the US market is no longer investors’ darling, as fund managers increasingly jump on the bandwagon of reducing their US dollar exposure. This explains the lacklustre 0.5% decline in US equities (as of 3 Mar), as compared to average gains of 9.4% for Japan and Asia ex-Japan. Second, within US equities, investors are clearly pivoting away from technology plays towards more traditional industries such as energy, materials, and industrials. Both trends are underpinned by fundamental drivers and are likely to persist in the coming quarters.

The shift away from US assets has been well flagged in the media. Elevated US indebtedness has raised concerns over Uncle Sam’s ability to service rising debt costs, a debacle made worse by the “One Big Beautiful Bill”, which introduces substantial tax cuts at a time when the country can ill afford it. Adding fuel to the fire is the recent US Supreme Court decision on the legality of Trump’s tariff war, which opens the door to potential repayments of previously collected tariff revenue. These fiscal concerns, coupled with Trump’s frequent attacks on the independence of national institutions, have compelled investors to diversify their holdings and reduce portfolio concentration in US markets.

technology is both tactical and strategic. On the tactical front, it reflects a broader move away from “crowded trades”, where valuations are rich and expectations remaining sky high. Importantly, the shift from tech plays also signals investors’ progression to the next stage of the AI investment cycle. From an initial focus on “innovators”, attention is now turning to identifying the “winners and losers” of the AI revolution.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- China Healthcare: From Derivative to Definitive25 Mar 2026

- US Hotels: Souring Year as Geopolitical Tensions Bite25 Mar 2026

- Research Library25 Mar 2026

Related Insights

- China Healthcare: From Derivative to Definitive25 Mar 2026

- US Hotels: Souring Year as Geopolitical Tensions Bite25 Mar 2026

- Research Library25 Mar 2026