- US: Core inflation data in line with expectations, helping to support a mid-year rate cut narrative; resilient labour market signals the Fed should be more wary of upside risks to inflation

- Eurozone: Last mile of disinflation in the Eurozone more challenging than anticipated; policymakers to monitor ongoing wage negotiations closely to gauge pipeline pressures; ECB expected to keep rates unchanged

- China: Key economic targets and policy priorities in the NPC’s ‘Government Work Report’ seek to attract foreign investments and support sustainable growth; China’s dominance in “new three” industries central to sustainable growth

Related insights_tr

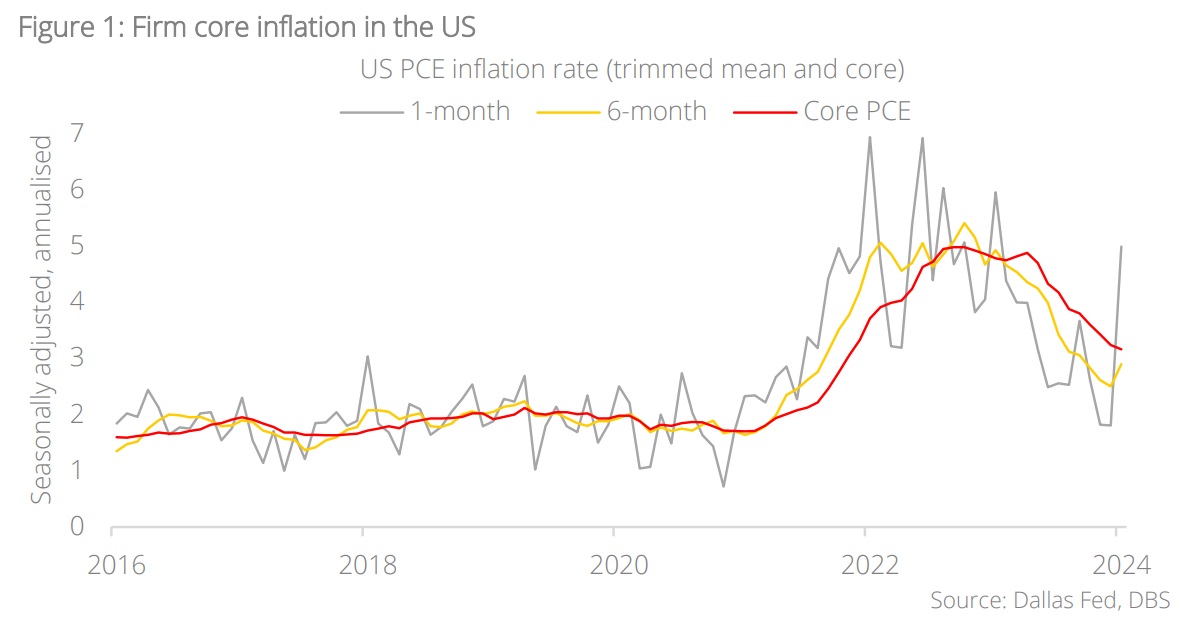

US: Firm core inflation. Markets were sanguine with the January personal consumption expenditure (PCE) inflation data release last week (ended 1 March). Both PCE (2.4% y/y) and core PCE (2.8% y/y) inflation readings were in line with expectations, supporting a mid-year rate cut scenario. However, the Dallas Fed’s trimmed mean PCE, an alternative measure of core, jumped by 5% y/y. This was driven by spikes in financial and hospital services, along with computer software and some beverage prices. Next week, consensus expects CPI inflation to increase again to 0.4% m/m in February after rising to 0.3% in January from 0.2% in the previous month. We believe caution is warranted.

Keeping an eye on the labour market. Friday’s Nonfarm Payrolls (NFP) will provide another pulse check on the labour market, which has proven resilient through this cycle. With two strong prints (333k and 353k in December and January respectively) in the bag, consensus is looking for a moderation to 200k, a level that is more consistent with full employment. Job creation at this pace with an unemployment rate below 4% could then translate into somewhat sticky wages (4.5% y/y in January). Based on these three metrics, the economy is doing remarkably well, and the Fed should be more cognisant of upside risks to inflation. That said, we note that the average weekly hours worked has dipped to 34.1, levels not seen since the early part of the pandemic in 2020. This divergence between firm NFP and lower hours worked is probably what is keeping a measure of caution in the markets.

Current market pricing (150 bps of rate cuts by end-2025) is about in line with the Fed’s December dot plot after the rates selloff over the past few weeks. However, February’s labour market and inflation data could have an impact on the Fed’s guidance at the Federal Open Market Committee (FOMC) meeting on 21 March. Another NFP print that is above 200k and/or another sticky Consumer Price Index (CPI) print could change the calculus. While recent Fed-speak point to a base case of cuts later this year, another month of upside surprises may prompt a tweak of the dot plot (perhaps less cuts in the dot plot) as worries tilt towards no-landing. If delayed/less cuts get worked in rates pricing, curve steepening would also be delayed.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.