- Equities: Property crisis amid an economic slowdown heightens investors’ expectation for more aggressive action from PBOC to stabilise the economy

- Credit: Rates volatility to persist as strong fiscal stimulus runs at odds to Fed’s monetary tightening. 3-5Y remains duration sweet spot to avoid excessive duration risks

- FX: DXY and its components ranged from converging monetary policy stances; Downside bias for GBP/USD within its 3- month range between 1.25 and 1.28

- Rates: DM rates facing uncertainties as market participants struggled to find appropriate pricing; We expect Fed to cut in mid-year and deliver four cuts in 2024

- The Week Ahead: Keep a lookout for US Change in Nonfarm Payrolls; China CPI Number

Related insights_tr

Chinese equities rose on optimism of stronger stimulus from PBOC. China’s economy continued to show signs of slowing growth where the February official manufacturing Purchasing Managers’ Index (PMI) number remained in contractionary territory at 49.1, dipping below 49.2 reported in the previous month. Additionally, according to China Real Estate Information Corp (CREIC), China’s top 100 developers saw property sales decline for the tenth consecutive month, plummeting 60% y/y in February. This property crisis amid an economic slowdown has heightened investors’ expectations for more aggressive policy supports from the People’s Bank of China (PBOC) to stabilise the economy. The SHCOM and CSI300 gained 0.7% and 1.4% respectively for the week.

China’s two sessions to dominate sentiments for the next two weeks. The two sessions which commence today (4 Mar), refer to the concurrent annual meetings held by China’s two main political bodies, the National People’s Congress (NPC) and the National Committee of the Chinese People’s Political Consultative Conference (CPPCC), focusing on China’s policy framework and plans moving forward. Apart from the stimulus measures, another key indicator would be investors’ attention to the gross domestic product (GDP) growth target. Currently, market is expecting a GDP growth target of 4.6% in 2024.

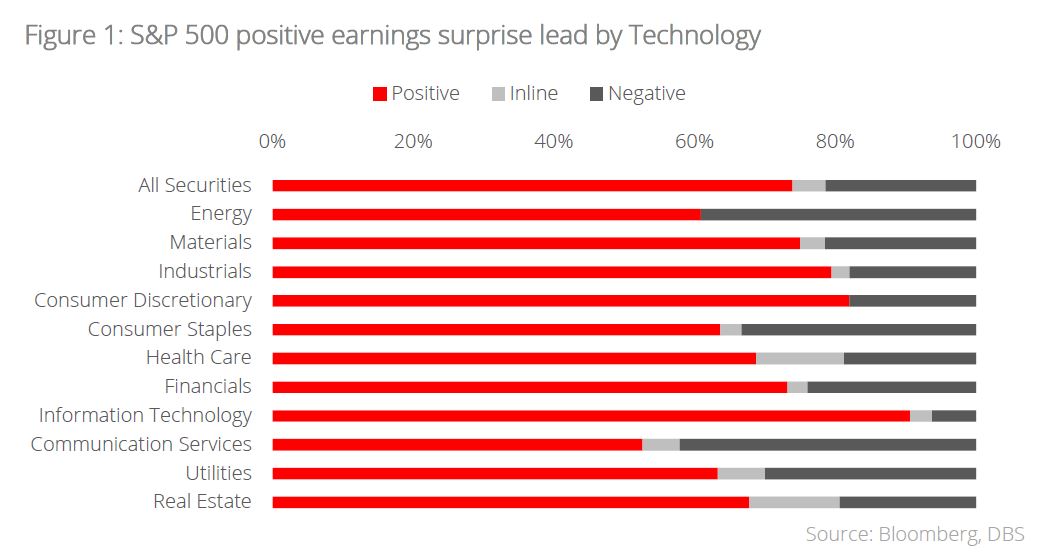

Topic in focus: US Equities – Solid end to earnings season. US equities continue their stellar run in 2024 with both the NASDAQ composite and S&P 500 index reaching record highs late last week (ended 1 Mar). This is in large part due to the current earnings season, which is concluding on a high; 492 out of 500 companies have reported earnings and 74% of them posted beats on quarterly earnings, above the average beat rate of 67% (since 1994). On a sectoral basis, Technology stands out as having the highest positive earnings surprise at 90%, buoyed by the wave of AI-related growth opportunities. Another stand-out sector is Consumer Discretionary, which notched an 82% positive earnings surprise.

On the back of this earnings season, we advocate investors stick with quality and invest in sector leaders with wide economic moats. At the same time, sectoral diversification is a must; while it is crucial to have meaningful exposure to Big Tech and the Magnificent 7 given their robust earnings growth, it is also important to be present in other sectors as profit growth broadens out. Within the ex-Tech space, we have preference for Quiet Luxury plays within the Consumer Discretionary sector and select opportunities within Healthcare that benefit from secular trends such as ageing demographics and the rise of obesity and lifestyle diseases.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.