Related insights_tr

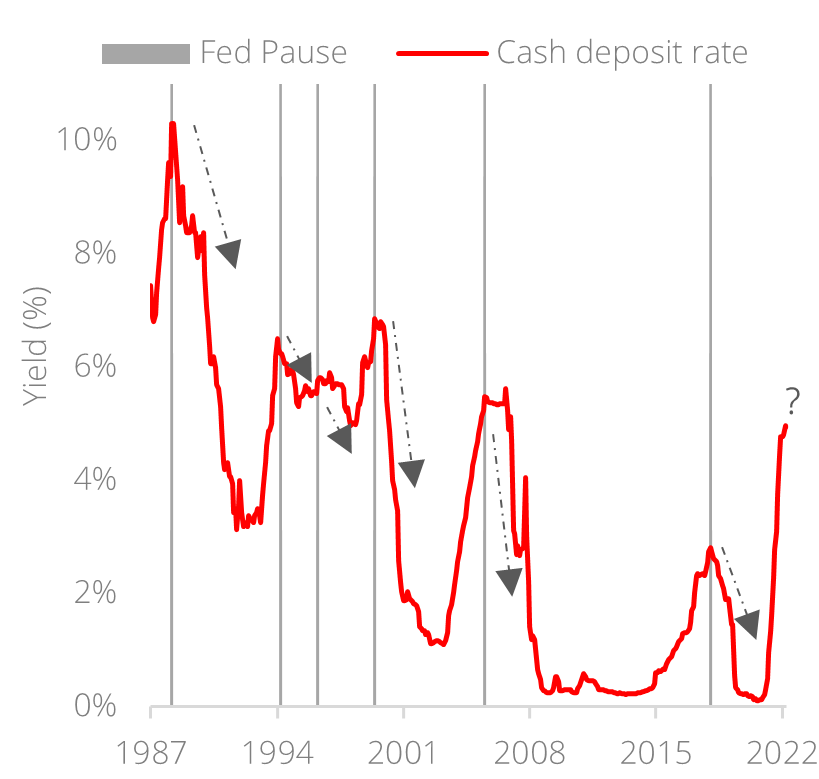

Figure 1: Fed pauses usually signal peaks in cash deposit rates

Source: Bloomberg, DBS

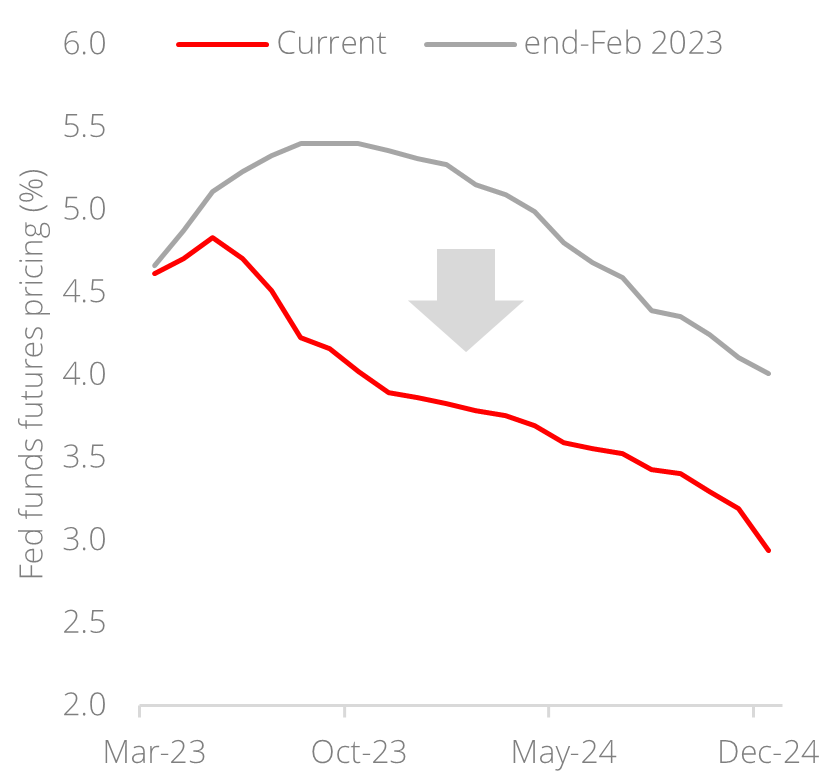

Bad news comes in pairs – high returns of cash is now at risk. Not only have concentration risks of cash deposits been made apparent, but so have return risks. Banking sector-related stresses have resurfaced narratives of monetary policy tightening having run its course, resulting in a massive 1.5% decline in the December Fed funds futures pricing since end-Feb 2023. Should this signal a pause in/the end of the Fed hike cycle, the days of high yields on cash deposits are certainly numbered, if history is any guide.

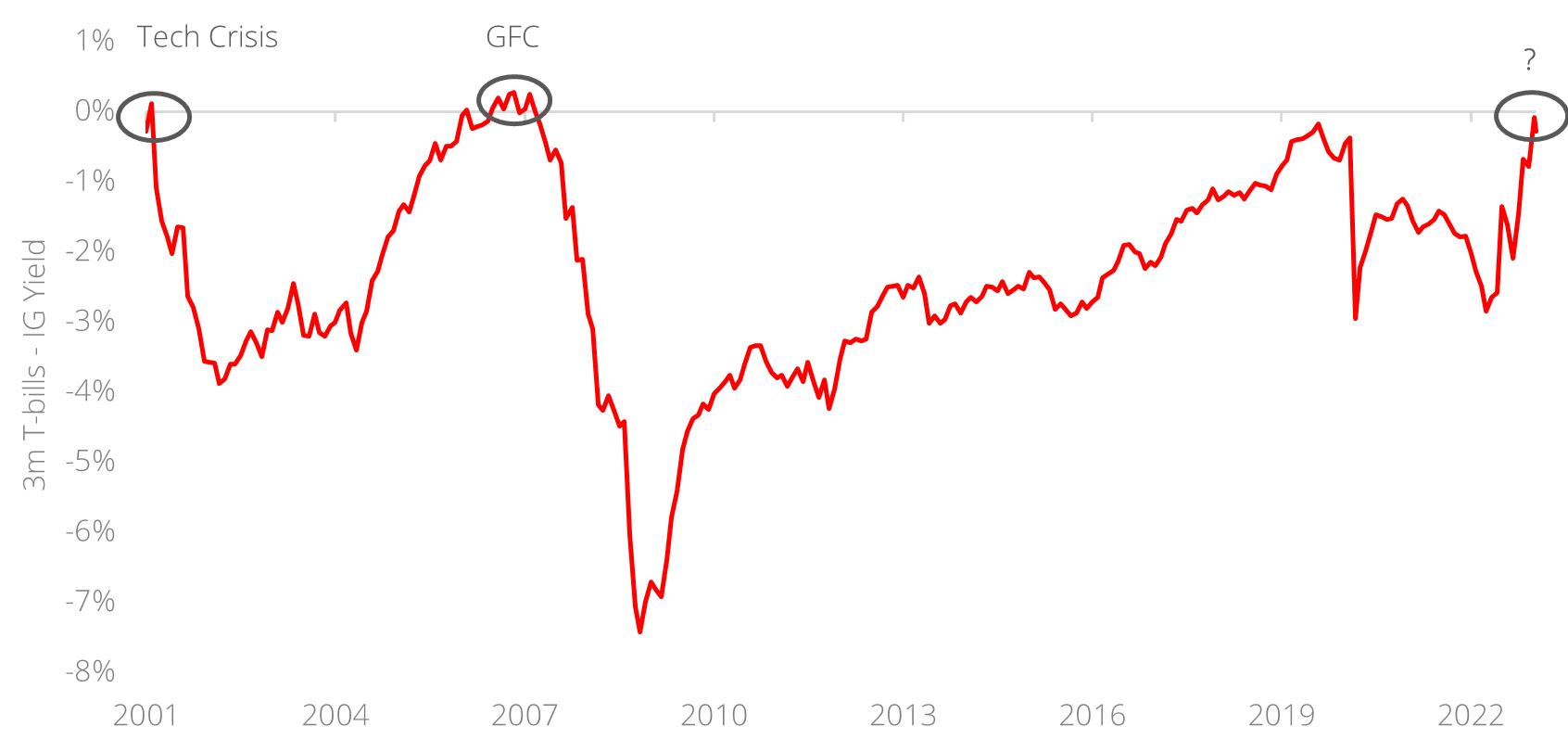

Figure 2: Cash never yields the same as IG credit for long

Source: Bloomberg, DBS

Cash or credit? This was the premise for our long-standing preference for quality credit over cash deposits, given that investors (a) can be well-diversified rather than have financial sector concentration risks, and (b) can lock in higher yields for a longer duration than the fleeting high rates of cash. The past 20 years illustrates this clearly; cash yields hardly ever come close to IG credit for more than a year. This means that investors are often better off taking a bit of duration risk in IG credit to lock in such high yields for a longer timeframe.

Moreover, high cash rates are not sustainable in a highly leveraged world; when cash and IG yields coincide, a recession generally ensues which forces rates lower again. Investors who hold only cash would merely see reinvestment risks with the decline in rates, while IG credit investors would experience capital gains as the rate environment adjusts lower, lifting bond prices.

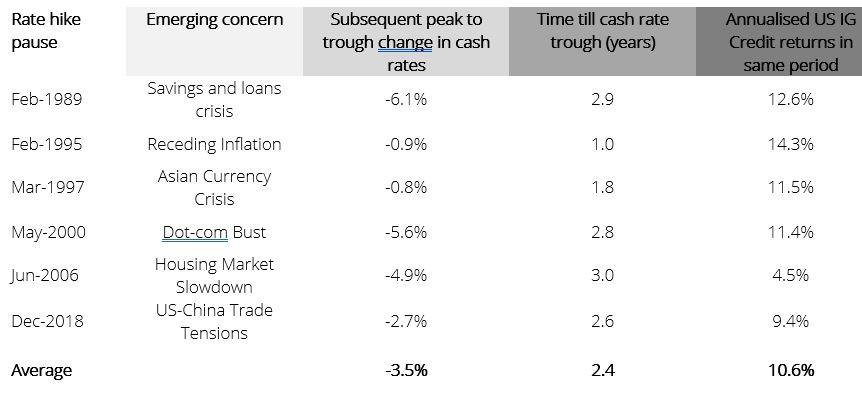

Figure 3: Quality credit outperforms cash after the Fed takes a pause

Source: Bloomberg, DBS

Echoes of the past. This phenomenon of credit outperforming cash is clearly observed in the notable episodes of Fed pauses since 1987. In the six instances observed above, cash rates (approximated by the 3-month LIBOR) see a mean peak-to-trough yield decline of 3.5% over 2.4 years on average following a pause in the rate hike cycle – usually due to the emergence of some form of economic stress – implying that reinvestment risk runs high once the hiking cycle is over. IG Credit on the other hand, sees tailwinds take over from the lower rates environment, averaging an annualized yield of 10.6% in the same period.

Stay with quality short duration credit. Towards the end of 2022, we opined that there was going to be a narrowing window for higher yields of such quality credit, due to (a) the inverted yield curve, (b) moderating inflation, and (c) Fed policy rate projections. What was not consensus at the time is fast becoming apparent, with systemic stresses in the financial markets coming to the fore. We continue to recommend that investors capitalize on this narrowing window by shifting cash towards high quality credit – in what we termed the Liquid+ strategy – to capture yields while stocks last.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.