- 4QCY25 largely in-line; pricing, mix, and productivity supported margins

- FY26 guidance cautious; low-to-mid single-digit sales, modest EPS growth

- Tariff and raw material volatility risks manageable via pricing and sourcing mitigation

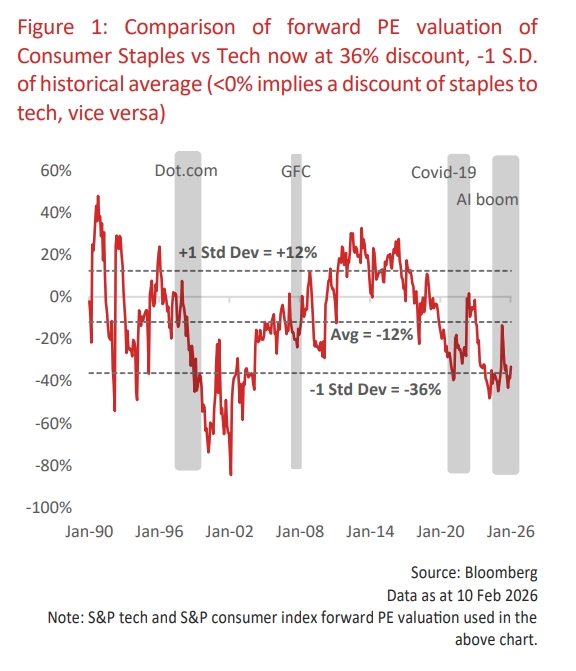

- Staples trade at -36% PE discount, offering defensive rotation opportunity

Related Insights

- DBS Stock Pulse: Equity Picks – Buy the drop!05 Mar 2026

- Research Library04 Mar 2026

- Caution as DXY approaches 100 04 Mar 2026

Resilient 4QFY25 amid mixed volumes. Global Staples – Food & Beverage, and Personal & Home Care – delivered largely in-line 4QFY25 results, with earnings dispersion reflecting pricing power and mix. Coca-Cola and Mondelez posted core EPS modestly ahead of consensus, supported by mid-single-digit organic revenue growth y/y and favourable mix shifts towards away-from-home beverages and premium snacking. PepsiCo met expectations as low-single-digit revenue growth was offset by steady cost discipline in Frito-Lay North America. Kraft Heinz remained more challenged, with declining sales as North American volume stayed negative despite flat pricing. Within Personal & Home Care, market leaders Procter & Gamble (P&G) and Colgate-Palmolive delivered low-to-mid single-digit organic growth and small EPS beats, aided by productivity savings and premium innovation in Fabric & Home Care and Oral Care, respectively. Across the group, gross margin recovery was driven by easing commodity input costs, pricing carry-over, and mix premiumisation rather than pure volume leverage. Free cash flow generation strengthened at P&G, Coca-Cola, and Colgate-Palmolive, enabling continued share buybacks and dividend growth, while Kraft Heinz built up a higher cash balance likely in preparation of separation, which has since been shelved.

Outlook cautious but constructive. Management tone heading into FY26 is measured, with most guiding for low-to-mid single-digit organic sales growth and mid-single-digit EPS growth, underpinned by productivity and disciplined reinvestment. Beverage exposure to emerging markets remains a relative bright spot, particularly for Coca-Cola, where management cited resilient demand in Latin America and parts of Asia despite currency volatility. By contrast, North American centre-store food and US prestige beauty remain softer, though companies highlighted sequential improvement in retailer inventory and promotional intensity. Several companies flagged incremental tariff exposure on aluminium packaging and select China-US trade flows relative to prior assumptions, but reiterated that mitigation via pricing, sourcing diversification, and hedging should limit net EPS impact to low tens of basis points. Broader input cost outlook is stable, with pulp and freight benign, though cocoa inflation remains a headwind for Mondelez given their forward hedges currently in place.

Valuation gap presents defensive opportunity. The US Consumer Staples Index currently trades at a c.-36% forward P/E discount to the US IT Index, around -1 S.D. below its historical average since 1990 and materially wider than the long-term discount of 12%. This valuation dispersion appears stretched given staples’ resilient cash flows, pricing power, and visible capital return, particularly among scaled Personal & Home Care leaders with strong balance sheets and structural cost initiatives. Demand stability across daily-use categories and flexibility to calibrate pricing and promotion should prove supportive if macro conditions soften. Against a backdrop of elevated broader market valuation, the relative de-rating suggests investors may consider rotating selectively into high-quality staples franchises where margin recovery, disciplined capital allocation, and emerging market exposure provide a more defensive earnings profile at historically attractive relative multiples.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- DBS Stock Pulse: Equity Picks – Buy the drop!05 Mar 2026

- Research Library04 Mar 2026

- Caution as DXY approaches 100 04 Mar 2026

Related Insights

- DBS Stock Pulse: Equity Picks – Buy the drop!05 Mar 2026

- Research Library04 Mar 2026

- Caution as DXY approaches 100 04 Mar 2026