- Geopolitical tension and unilateral actions are driving a dramatic increase in global defence spending, fuelling demand for self-sufficiency and diversified supply chains

- Defence capex carries strong upside potential as governments commit to multi-year modernisation and technological upgrades, creating sustained growth opportunities across the sector’s ecosystem

- Traditional prime defence contractors will continue to dominate, capturing majority of budgets through scale, massive orderbook backlogs, proven platforms, and cost-plus contracts, delivering steady profits and returns

- Non-traditional high-tech disruptors are gaining traction and relevance thanks to their agile, software-centric innovation in AI, autonomy, drones, and dual-use (commercial & defence) technologies

- Modern warfare’s swiftly shifting dynamics favours high-tech non-traditional contractors, with primes also adapting quickly via M&As and partnerships; ride the trend with a fine balance of stability a

Related Insights

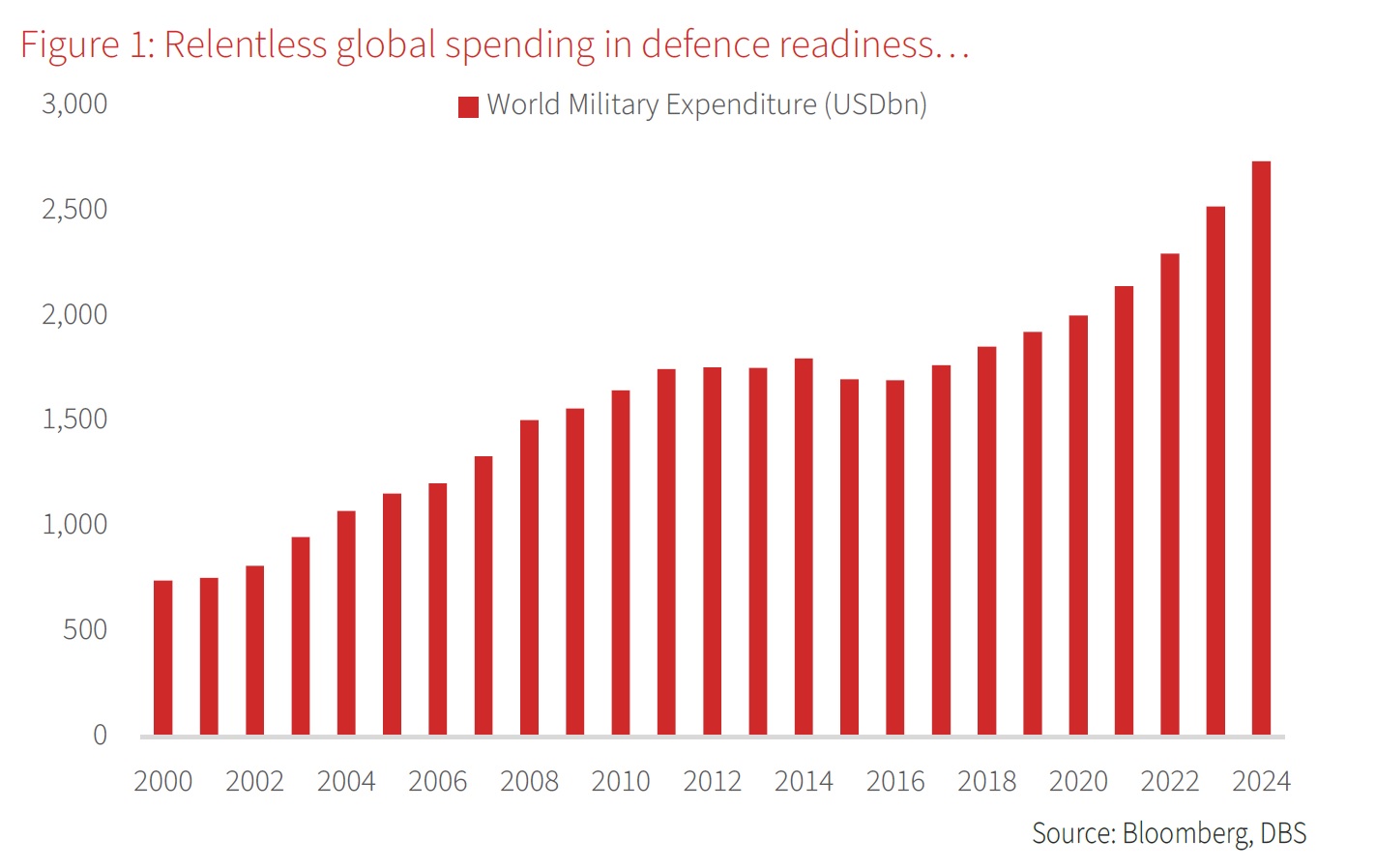

A prominent surge in defence spending. In an era where geopolitical fault lines crackle with unprecedented intensity – from Russia’s grinding assault on Ukraine to simmering American rivalries in the Western Hemisphere – the world’s governments are reaching deeper into their coffers. Global defence spending swelled to USD2.7tn in 2024 and is on track to reach >USD3.3tn by the end of the decade. This surge, propelled by NATO’s ambitious pledge to hoist expenditures to 5% of GDP by 2035 (up from a paltry 2% today), Japan’s plan to double spending by 2027, and the US’s target to raise defence spending by 50% over the same period, reflects not just paranoia but a grim calculus: the cost of deterrence in a multipolar world fraught with economic warfare, territorial spats and the spectre of great-power conflict.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.