- US: US consumption grew robustly last year, though sustaining such growth may be untenable in 2026; the Fed has the tools to counter any incipient downside to consumption; we expect two 25 bps rate cuts to be delivered in 2H26

- Singapore: We view Budget 2026 as a strategic, forward-looking plan that sharpens Singapore’s economic competitiveness and strengthens the social compact under the Forward Singapore agenda, underpinned by fiscal discipline

- Thailand: We expect the dovish BOT to cut its policy rate by 25 bps to 1.00% in 2026, but it will likely hold in February following better-than-expected 4Q25 growth; we maintain our forecast for slower growth of 1.6% in 2026, given various challenges

Related Insights

- Research Library24 Feb 2026

- DACS: Lesser impact from US tariffs24 Feb 2026

- India markets: Cautious relief from US tariff ruling, domestics sway bonds24 Feb 2026

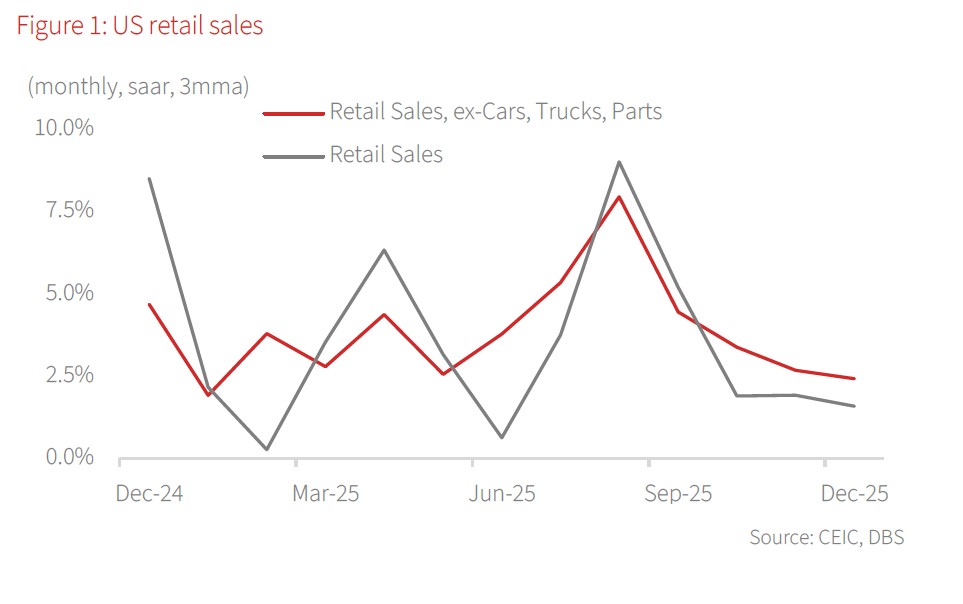

US: Slowing US consumption; we pencil two rate cuts in 2H26. Despite trade wars and policy uncertainty, sticky inflation, and geopolitical tussles, US consumption remained strong through 2025. We estimate a 4% growth in retail spending last year – the highest in three years. However, there are early signs of a slowdown, especially in the 4Q25 data. We estimate progressively slower retail sales growth from September onward across various permutations of the data (e.g. including or excluding auto sales). The implication of this development is visible in real-time GDP estimates. The Atlanta Fed’s recent downward revision of its US GDP Nowcast, from over 5% to over 3%, has been driven entirely by slowness in consumption growth.

Placed in context, the consumption trend does not appear worrisome. The US household/GDP ratio has been declining for half a decade, net worth has risen considerably due to stock market gains, and real interest rates have fallen following Fed rate cuts. Aided by tax cuts from President Trump’s legislative measures last year, consumption ought to remain resilient, even if it is not sustainable at last year’s torrid pace.

That said, tariff passthrough to inflation and job-related uncertainties could weigh on consumer sentiment. Oil prices, currently low, could spike amid US actions in the Middle East, posing further downside risks to sentiment. Survey readings, such as the Michigan Survey, highlight a bifurcated economy. Households at the lower end of the income spectrum, who have minimal exposure to stock market gains, are feeling particularly despondent, and these readings could deteriorate further.

Authorities have tools to address such eventualities. The Fed has been under considerable pressure from the White House to cut rates in any case, and emerging downside risks to consumption would provide ample motivation.

Meanwhile, recent Fed minutes were more hawkish than generally expected, as policymakers discussed a potential rebound in the labour market, sticky inflation, and even the possibility of rate hikes. With these views, the hurdle for near-term cuts remains high.

We have pencilled in two Fed rate cuts this year, one in 3Q26 and another in 4Q26. We do not believe inflation remaining well over target will be a constraint. In our view, sub-2% inflation is unlikely to characterise the US economy for some time. Since the pandemic, the Fed’s aim seems to have been to run the economy “hot”, a stance we expect to continue under incoming Chair Warsh.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Research Library24 Feb 2026

- DACS: Lesser impact from US tariffs24 Feb 2026

- India markets: Cautious relief from US tariff ruling, domestics sway bonds24 Feb 2026

Related Insights

- Research Library24 Feb 2026

- DACS: Lesser impact from US tariffs24 Feb 2026

- India markets: Cautious relief from US tariff ruling, domestics sway bonds24 Feb 2026