- A potential 10% interest rate cap on credit cards will impact big card issuers with sizeable cards portfolio the most

- US banks are likely to continue to see big shareholder payouts supported by further regulation reduction

- We expect US banks to register resilient high single-digit y/y earnings growth as investment banking fees and trading income continue to boost non-interest income

- We remain highly selective and favour US firms with a compelling restructuring story, riding on revenue growth and share buybacks

Related Insights

- Research Library13 Feb 2026

- US Jobs Rebound; Japan’s Landmark Election13 Feb 2026

- Take-Two Interactive Software Inc13 Feb 2026

Keeping a close watch on potential 10% interest rate cap on credit cards. President Trump continues to push for a temporary one-year interest rate cap of 10% in early 2026 to relieve high borrowing costs for US consumers. It remains to be seen how the rate cap can be implemented, with no federal law, executive order, or regulatory rule enacted as yet. It is widely believed that an executive order could be met with industry legal action, as some big lenders have criticised the rate cap. There is an ongoing debate about affordability versus ensuring credit access, as well as disruption to pricing of consumer credit risk, as most bank management agree that a cap will constrict credit eventually, potentially causing a slowdown to the economy. Most issuers have left rates unchanged for the time being. Fintech BILT has started to offer new credit cards with 10% interest rate on first year as an introductory offer. The proposed plans on a rate cap may hit big banks with sizable cards portfolios the most, namely JPM and Citi amongst others.

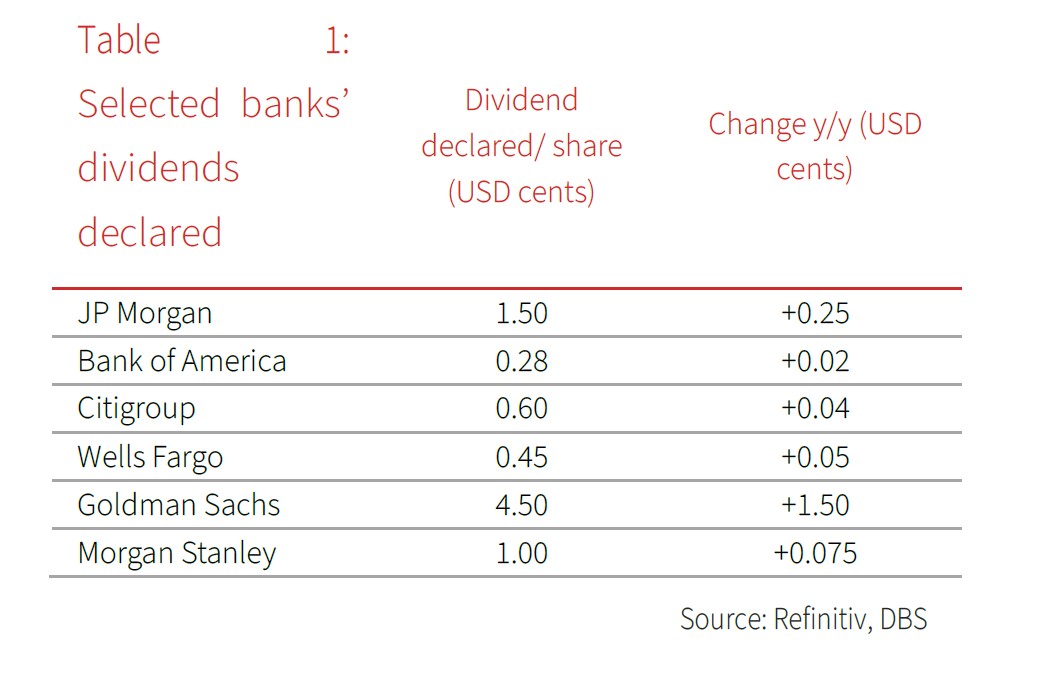

US Banks continue to see big shareholder payout given expected further regulation reduction. US regulators have moved to reduce post GFC rules governing large banks, in view of the current overly complex framework constraining growth. A central change is the narrowing of banking supervision, with Fed cutting supervision and regulation staff by c.30% and refocusing oversight on material risks including capital adequacy and major operational weaknesses, focusing less on compliance and documentation issues. A less stringent, risk-based capital framework, which is potentially capital-neutral, is likely to replace the original Basel III Endgame. The proposed easing of enhanced supplementary leverage ratio would relax capital requirements, particularly for large banks. During 2025, post 2025 stress tests, JPM has announced its largest share repurchase program till date, amounting to USD50bn with an unspecified end date, while BAC, Citi, WFC, GS, MS all raised dividends since 2H25 as ongoing excess capital return via higher dividends and share buyback continues.

A year of resilient earnings growth for US Banks; we remain highly selective. We believe US Banks are poised for high single-digit y/y earnings growth, as investment banking fees and trading income continue to boost non-interest income. Net interest income is likely to continue seeing modest growth on the back of lower funding costs amidst moderate asset growth. We recommend US firms with compelling restructuring story, riding on revenue growth and share buybacks.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Research Library13 Feb 2026

- US Jobs Rebound; Japan’s Landmark Election13 Feb 2026

- Take-Two Interactive Software Inc13 Feb 2026

Related Insights

- Research Library13 Feb 2026

- US Jobs Rebound; Japan’s Landmark Election13 Feb 2026

- Take-Two Interactive Software Inc13 Feb 2026