Related insights_tr

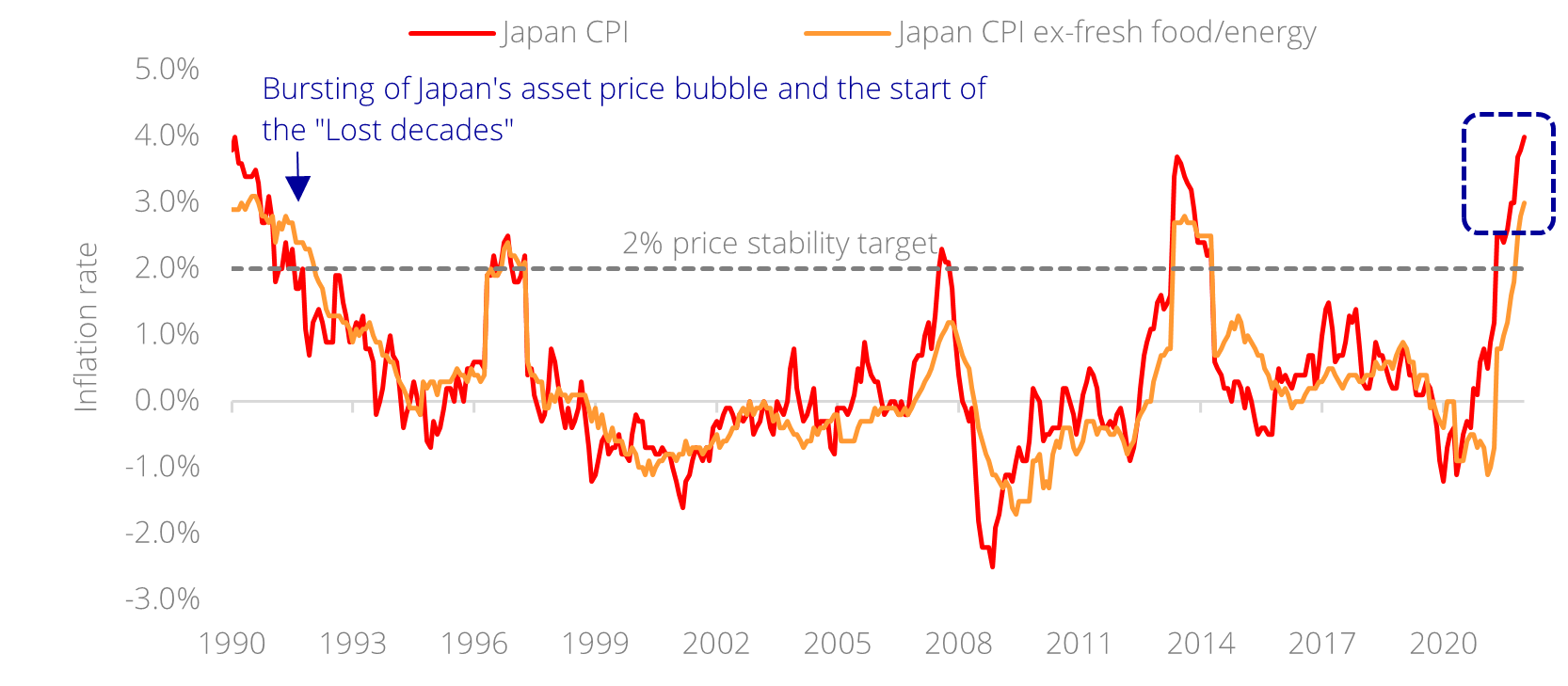

Japan’s inflation conundrum. The Bank of Japan (BOJ) gave the world a Christmas shock in 2022 by widening the trading band for 10Y JGB yields from ±25 bps to ±50 bps about zero under its yield curve control (YCC) framework – no doubt showing that it can no longer stand idly by while its citizens deal with the rise in domestic prices. Apparently, even an economy famed for its secular stagnation – for which the term “Japanification” came about – was no longer immune to the inflationary pressures that have engulfed the globe. Notably, Japan’s CPI rates are at highs not seen for the last 30 years.

Figure 1: Japan’s inflation rates back to bubble-era levels Source: Bloomberg, DBS

Source: Bloomberg, DBS

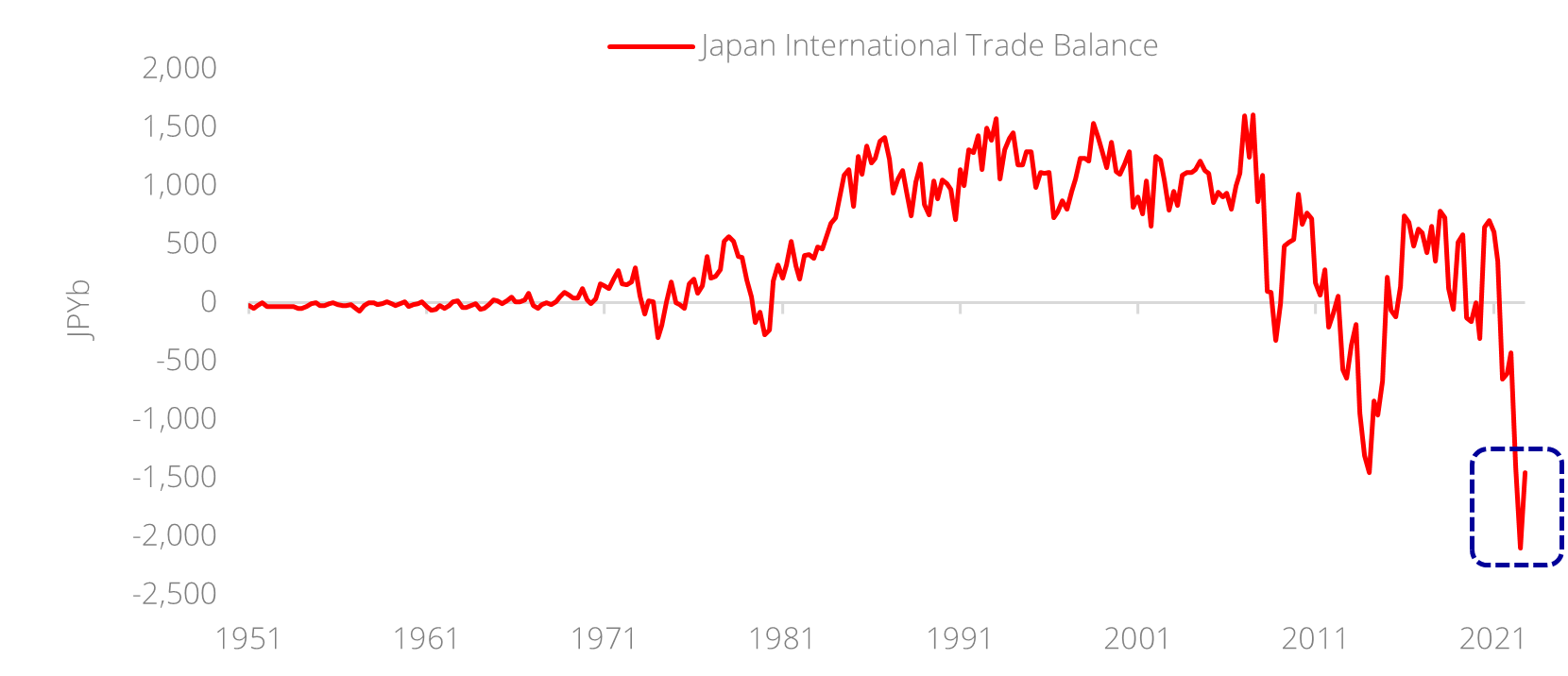

Policy at odds with reality. Such price pressures make the YCC policy – where the BOJ purchases whatever quantity of JGBs it takes to keep 10Y yields near 0% – look increasingly anachronistic; unsuited for the times they are in. As the rest of the world raced to tighten monetary policy, the BOJ worked in reverse; in effect sacrificing the JPY to support their bond markets and resulting in the c.30% decline of the JPY against the USD at its peak in 2022. While famed for being an export juggernaut in the 1980s, today’s Japan is more import reliant, and the weaker yen only stands to (a) raise imported inflation and (b) widen the already significant trade deficit observed in 2022.

Figure 2: Japan’s record trade deficit on surging energy imports Source: Bloomberg, DBS

Source: Bloomberg, DBS

The impending great unwind. The facts suggest that an exit of accommodative policy is not a matter of if, but when; given that it is no longer beneficial to have an ever-weakening yen. Yet it is difficult to imagine a stoppage or reversal of decades of QE without important financial consequences. To give perspective on the task at hand, consider that the US Fed is currently “only” reducing its balance sheet by USD95b a month (or USD1.14t a year, approximately 4.4% of annual GDP) to taper excess bank reserves. Given reserve balances of c.USD3.1t, this would take them c.33 months to bring said reserves to zero.

The BOJ, on the other hand, has amassed a gargantuan JPY451t in excess reserves. To normalise policy at the same rate as the US would imply the reduction of c.JPY164t in JGBs per year, a massive 30% of annual GDP – close to seven times the US amount in %-GDP terms. Put another way, should Japan begin normalisation immediately at the same pace as the US (in %-GDP terms), it would still take more than 18 years from today to reduce excess reserves to zero.

The unnoticed risk for bonds. It is no wonder then that policy change is consistently met with such inertia. That, however, does not absolve the fact that inflationary pressures continue to mount in the background, as large Japanese corporates are already planning sizeable domestic wage increments from this year onwards (e.g. Uniqlo, a Japanese casualwear brand announced pay increments of up to 40% for about 8,400 employees), introducing further threats of a potential wage-price spiral. We believe that the upward pressure on yields in Japan is an under-appreciated risk for fixed income investors, warranting caution on long duration exposure.

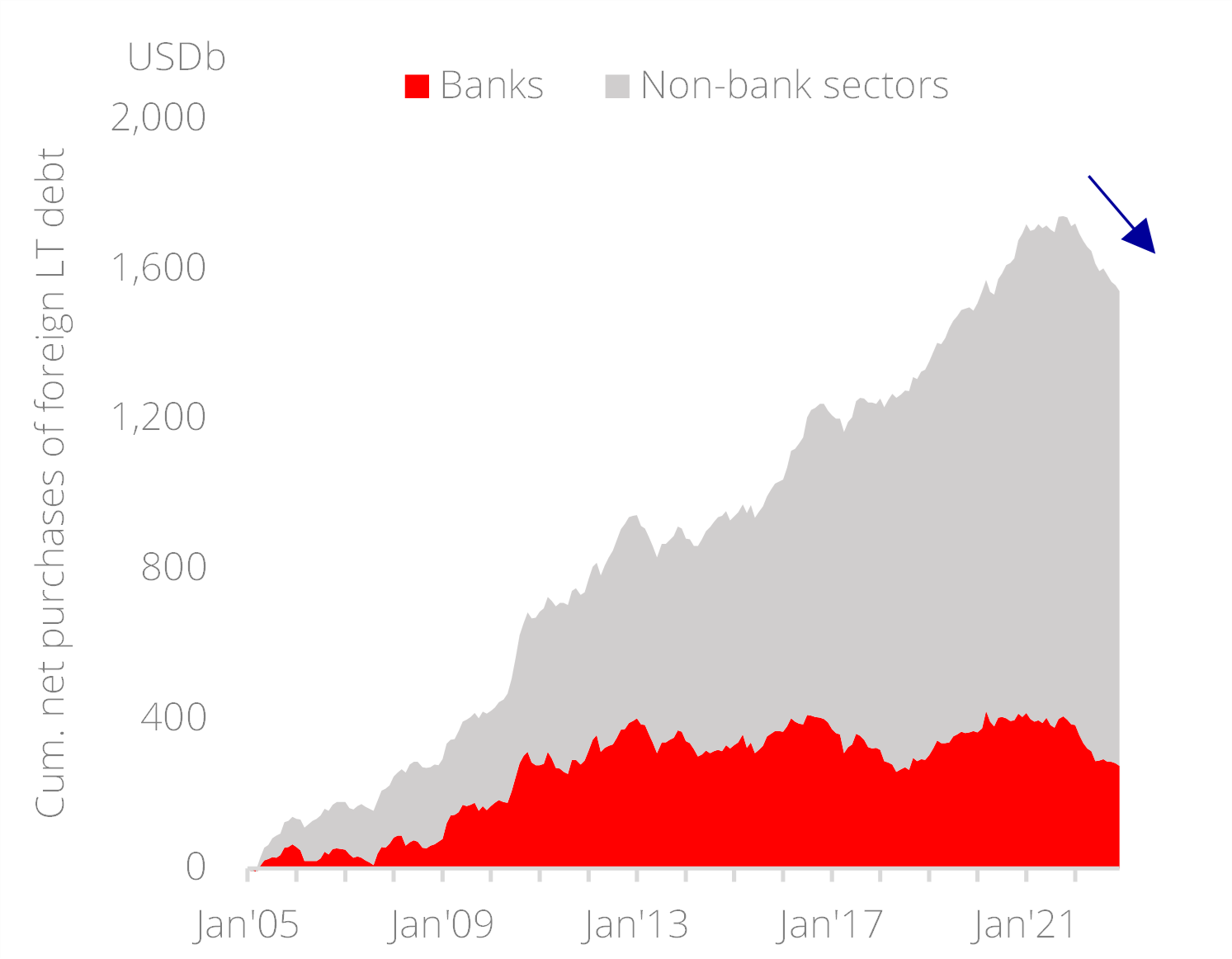

Figure 3: Japanese investor flows into foreign assets have reversed

Source: Ministry of Finance Japan, Bloomberg, DBS

Source: Ministry of Finance Japan, Bloomberg, DBS

Mrs. Watanabe no longer shopping abroad. Unlike the US, Japanese corporates/households have (a) accumulated large excess savings since the year 2000, and (b) had funneled such surpluses over the next 20 years into foreign assets, given that zero-bound domestic rates had forced Japanese investors to look offshore – leading to the country having the largest net international investment position (NIIP) in the world. With domestic rates now set to rise under the return of inflationary pressure, opportunities for yields onshore – for the first time in decades – would turn increasingly attractive, negating the need to invest in foreign assets. Already since 2022, we have observed such a pivotal shift in cumulative flows out of long-term foreign debt from private Japanese investors.

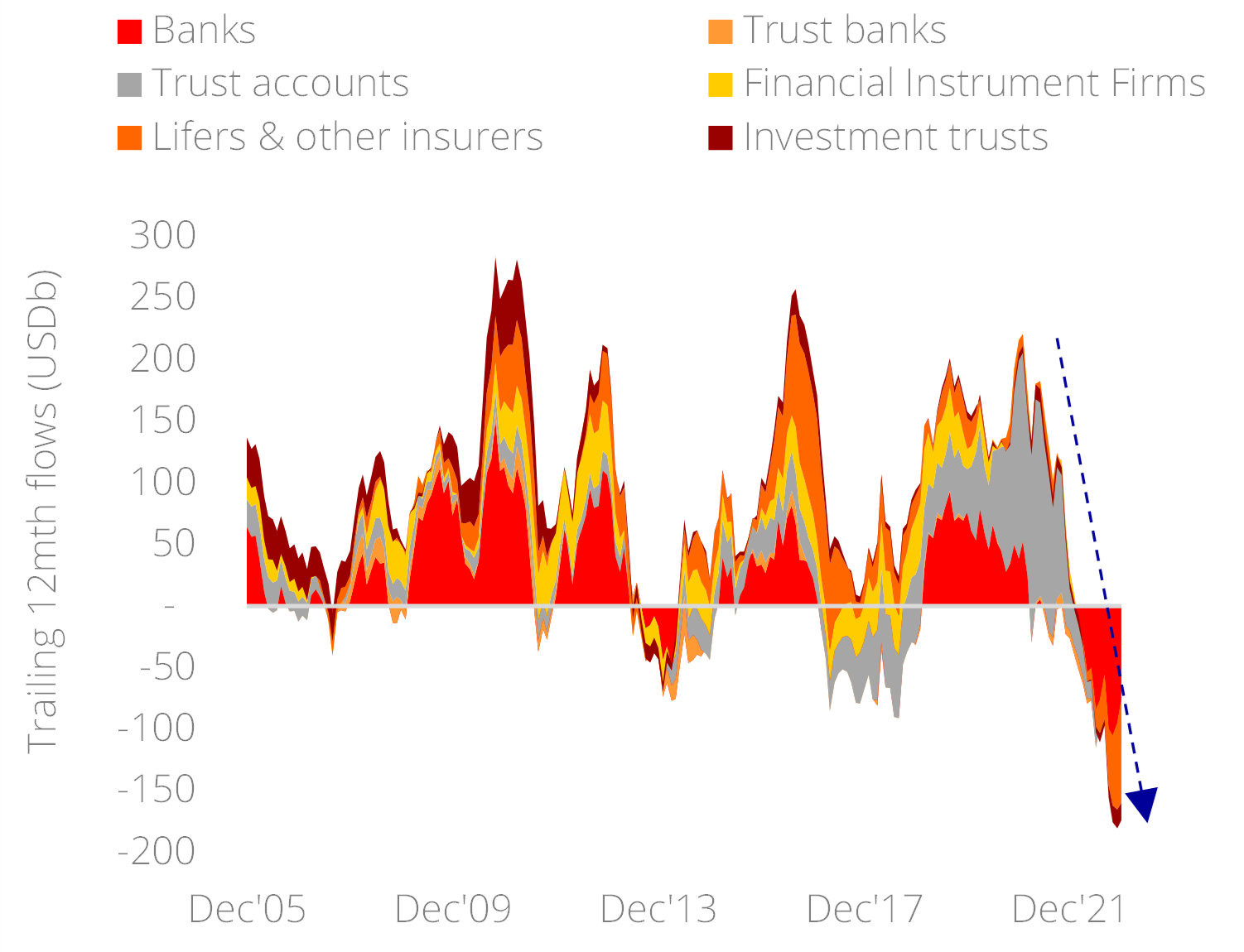

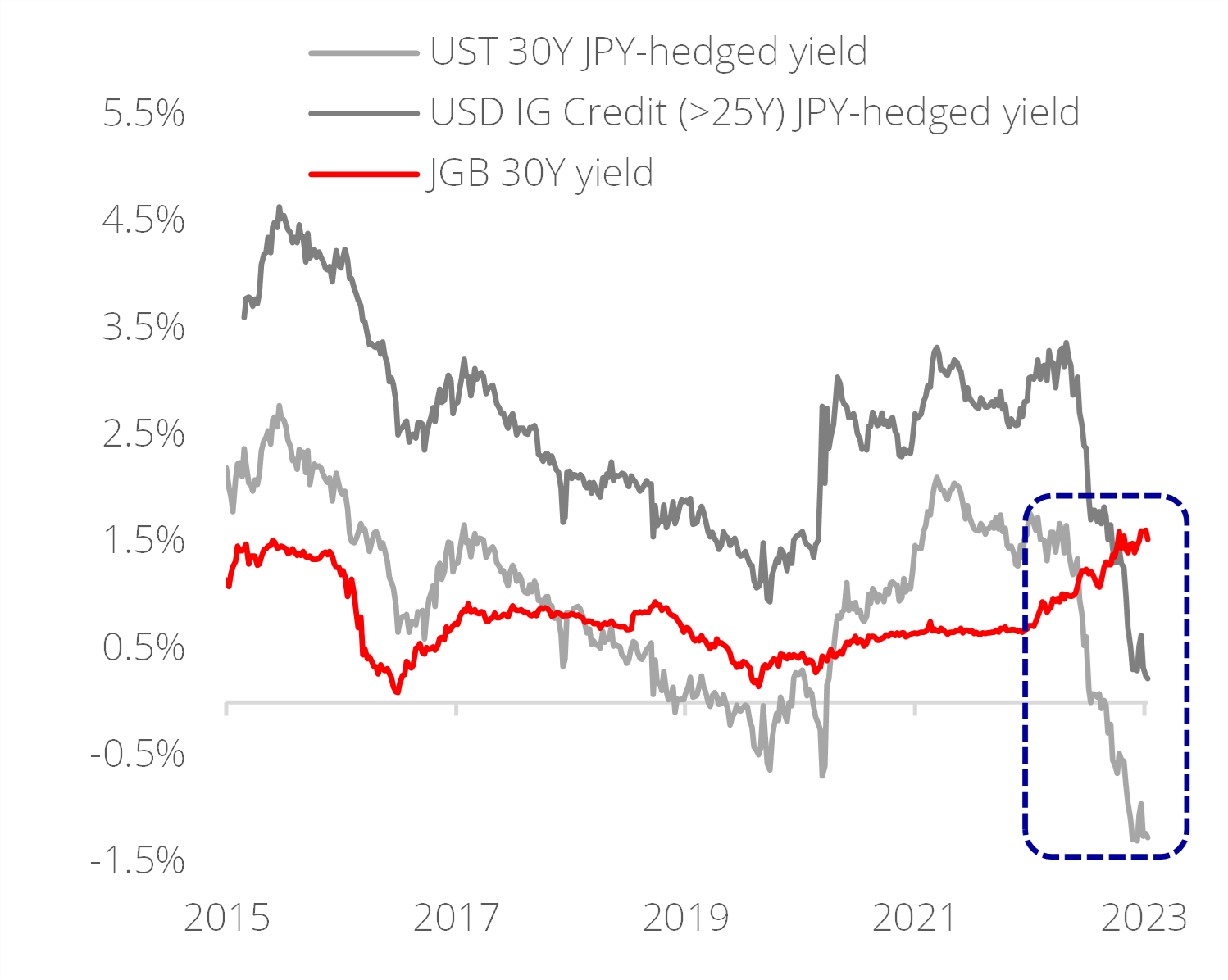

Higher costs of FX hedging. Another key headwind for Japanese flows could be that the costs of hedging foreign assets back to JPY has become exorbitant. A Japanese investor buying USD assets for example, faces hedging costs equal to the difference in cost of borrowing in USD versus JPY for a similar tenor, plus a premium (basis) that incentivises the lending of the dollars to the Japanese investor. The rapid rise in short-term US rates has now made it unprofitable to borrow dollars in the short term for most Japanese investors – to the extent that even currency-hedged USD IG credit yielded less than JGBs by end-2022.

Figure 4: Hedging costs are now punitive for Japanese investors

Source: Bloomberg, DBS

Source: Bloomberg, DBS

What are the implications? As investors had learnt from the Gilt selloff in the UK last year, rising yields can often cause accidents when assets need to be disposed as a form of loss mitigation. While the US yield curve is deeply inverted, for example, Japanese institutions holding long-duration US assets may be running losses on “negative carry” positions (cost of borrowing in the short end is higher than the yield on assets in the long end) and would de-risk from the more duration-sensitive foreign investments to unwind such positions in a major “fire-sale” scenario. Even without such extremes, it is likely that Japanese investors continue to allow the run-off of their foreign holdings to free up capital to invest onshore – diminishing the Japanese bid for global fixed income that the world had grown accustomed to in the post-millennium years.

The calm before the storm. The BOJ may have held its policy unchanged in the recent January meeting as a show of resolve, but underlying inflationary pressures ensure that the policy debate would remain hotly contested for the remainder of the year. There could be a chance that Governor Kuroda prefers to end his term come 8 April this year without further legacy-altering changes, but investors should not hold their breath.

We therefore encourage investors to not be complacent with duration risk in the interim. It is tempting for example, to purchase long-duration USTs as a recession hedge, but if that thesis is predicated on the Fed having to restart rate cuts/QE, we feel that gold would be (a) the better expression against such forms of monetary debasement and (b) is a better hedge for inflationary surprises. For yield investors, focusing on high quality credit in the 3-5Y segment is the sweet spot while such policy uncertainty remains at bay.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.