Related Insights

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

- Singtel15 Dec 2025

Markets may pay less attention to Fed Chair Jerome Powell at the December 10 FOMC meeting. The centre of gravity may already have shifted towards US President Donald Trump’s impending pick for Fed Chair, a decision he may announce around the turn of the year, months before Powell’s term ends in May 2026. Investors are increasingly focused on the emerging Shadow Fed rather than Powell’s short-term guidance. The futures market has started to reflect this transition, with rate cuts in 2026 being driven more by expectations of a new supply-side-oriented Fed Chair, weighing on the USD.

Against this backdrop, commodity currencies – AUD, NZD, and CAD – have outperformed in the first week of December. Markets view the Fed as having more cuts ahead in 2026, while its counterparts in Australia, New Zealand, and Canada may have finished with easing and signalling a high bar for additional cuts.

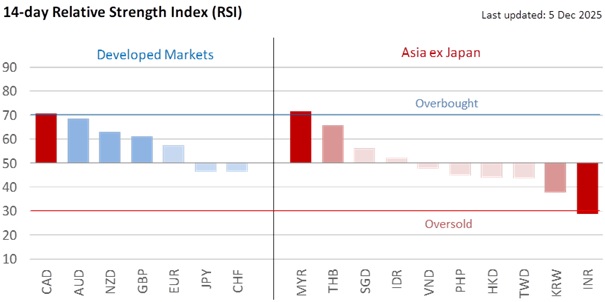

AUD has the strongest policy divergence story, with the futures market pricing in a possible 2026 hike. In contrast to the Fed, the Reserve Bank of Australia is prioritising inflation over jobs in its dual mandate. Both CPI and core inflation have risen above the RBA’s 2-3% target band, while the unemployment rate is slightly below the NAIRU, or the non-accelerating inflation rate of unemployment. During the Senate hearing on December 3, RBA Governor Michele Bullock said the private sector may be starting to take over from the public sector as the driver of economic growth. Bullock rejected allegations that the monetary policy was responsible for rising housing prices.

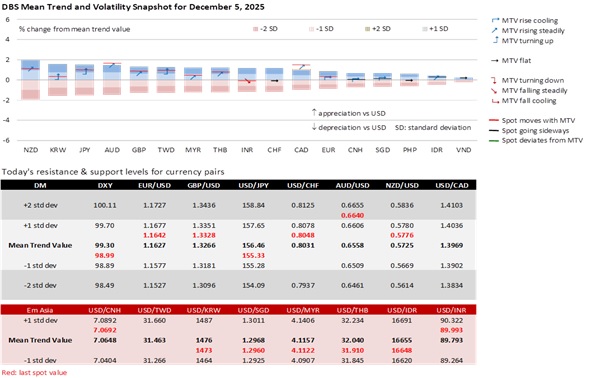

USD/CAD broke decisively below 1.40 last week to 1.3817, retracing some 50% of July-November’s rise. Following stellar Canadian jobs data, no one expects the Bank of Canada to mirror the Fed’s expected cut this week. In contrast to the soft US labour market, Canada’s unemployment rate fell to 6.5% in November, bucking the consensus for an increase to 7% from 6.9% in October. Apart from 275 bps of rate cuts since mid-2024, the Canadian economy is also supported by a fiscally stimulative budget. Hence, the BOC is unlikely to take any chances even though inflation has been near target. Look for the BOC to signal an extended pause at this Wednesday’s meeting. The OIS market is more hawkish and has started positioning for a possible BOC hike in late 2026. Look for any correction to reinstate USD/CAD shorts to September’s low of 1.3725.

NZD/USD rebounded from the year’s low of 0.5580 after the Reserve Bank of New Zealand cut rates and signalled a high bar for further easing at its November 26 meeting. Prospects for an extended pause lifted NZD to 0.5775 last Friday. Assuming her position on December 1, new RBNZ Governor Anna Breman was clear about restoring credibility to the monetary policy. Her appointment came after the departure of former governor Adrian Orr, who drew government criticism for losing control of inflation, prompting his resignation in March. With inflation higher at 3% in 3Q25, Breman will focus on returning it to 2% or the middle of the 1-3% target range. NZD/USD needs to break above 0.5785 (38.2% Fibonacci retracement level) to further advance to 0.5850 (50% Fibo).

Quote of the Day

“The best thing about the future is that it comes only one day at a time.”

Dean Acheson

December 8 in history

The Flag of Europe was adopted by the Council of Europe in 1955.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related Insights

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

- Singtel15 Dec 2025

Related Insights

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

- Singtel15 Dec 2025