- G3: The US economy is poised to end 2025 on a strong note, though the outlook for 2026 presents some areas of concern; market expects monetary policy divergence across the G3 at the December meeting

- India: India faces a challenging act at the December rate review, given the mix of strong growth print and record-low inflation

- Indonesia: Within-target inflation and softening export growth set the stage for a dovish BI; we maintain our call for an additional 75 bps of cuts by end-2026, to align policy with the government’s pro-growth stance

Related Insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

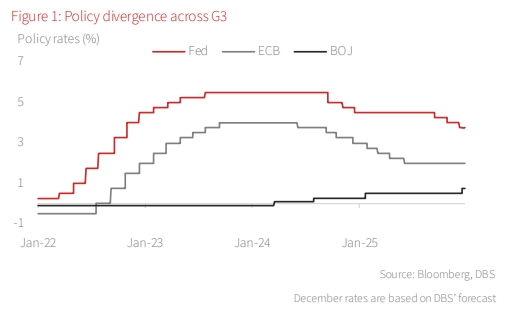

G3: Risks lurking underneath the US economy; policy divergence across G3. On the surface, the US economy has entered the final leg of 2025 with considerable strength. As per Atlanta Fed’s Nowcasting analysis, economic growth momentum is currently the highest seen this year. Durable goods orders, manufacturing PMI, retail sales, non-residential investment, and public spending trends point to above-trend GDP growth in 3Q25 and possibly in 4Q25. Our 2025 GDP growth forecast of 1.9% is characterised by substantial upside risk. The Fed may not be ultra-dovish (yet), but the market is confident that the path ahead includes lower rates and ample liquidity. But is the outlook paved with nothing but comfort? We are picking up several clues that suggest potential headaches ahead. First, labour market developments could pose risks to the consumption outlook. Second, financial sector stability issues could resurface in 2026. Lastly, inflation. Cost-of-living concerns dominated this year’s off-cycle elections and are unlikely to fade, especially if the Fed errs by keeping policy too loose. From tariff passthrough to immigration tightening that raises labour costs in services and construction, inflation could climb well past 3% and spoil the party in 2026.

Markets have shifted focus away from Powell’s comment that a December rate cut was not a forgone conclusion. Futures markets are now effectively pricing in an insurance cut as two factors converge. The latest ADP employment report –the final labour market indicator before the upcoming Fed meeting – showed a 32K job decline in November, compared to a revised 47K gain in October and a market consensus of 10K gain, underscoring further deterioration in the US labour market. Looking ahead, Trump is expected to nominate the next Federal Reserve chair in early 2026, with Kevin Hassett emerging as a leading contender. The prospect of a “shadow Fed” forming before Powell’s term ends in May 2026 raises concerns about policy continuity and central bank independence.

In contrast, markets are increasingly confident that the European Central Bank (ECB) has ended its easing cycle. Unlike the Fed, the ECB faces no equivalent leadership uncertainty. The Governing Council has emphasised that it is more comfortable pausing than risking premature easing after halving the deposit facility rate by 200 bps to 2%, a level broadly aligned with inflation slightly above target. Eurozone CPI inflation rose to 2.2% y/y in November from 1.9% in May, while the unemployment rate remained near record lows.

For Japan, Bank of Japan (BOJ) Governor Ueda hinted that December’s meeting is live. He appears less concerned about tariff impacts and is focusing more on how a weak JPY could boost inflation. Market participants were caught off guard and quicky raised the odds of a BOJ hike to above 80%.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

Related Insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025