- US: Backed by tech investments, fiscal impetus, and impending Fed easing amid a cooling job market, the US enters 2026 largely recession-proof; still, underlying concerns about cyclical strength, central bank independence, and a strained fiscal outlook warrant close watching

- Japan: China-Japan tensions remain manageable for now, with limited immediate economic impact expected; however, China’s broader restrictions could increase risks; better-than-expected 3Q25 GDP supports a BOJ rate hike, while fiscal stimulus and the October CPI should guide the timing

- Thailand: We project a slowdown in Thailand’s 2026 GDP growth, driven by anticipation of rising domestic political uncertainty in 1H26; the BOT is expected to stay dovish, bringing policy rate to 1% in 2026

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

US: No Recession, but the best is behind. September’s nonfarm payroll (NFP) surprised to the upside at 119k (vs. 51k expected). However, the unemployment rate ticked up from August’s 4.3% to September’s 4.4%. Despite a higher labour force participation rate, job opportunities could not keep pace. The next official labour print, the November NFP, will be released six days after the 10 Dec FOMC meeting. In the absence of official NFP data, investors will likely lean on alternative indicators to gauge labour momentum. Weekly ADP employment has now contracted for two consecutive weeks. We see the following downside risks for the job market. First, government shutdowns could have dragged overall hiring. Notably, the government and quasi-public sectors like education and health care contributed to 90% of NFP gains over the past nine months. Second, retail, leisure, and hospitality employment could also be at risk. Against this backdrop, the Fed remains on track to deliver another 50 bps of cuts by end-2026.

Amid the debate over monetary policy easing, it is striking that many aspects of the US economy and financial markets look relatively healthy. While we recognise sporadic signs of weakness, we remain firmly in the no-recession camp. We forecast real GDP growth of c.1.5-2% this year and the next.

The US economy is leading the world in a historic spike in tech investments, primarily related to data centres and hardware for training and executing Large Language Models. With hundreds of billions spent this year and more in the pipeline for years to come, this secular investment boom is likely to be as important a growth contributor as consumption, traditionally the mainstay of the US economy. The electricity needs of the tech sector are surging, driving a spike in investment in power generation. From renewables to natural gas, small nuclear reactors to oil, the US accounts for 25% of global energy investment, and all signs point to further momentum in this sector in the near and medium term.

Various tax benefits for the household and corporate sectors stipulated in the recently passed One Big Beautiful Bill will be trickling through the US economy in the coming quarters. Additionally, tax refunds starting January 2026 could be as much as 20% higher for 70% of American households. This would likely be of substantial support for consumption and overall demand.

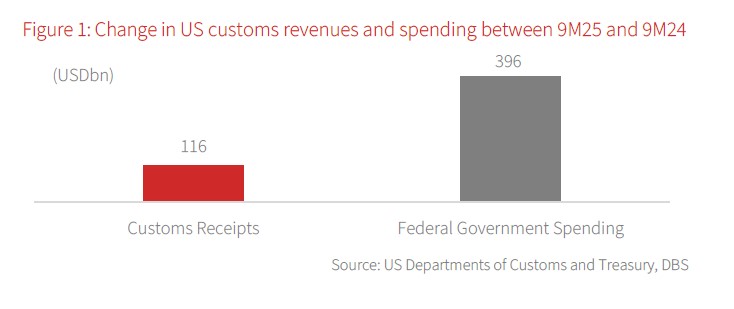

Federal government spending is up by nearly USD400bn so far this year, while tariff revenues have risen by USD116bn. Monthly tariff collections have stabilised at just under USD30bn. Assuming this collection rate continues, the US could collect over USD350bn annually in tariff revenues going forward, amounting to 1% of GDP. Unfortunately, even after this herculean and destabilising effort, the US fiscal position will remain challenging, with spending increases likely to outpace revenue growth. The biggest offset to tariff revenues will come from significant tax cuts in the pipeline, as part of the mega fiscal measures passed in 2025.

After proving stronger than feared earlier this year, the US is stepping into 2026 with little fear of recession but a broader set of concerns about cyclical strength and erosion of institutional integrity. The best times may well be behind us.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025