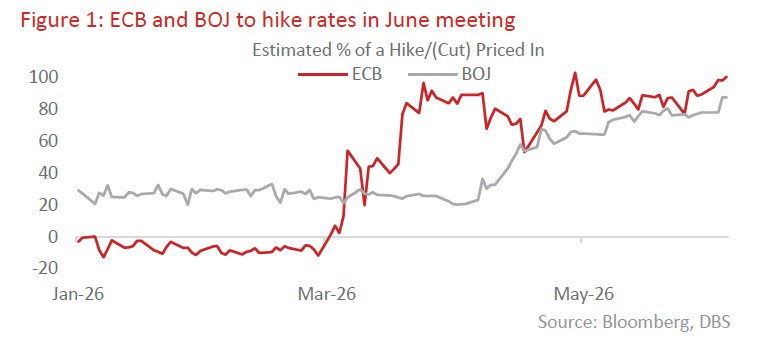

- G3: As the Fed navigates its internal transition, the ECB and BOJ are expected to hike rates at their upcoming June meetings; with the Middle East situation still in limbo, focus shifts to labour market data due this Friday

- Eurozone: May inflation rose to 3.2% y/y, above the official target, with an uptick in core readings; we expect a 25 bps rate hike at the June meeting, with policy guidance to stay cautious and hawkish

- Japan: BOJ has issued clear signals pointing toward a potential rate hike at its upcoming June meeting; we bring forward our long-held 25 bps rate hike call from July to June

- South Korea: BOK turned hawkish at its May meeting, with accelerating May CPI supporting this shift. We maintain our forecast for a 25 bps hike in 3Q26, as early as the July meeting, with another potential 25 bps hike in 4Q26

Related Insights

- US Equities: Riding the AI Capex Cycle via US Financials17 Jul 2026

- Research Library17 Jul 2026

- FX Tactical Ideas: USD Consolidates17 Jul 2026

G3: Still muddling through? As we move into Jun 2026, optimism around a "muddle-through" peace deal in the Middle East remains elusive, while the macroeconomic landscape braces for a highly anticipated Fed transition. Focus is on the 16-17 Jun FOMC meeting, Kevin Warsh’s debut as Fed Chair, as he walks a tactical tightrope. On one hand, President Trump has made his preference for lower interest rates unmistakably clear. On the other, April's CPI inflation print ticked up to 3.8% y/y (with whisper numbers pointing toward a breach of 4% if energy pressures persist). As the Fed navigates its internal transition, other major central banks are facing their own tactical dilemmas. June has become a month of hawkish recalibration amid the lingering Middle East conflict, which has kept global energy costs elevated. The European Central Bank (ECB) is expected to deliver an insurance hike to counteract inflation driven by energy shocks. Look for the deposit facility rate to increase by 25 bps to 2.25% at its 11 Jun meeting, alongside an upward revision to its inflation outlook. In Japan, we now expect the Bank of Japan (BOJ) to hike interest rates by 25 bps to 1% at its June meeting, brought forward from July.

With the situation in the Middle East still in limbo, focus shifts to this week’s labour market data. Jobless claims (initial and continuing) have remained low in recent weeks, pointing to continued resilience in the US economy. JOLTS job openings rose to 7.6mn (consensus: 6.9mn). It is therefore unsurprising that consensus is keeping an upbeat view on the official data due on Friday: nonfarm payroll is expected to come in at 85k (marking a third consecutive positive print), while the unemployment rate is projected to hold steady at 4.3%.

Concurrently, the Office of the US Trade Representative (USTR) unveiled a new legal pathway to reinstate country-specific tariffs. Following legal setbacks — including a Supreme Court ruling against broad IEEPA tariffs in February and a Court of International Trade decision striking down Section 122 tariffs last month — the Trump administration has shifted to Section 301 of the Trade Act of 1974 as its latest trade enforcement tool. The USTR identified 60 trading partners for allegedly failing to adequately restrict goods produced through forced labour. The proposal would impose an additional 10% tariff on 16 economies, including the EU, UK, Canada, Mexico, and Taiwan, for inadequate enforcement of existing bans, and a further 12.5% on 44 economies, including China, Japan, South Korea, India, Australia, and Singapore. Markets initially saw this as an escalation in trade tensions. However, the proposal must still complete the Section 301 process, with public comments due by 6 Jul, and hearings to start on 7 Jul. The administration appears to be fast-tracking the timeline so new tariffs can take effect before the temporary Section 122 tariffs expire on 24 Jul.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- US Equities: Riding the AI Capex Cycle via US Financials17 Jul 2026

- Research Library17 Jul 2026

- FX Tactical Ideas: USD Consolidates17 Jul 2026

Related Insights

- US Equities: Riding the AI Capex Cycle via US Financials17 Jul 2026

- Research Library17 Jul 2026

- FX Tactical Ideas: USD Consolidates17 Jul 2026