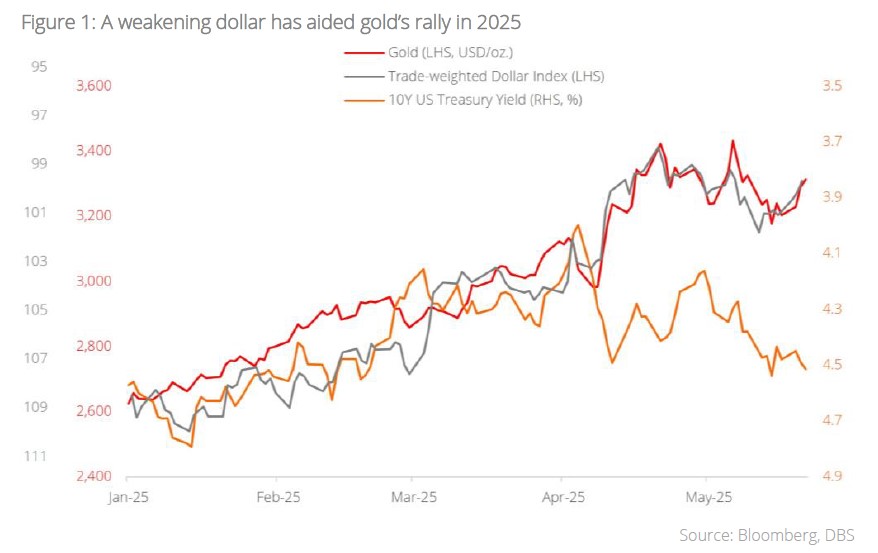

- Gold continues its stellar bull run, reaching a new all-time-high of USD3,500/oz. on 22 Apr amid trade war worries

- Continued central bank reserve diversification and robust investor demand to buoy gold in new era of heightened risk and uncertainty

- Growing recession and stagflation risks add to gold’s appeal

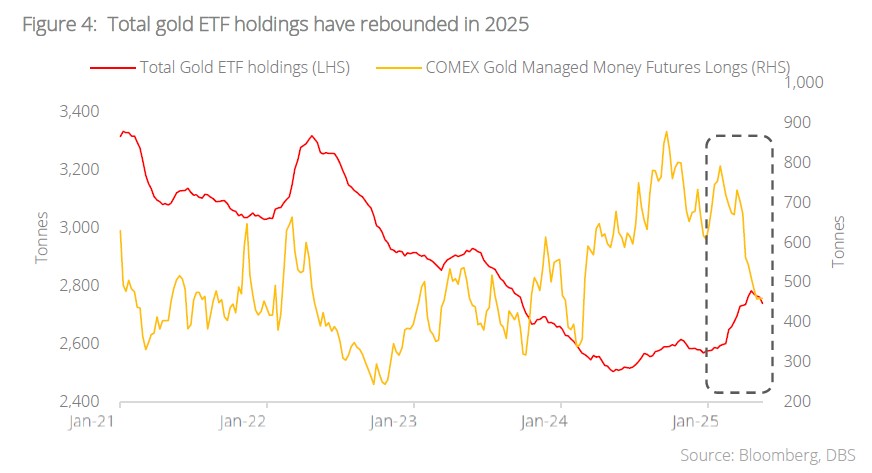

- Gold ETF flows have sharply rebounded on a YTD basis

- Raise TP to USD3,765/oz. by year-end (previously USD3,330/oz. by 1Q26)

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Running circles around analyst predictions. By now, it is well established that gold has been in a consistent bull market for the better part of the last three years. We have covered, in past publications – “Further Highs for Bullion as Trade War Fears Mount” (Feb 2025); “A Glittering Haven” (Apr 2025) – the various tailwinds for the precious metal. These include geopolitical uncertainty, a widening US fiscal deficit, de-dollarisation, and fiat currency debasement among others. For 2025, the clear consensus on the street was bullish gold, with upside far outweighing potential downside. Despite this, few could have predicted gold’s prodigious rally in April. It was as if gold had suddenly floored the figurative gas pedal and kicked into a higher gear, peaking at an intraday high of USD3,500/oz. on 22 Apr. Having said that, the key question remains: how high can gold go? The DBS CIO Office is revising our gold target price to USD3,765/oz. by 4Q25 (previously USD3,330 by 1Q26) against the backdrop of accelerating tailwinds under a changing world order.

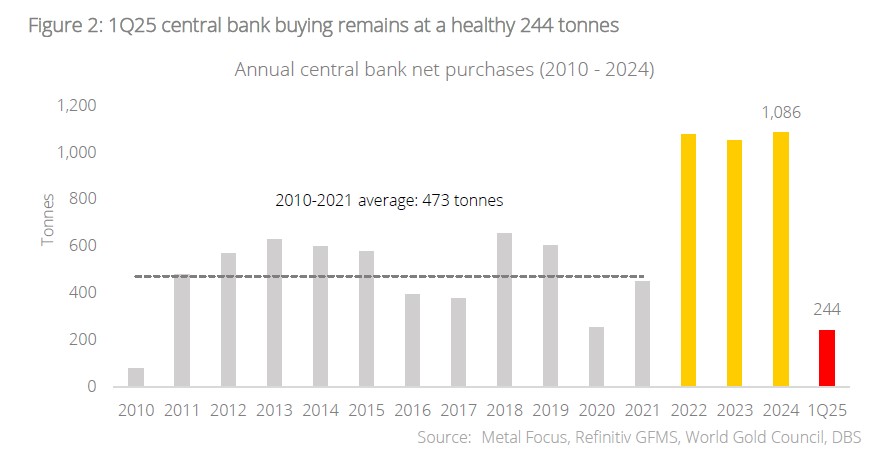

Central bank and investor demand are key to gold’s continued rise. We have long opined that one of the key tailwinds for gold in this new era is central bank and investor gold buying on the back of geopolitical uncertainty and fragmentation. This not only provides a steady structural demand for gold in the long run, but also maintains a price floor and caps downside risk for the precious metal during times of broad de-risking, as was illustrated post “Liberation Day” in April. We performed a linear regression analysis (using quarterly data from 2017 to 1Q25) of the q/q change in gold price against the combined quarterly central bank and investment (bar, coin, and ETF) demand for gold, and found that it takes approximately 600 tonnes of quarterly demand to produce a quarterly increase of 6.4% in gold prices. This is one of the key assumptions underpinning our revised target price of USD3,765/oz. by 4Q25. The average quarterly central bank and investment demand for gold per quarter was roughly 500 tonnes from 2017 to 1Q25, and we believe that the assumption of demand increasing to an average of 600 tonnes per quarter is fairly justified given how: i) the geopolitical landscape has deteriorated under Trump, which will further spur central bank buying; and ii) gold as a percentage of international reserves remains at roughly 21% (as at Feb 2025), well below the historical 54-year average of 29%. On point (ii), the percentage falls drastically to 11% if US, Germany, France, and Italy (countries with the largest gold reserves) are excluded from the calculation, highlighting significant headroom for reserve diversification for central banks from other nations such as China, Poland, Turkey, Singapore, India, and others.

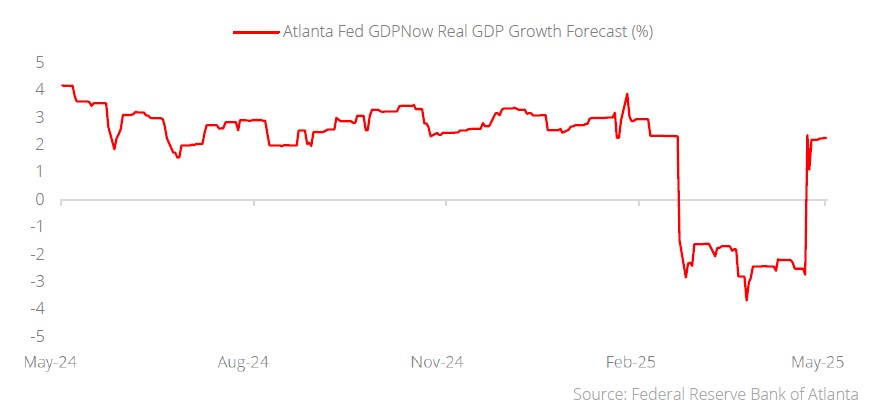

Recession and stagflation risks at play. Another reason that the assumption of increased investment demand for gold is justified is that the macroeconomic backdrop has weakened thanks to the Trump administration’s tariffs and the ongoing US/China trade war. The US recession probability, as measured by the 3-month and 10-year US Treasury yield spread, while below its 2023 peak, remains at a substantial 30.5% (as at Apr 2025). The Atlanta GDPNow forecast also reflected uncertain economic conditions earlier this year, hinting at the possibility of recession and stagflation. Against this backdrop, we believe rate cuts are on the cards, which should benefit gold significantly. Yes, there is a possibility of tariffs being called off and successful trade deals being negotiated, and that would potentially derail this tailwind for gold. But as long as Trump remains in office, the uncertainty factor remains high, regardless of subsequent trade and policy developments that take place. We maintain that gold is one of the best hedges that investors can hold in their portfolios. It protects not only against recession and stagflation risks, but also against a myriad of others, including fiat currency debasement, de-dollarisation, and other US policy-related risks.

A sustained rebound in gold ETF demand. The favourable backdrop for gold has seen gold ETF demand rebound in 2025. ETF demand for 1Q25 was 227 tonnes, the highest it has been since 1Q22. This positive momentum continued as April saw a further 115 tonnes of ETF demand, the strongest inflow since Mar 2022, taking the total YTD demand to 342 tonnes. Despite the surge however, total gold ETF holdings remain 10% below the month-end peak in Oct 2020, suggesting that this rally still has room to run. In terms of regional flows, Asia and North America dominate on a YTD basis. Unsurprisingly, gold trading volumes also boomed in April by 48% on a m/m basis. This was for both OTC (LMBA) and exchange-traded (COMEX and Shanghai Futures Exchange) activities. Nonetheless, long positions held by money managers fell in April due to profit-taking amid record high gold prices.

New target price: USD3,765/oz. by 4Q25. As we delve into a new era for gold, structural tailwinds remain firmly in place, and we see asymmetric risk-reward for the asset class; limited downside with plenty of upside yet to materialise. In this new era, we see gold prices buoyed by strong central bank and investor demand amid macroeconomic and geopolitical uncertainty, recession/stagflation risk, and ongoing monetary debasement concerns. Even during episodes of relative dollar and rate strength, gold prices should remain fairly supported as heightened risk and uncertainty should encourage strong dip-buying behaviour. Accordingly, we are upgrading our target price for gold to USD3,765/oz. by 4Q25 (previously USD3,330 by 1Q26) based on the assumption of approximately 600 tonnes of combined central bank and investment demand per quarter among other factors.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Related Insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025