Related Insights

- FX Tactical Ideas: USD Supported by Higher Yield22 May 2026

- US Equities: Navigating Rising Yields & Concentration Risks22 May 2026

- Hang Lung Properties22 May 2026

Global: IMF flags rising risk of stagflation. With Brent crude prices holding mostly below USD100/bbl over the past week, markets are now pricing in a diplomatic resolution between the US and Iran amid reports of ongoing talks. Despite the failure of the first round of talks in Islamabad, President Trump announced a drastic policy shift by ordering US Navy to begin blockading the Strait of Hormuz, interdicting vessels in international waters that have paid a toll to Iran for safe passage in the Strait. This move has strengthened the resolve of EU nations and China to push for a diplomatic solution. Concurrently, markets are now signalling that a resumption of talks is the better path for US policymakers to pursue.

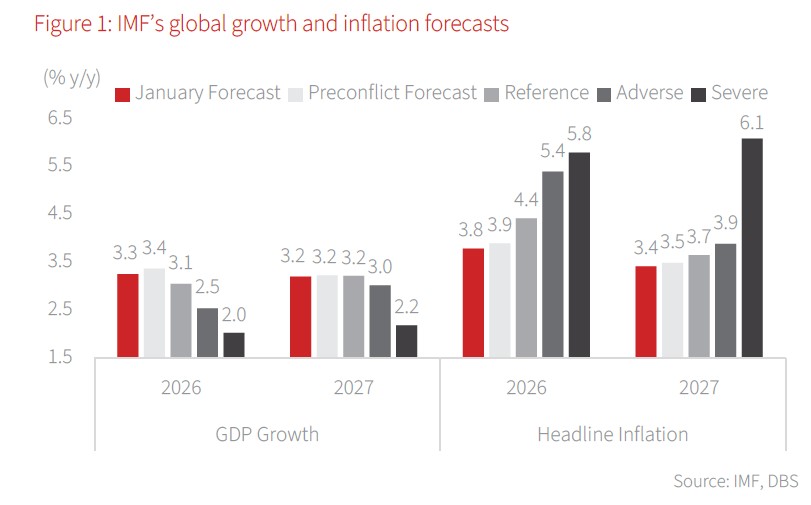

The International Monetary Fund’s (IMF) latest World Economic Outlook, released on 14 Apr, flagged rising global stagflation risks from energy shocks and framed the outlook through growth and inflation scenarios. In the ‘reference’ case of a short-lived conflict, the global growth forecast has been revised down to 3.1% y/y in 2026 from a pre-conflict estimate of 3.4%, while the headline inflation forecast was raised to 4.4% from 3.9%. The IMF Chief Economist cautioned that an ‘adverse’ case is increasingly plausible: a larger and more persistent oil-price spike (leading to average oil prices of USD100/bbl in 2026; USD75/bbl in 2027) would drag 2026 growth down to 2.5% and lift inflation to 5.4%. In a ‘severe’ scenario with greater damage on regional energy infrastructure (USD110/bbl in 2026; USD125/bbl in 2027), growth in 2026–27 could fall to c.2.0%, with inflation rising to c.6.0%.

Meanwhile, China’s cost-push inflation concerns appear somewhat overstated. March CPI and PPI prints remain relatively contained compared with those of other major economies. A diversified energy mix helps cushion cost pressures, with renewables and nuclear accounting for a larger share of energy consumption than oil.This relative resilience in energy supply should help support export performance. March’s weak trade data should be interpreted with caution, as base effects are distorting the signal. A late Lunar New Year in 2026 delayed the resumption of factory activity into March, while Mar 2025 exports were exceptionally strong due to front-loading ahead of the US ‘Liberation Day’ in April that year. High-frequency indicators such as port throughput (excluding oil and gas carriers) have remained broadly stable at around 60mn tonnes per day into April, suggesting that underlying trade momentum has not materially deteriorated.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- FX Tactical Ideas: USD Supported by Higher Yield22 May 2026

- US Equities: Navigating Rising Yields & Concentration Risks22 May 2026

- Hang Lung Properties22 May 2026

Related Insights

- FX Tactical Ideas: USD Supported by Higher Yield22 May 2026

- US Equities: Navigating Rising Yields & Concentration Risks22 May 2026

- Hang Lung Properties22 May 2026