Related Insights

- FX Tactical Ideas: USD Supported by Higher Yield22 May 2026

- US Equities: Navigating Rising Yields & Concentration Risks22 May 2026

- Hang Lung Properties22 May 2026

Global: Ceasefire with caveats. We have reached a temporary, conditional de-escalation in the Middle East conflict as US President Donald Trump agreed on a two-week ceasefire until 22 Apr, on the condition that Iran reopens the Strait of Hormuz. The market has clearly recognised that this choke on energy-related commodities can be undone relatively quickly. Even if there is no deal, a ceasefire that would allow ships to transit the Strait safely would go a long way towards easing shortage fears (especially across Asia). War premiums eased across the board with Brent/WTI crude oil prices falling below USD100/bbI, reflecting easing concerns over supply destruction.

While there will almost certainly be more volatility ahead, this episode could mark the beginning of the end of the Middle East situation, as far as the market is concerned. The economic impact on interest rates should also be considered. Inflation is likely be elevated for some time, which should constrain aggressive bets on Fed easing. US March CPI is due on 10 Apr, while Eurozone inflation rose to 2.5% y/y in March from 1.9% in February, according to preliminary data – driven in part by a sharp surge in global energy prices amid tensions in the Middle East.

Given that the energy inflation is clear. there is a gradual broadening of the crisis as price pressures move downstream. As production processes rely heavily on petroleum products and natural gas, prices of chemicals, plastics, and fertiliser have already jumped 20-70%. The impact on the travel industry, from flight availability to airfares, is evident. Agriculture and manufacturing will follow. Moreover, electronic prices, already heating up, will have one more catalyst from energy inflation.

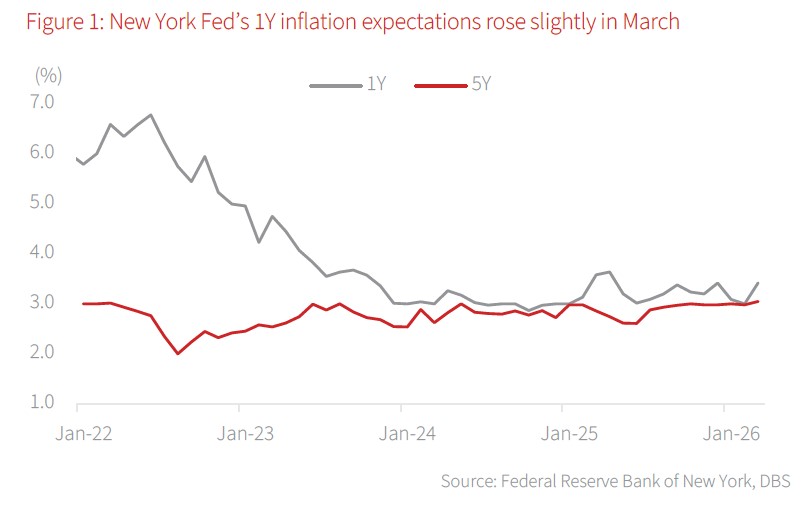

At the same time, the Fed’s “wait and see” stance should keep 2026 hike expectations off the table. The New York Fed reported that one-year inflation expectations increased to 3.42% in March, below expectations for a rise to 3.50% from 3.00% in February. Five-year inflation expectations held steady at 3%. New York Fed President John Williams downplayed oil-driven headline inflation, citing limited underlying inflation pressure in a “low hire, no hire” labour market. His expectation that the war will add 0.1-0.2% to core inflation aligns with the March Summary of Economic Projections, which revised the 2026 core PCE inflation forecast to 2.7% from 2.5%.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- FX Tactical Ideas: USD Supported by Higher Yield22 May 2026

- US Equities: Navigating Rising Yields & Concentration Risks22 May 2026

- Hang Lung Properties22 May 2026

Related Insights

- FX Tactical Ideas: USD Supported by Higher Yield22 May 2026

- US Equities: Navigating Rising Yields & Concentration Risks22 May 2026

- Hang Lung Properties22 May 2026