- Recent advancements in AI (led by Claude) suggests greater disruption to the SaaS model is on the table

- By automating tasks across multiple applications, AI reduces vendor lock-in, erodes pricing power, and lowers barriers for smaller competitors

- Large-cap software earnings were mixed, with Microsoft delivering strong growth, while SAP and Salesforce reported results broadly in line with expectations

- Integrated platform players are best positioned to embed AI natively, maintain pricing power, and capture value across multiple layers

Related Insights

- Singapore Equity Picks26 May 2026

- Europe Equities26 May 2026

- Japan Equities26 May 2026

AI is reshaping the SaaS playing field. Recent advancements from Anthropic (from Claude Cowork to new computer use capability) suggest greater disruption to the SaaS model is on the table (though not outright displacement). We see intensifying competition and a gradual erosion of pricing power for SaaS vendors. By abstracting away the user interface and enabling AI agents to operate across multiple applications, AI reduces vendor lock-in and weakens the control that platforms such as Salesforce and SAP have historically exerted over workflows. This could allow “challenger SaaS players” to use AI to replicate functionality at a lower cost. At the same time, Gartner’s timeline for AI agents performing multiple tasks across multiple applications by 2028 seems to have accelerated materially, compressing the window for incumbents to respond. While systems of records should remain intact and large platforms are unlikely to be displaced, we expect growth to moderate as pricing power declines. In such an environment, we favour integrated platform players that retain control over the broader ecosystem which underpins AI-driven workflows.

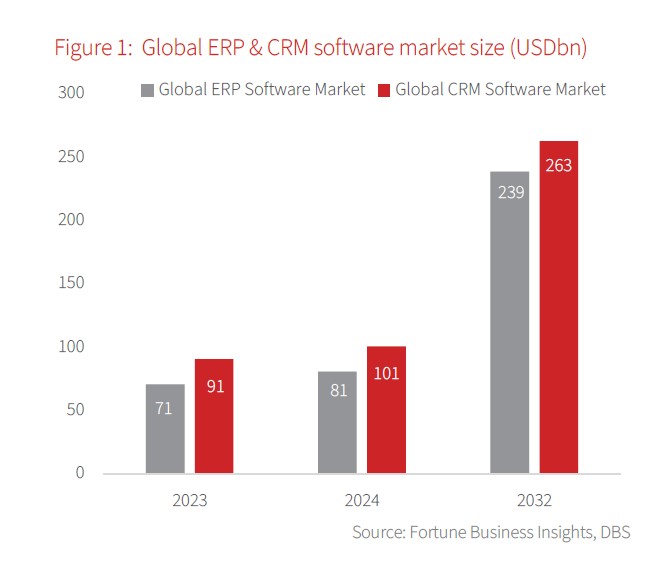

Mixed earnings across large-cap software in latest quarter. Microsoft delivered a strong 2Q26, with revenue up 17% y/y and operating income rising 21% y/y, ahead of expectations. Alphabet’s 4Q25 revenue increased 18% y/y, exceeding consensus, while non-GAAP operating profit increased by 23% y/y led by Google Cloud’s EBIT margin expanding to 30% from around 18% in 4Q24. In 4Q25, SAP reported revenue growth of 3% y/y, slightly below consensus, while non-IFRS operating profit rose 16% y/y, modestly above expectations, with margins expanding 4.5 %pts to 28.3%. Salesforce’s 4Q26 revenue grew 12% y/y, broadly in line with consensus, though operating profit fell short, reflecting a 150 bps y/y margin decline. Looking ahead, SAP expects FY26 cloud revenue growth of 23 – 25% y/y, Salesforce targets FY27 revenue of USD45.8 – 46.2bn (+10 – 11%), Microsoft guided 3Q26F revenue of USD80.7 – 81.8bn (+15 – 18%), and Alphabet guided FY26F capex at USD175 – 185bn, up around 90–100% y/y on AI and infrastructure demand.

We view recent AI developments as piling pressure on SaaS pricing power, with integrated platforms best positioned. While negatives are priced in for big SaaS players such as SAP and Salesforce, a clear picture may not emerge in 2026. We view the SaaS pricing model as undergoing a structural shift from traditional seat-based subscriptions toward hybrid monetisation. While per-user pricing still accounts for around 54% of vendors, AI-driven productivity gains (accelerated by advancements from Anthropic) are likely to reduce seats per workflow, weakening a key expansion lever. While we do not expect LLM players like Anthropic to challenge SaaS players directly, incumbent SaaS vendors could end up losing market share to SaaS players offering AI-native functionality at a lower price. In contrast, integrated platform players such as Microsoft and Alphabet are better positioned to capture value across multiple layers given their deep integration across the enterprise stack. Alphabet stands to benefit the most from its recent innovation announced in late March, which could drive around a 20 – 35% reduction in total memory per query.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Singapore Equity Picks26 May 2026

- Europe Equities26 May 2026

- Japan Equities26 May 2026

Related Insights

- Singapore Equity Picks26 May 2026

- Europe Equities26 May 2026

- Japan Equities26 May 2026