- Big Tech and surrounding ecosystem plays fit the characteristics of Quality Growth-at-a-Reasonable-Price (Q-GARP)

- The pipeline of innovation and new technologies that is continually reshaping the world is also bolstering the attractiveness of tech-investing

- Global IT expenditure will remain robust; total addressable market to reach USD5.3t by 2025

- DBS CIO Office continues to be constructive on global technology, with emphasis on Big Tech and sector leaders

Related Insights

- Digital Assets Update 2Q24: Base broadening14 May 2024

- BNP Paribas SA14 May 2024

- India rates: Macro sweet spot backs RBI’s comfortable hold 14 May 2024

No stopping this technology train. The CIO Office has long been constructive on global Technology and Big Tech. Despite shaky investor sentiment during the relentless Fed rate hiking cycle in 2022 and 2023, we maintained the view that the Technology sector would make a comeback on the bases of robust earnings growth, balance sheet strength, and structural criticality. We refuted opinions that higher rates would hurt Big Tech through tighter funding conditions, and instead argued that Big Tech companies were mostly sitting on net cash positions in their balance sheets even before the pandemic. Such financial strength has enabled them to weather a higher rate environment, capitalise on high savings rates, and initiate value-accretive M&A transactions. We also contested the notion that higher rates will suppress end demand, citing the emergence of artificial intelligence (AI) as a growth catalyst that would usher in a new growth paradigm for Big Tech companies, many of whom form the structural backbone of this nascent technology. Additionally, Big Tech companies have further cemented their leadership in the past two years, establishing authority in a growing number of tech-related verticals through innovation and inorganic growth. In hindsight, this series of contrarian calls has panned out well, with Big Tech delivering a striking performance of c.+96% from October 2022 to January 2024.

Figure 1: Big Tech has beaten the market and looks poised to continue its outperformance

Source: Bloomberg, DBS

Expensive but not astronomical. Despite general concerns of the relatively higher valuations of Big Tech and Technology companies compared to the broader market, we believe that such valuations are largely justified. Quality investments that display both robust growth prospects and strong defensive moat characteristics — as many of the Big Tech names do — do not come cheap but are worth the price. This combination of growth and true safety is something that is rare in equity investing, and accordingly the markets have priced in a significant, but in our view reasonable, premium for such companies.

Figure 2: Growth and quality justify premium valuations

Source: Bloomberg, DBS

We believe Big Tech will continue to be a bright spot within the Equity space, buoyed by multiple catalysts listed below.

Catalyst 1: Semiconductor recovery in sight. Semiconductor chipsets form the core foundation of most technology today and is a good barometer of the upstream technology sector. After a year-long slowdown, semiconductor sales to China and US have passed the trough in mid-2023 on the back of a stable recovery driven by new demand from AI and related services. We believe this represents a turning point for the sector and suggests that inventory issues are gradually being resolved. Coupled with signs that demand is bottoming, we will likely see a further recovery across the semiconductor sector moving forward.

Figure 3: Global semiconductor sales rebounding

Source: Bloomberg, DBS

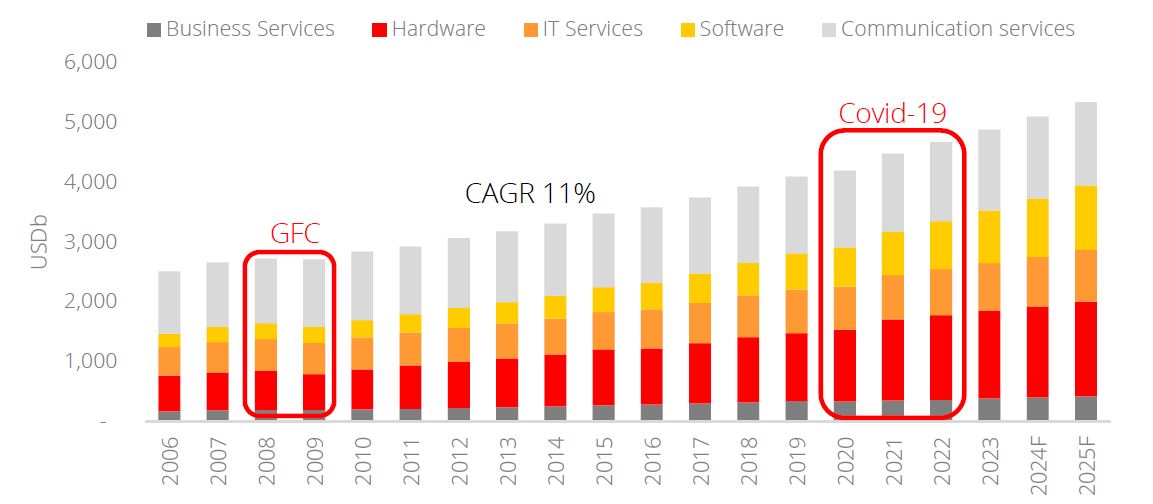

Catalyst 2: Resilient global IT spending uptrend. Global IT expenditure is expected to remain robust and broad-based, spanning across services, hardware, software, and communications, and reaching a total addressable market size of USD5.3t by 2025. This uptrend has remained intact over the past two decades, persisting even during the peak of Covid-19 lockdowns. The only exception was a minor blip during the GFC in 2009. As the adoption of Cloud computing and AI-embedded applications continue to expand, we believe Big Tech companies and sector leaders are poised to secure a slice of this growing pie.

Figure 4: Global semiconductor sales rebounding

Source: Bloomberg, DBS

Catalyst 3: Strong revenue and earnings backdrop. The sector’s glittering performance was driven by its strong fundamentals with the prospects of constructive earnings growth that outstrips the broader market. The enduring end demand, admirable pricing power, balance sheet strength, and the ability to generate robust cashflows all enhance the sector’s pole position in attracting investment fund inflows.

Figure 5: Big Tech’s outperformance is rooted in superior revenue and earnings growth

Source: Bloomberg, DBS

Catalyst 4: Solid balance sheet and shareholder returns. As mentioned, majority of Big Tech companies have negative net debt and have a higher degree of liquidity and financial stability compared to companies that are more highly levered. Additionally, having a large cash pile gives them the financial muscle to make opportunistic acquisitions and grow inorganically. This low dependence on leverage, coupled with strong earnings growth, has seen Big Tech consistently deliver impressive shareholder returns above that of global equities.

Figure 6: Low dependence on leverage and outstanding shareholder returns

Source: Bloomberg, DBS

Catalyst 5: Growth-adjusted valuation has room for expansion. While naysayers may argue that Big Tech trades at a huge premium (c.30x and c.26x 2024/25 earnings respectively), we believe the premium is justified given the quality of companies in question. Furthermore, on a growth-adjusted basis, the average 2024/25 PE-to-growth is not at all demanding. Big Tech’s 2-year average PE/G of 1.3x is at a stark discount compared to 1.8x of global equities. This fits well into our investment angle of Quality Growth-at-Reasonable-Price (Q-GARP): resilient growth that is not excessively priced.

Figure 7: Big Tech forward PE/G is at a discount to global equities

Source: Bloomberg, DBS

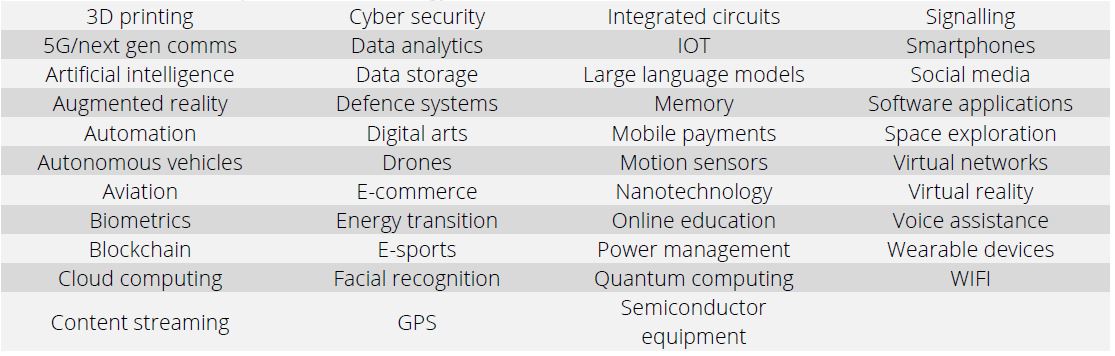

Catalyst 6: Growing opportunities across a myriad of verticals. Technology is more than just a buzzword in the investing community, it signifies a myriad of intertwined verticals that form the bedrock of the digital world we live in. Some prominent examples include AI, cloud computing, cyber security, e-sports, integrated circuits, power management, smart devices, software, and wearable devices. By investing in technology trend setters, investors are essentially participating in the creation of future.

Table 1: Select examples of technology verticals

Source: Bloomberg, DBS

Capture the value of Big Tech with the DBS CIO I.D.E.A framework. The pipeline of innovation and new technologies that is constantly and continuously reshaping our world is simultaneously bolstering the attractiveness of tech-investing. Big Tech and surrounding ecosystem plays fit the characteristics of Q-GARP. On the growth side of CIO Barbell strategy, we advocate for investors to employ the Q-GARP philosophy to capture long-term secular growth themes through the DBS CIO I.D.E.A. (Innovators, Disruptors, Enablers, and Adapters) framework in the following verticals: cloud computing, semiconductor, energy transition, AI, data analytics, software applications, and cyber security.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Digital Assets Update 2Q24: Base broadening14 May 2024

- BNP Paribas SA14 May 2024

- India rates: Macro sweet spot backs RBI’s comfortable hold 14 May 2024

Related Insights

- Digital Assets Update 2Q24: Base broadening14 May 2024

- BNP Paribas SA14 May 2024

- India rates: Macro sweet spot backs RBI’s comfortable hold 14 May 2024