Related insights

We expect the final quarter of the year to be volatile from economic, financial, political geopolitical events.

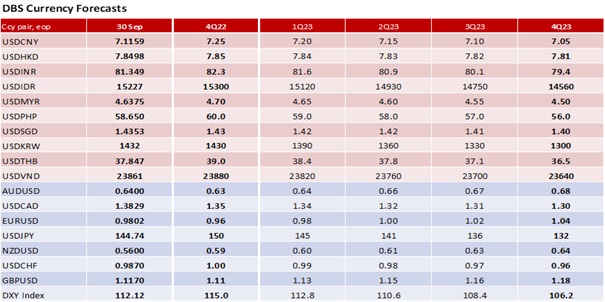

Look for the USD to extend its rise into 4Q22. The US economy is exiting its technical recession in 3Q22 (US GDP data on 27 October). We see the Fed delivering a fourth 75 bps hike to 4% at the FOMC meeting on 3 November. On 7 October, Bloomberg consensus expects US nonfarm payrolls to slow to 250k in September from 315k in August, with the unemployment rate unchanged at 3.7%. A week later, on 13 September, consensus sees US CPI core inflation firm at 0.4% MoM from 0.6%.

Conversely, the Bank of England believed the UK economy might have entered a mild technical recession with a contraction of 0.1% QoQ sa in 3Q22 (UK GDP data on 11 November). However, the BOE is in crisis mode after the Truss government delivered a mini-budget on 23 September that pounded GBP to a new lifetime low (1.0350 on 26 September) and boosted the 10Y Gilt yield to its highest level (4.59% on 28 September) since 2008. The markets considered the tax cut plans well-intentioned but poorly designed, i.e., exacerbating inflation and threatening fiscal sustainability.

On 29 September, the BOE intervened to cushion the pension industry with a pledge to buy up to GBP5bn of long-dated bonds a day until 14 October. The market expects a 100 bps hike to 3.25% at the MPC meeting on 3 November in response to the meltdown in the GBP and spike in Gilt yields. Although GBP recovered to the levels it fell from at the budget's announcement, investors were unwilling to accept a 10Y Gilt yield below 4% until they knew how the government intends to fund the largest tax cuts in five decades.

On 23 November, Chancellor Kwasi Kwarteng will announce a “Medium-Term Fiscal Plan” which will be accompanied by growth and borrowing forecasts from the Office for Budget Responsibility. However, the announcement is too far away for a market nervous over a government that is unwilling to make a policy U-turn or able to push forward. The Conservative Party annual conference in Birmingham this week (till 5 October) will gauge the discontent within the Tory MPs for the prime minister and her government. Many fear a new era of fiscal austerity to fund the mini-budget.

Over the weekend, attention has turned to Credit Suisse after its credit spreads widened to 2009 levels and its share price tumbled to a new record low. According to the Telegraph, the BOE’s Prudential Regulation Authority, which is monitoring the situation with Finma, believes that the stress did not result from major recent developments but from speculation triggered by its Chief Executive’s internal email seeking to reassure staff of the bank’s strong capital base and liquidity position. Credit Suisse will announce a new strategic plan on 27 October.

Europe is bracing for a harsh winter from a full-blown energy crisis. Bloomberg consensus has forecast the Eurozone economy entering a technical recession in 4Q22-1Q23. However, the European Central Bank has pledged to keep hiking rates in the next several meetings to control CPI inflation which spiked to 10% YoY in September. Even so, the ECB is unlikely to match the 100 bps expected for the BOE at its meeting on 27 October. After its spike above 0.92 on the mini-budget on 26 September, EUR/GBP fell back to its support around 0.8750 last Friday. The cross rate may rise again if the EUR and GBP resume their declines after last week’s relief rally.

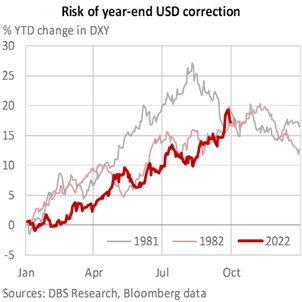

However, the USD may also peak in 4Q22. The Fed may slow the pace of hikes to 50 bps in December. Recent events in Europe have rendered the Fed more alert to the possible negative economic and financial spillovers from external forces. The last time the USD appreciated this much in a year was 1981 and 1982. It consolidated in 4Q81 and fell in November-December 1982.

Last week, Atlanta Fed President Raphael Bostic warned that UK’s mini-budget crisis could add to more uncertainties for consumers and businesses and lead to a global recession. Fed Vice Governor Lael Brainard fears that global monetary policy tightening could trigger deleveraging dynamics in emerging markets with high sovereign and corporate debt levels. The IMF World Economic Report on 5 October should provide more insight on these issues.

Asia is unhappy with the USD’s strength.

On 22 September, Japan intervened after USD/JPY pushed above 145 after the Bank of Japan’s decision to maintain its ultra-accommodative monetary policy, one day after the Fed lifted its projection for interest rates. Although USD/JPY has recovered from 140, it consolidated in a tight 144-145 range last week, caught between monetary policy divergences and fears of more intervention.

China pushed back against speculative one-sided currency bets that drove USD/CNY to the upper limit of its official trading band. The People’s Bank of China told banks to reinstate the counter-cyclical factor in their daily fixings last Wednesday. The Wall Street Journal reported the China Securities Regulatory Commission sending an advisory to international and domestic banks to refrain from publishing politically sensitive research ahead of the Communist Party meeting in mid-October. USD/CNY ended September at 7.1159, near its fixing at 7.0998, before China went away for the Golden Week holiday this week.

US President Joe Biden and President Xi Jinping will meet face-to-face at the G20 Summit in Bali, Indonesia, on 15-16 November. Before that, the stage is set for Chinese President Xi Jinping to secure a third term at the 20th Party Congress on 16 October. On 8 November, polls expect the Democrats to lose one or two houses of Congress at the US mid-term election. A poor outcome may lead President Biden to consider personnel changes, including the Treasury Secretary’s position. President Xi and US Vice President Kamala Harris will attend the APEC Summit in Bangkok, Thailand, on 18-19 November. The ASEAN Summit in Phnom Penh, Vietnam, on 11-12 November, will focus on the Russia-Ukraine war, energy prices, and food security.

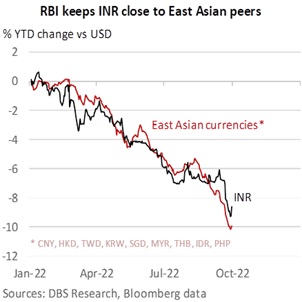

INR hit a record low of 82 per USD on 28 September. The Reserve Bank of India delivered a second 50 bps hike to 5.90% on 30 September. More importantly, RBI Governor Shaktikanta Das explained that the 15.2% drop in foreign reserves from USD634bn in December to USD538bn in September was not due to capital outflows. About two-thirds were attributed to valuation impact from the sell-off in the other reserve currencies such as EUR, GBP, CHF, and higher US bond yields. RBI will not hesitate to intervene to smooth exchange rate volatility. Indeed, this has kept the INR fairly aligned with the average depreciation in East Asian currencies this year.

Quote of the day

“One of the test of leadership is the ability to recognize a problem before it becomes an emergency.”

Arnold H. Glasgow

3 October in history

In 1863, US President Abraham Lincoln designated the last Thursday of November as Thanksgiving Day.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.