Related insights

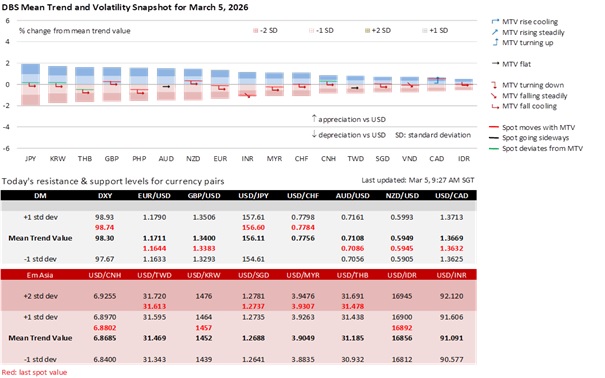

The DXY has retraced lower to below 99, amid hopes of a resolution to the current war between US and Iran. Iranian missile launch intensity has fallen sharply due to degradation from strikes, and media reports indicate that Iranian intelligence has signalled openness to talks to end the war. Iran has officially denied this, and a consequential decision could have to await the election of a Supreme Leader to replace Khamenei. Meanwhile, US and Israeli air superiority should lower, but not eliminate, risks of disruptions to energy production. Brent prices have stabilized at around USD82 after initially testing as high as USD85, while US equities have also recovered some of its Tuesday losses. US payrolls tomorrow may play second fiddle to geopolitical developments for the USD now.

USD/KRW has completely a full retracement back to 1460 levels, after an initial surge to 1500 on Tuesday. Sentiment has turned sharply as Korean equities surged by 11% at today’s open, recovering strongly from its worst two-day loss (-18%) since the 2008 Global Financial Crisis. Such meme-stock level of volatility is unusual, and FSC Chair Lee said yesterday that Korea is prepared to use its KRW100trn market stabilization program in case of excessive volatility. Economically speaking, only around 7% of Korean power generators’ feedstock is subject to disruption risk at the Straits of Hormuz, which is a tolerable risk. Electricity tariffs are also subject to regulation in Korea, so energy cost pass through to companies and households may also be limited. We see the sell-off in Korean in equities as being more driven by speculative squaring than economics, with market valuations having surged to record highs this year.

China’s NPC has announced its 2026 growth target as 4.5% to 5%, lowering it from the 5% target for 2025. China’s budget deficit will be kept unchanged at around 4% of GDP for 2026, with issuance of ultra-long special sovereign bonds and local government special bonds kept unchanged at CNY1.3trn and CNY4.4trn respectively. Without new fiscal impulse, the pace of RMB gains will likely be kept gradual to support growth, while RRR and rate cuts have also been flagged as possible tools to support the economy. Meanwhile, USD/CNH has stabilized at around 6.90, after having tested 6.94 amid USD strength. The scrapping of the 20% reserve requirement on FX forwards is a reversion to normal after RMB depreciation pressures fade, and is in line with a historical practice to lower the ratio back to zero when RMB strengthens, such as in Sep 2017 and Oct 2020.

Quote of the Day

"Never allow a person to tell you no, who doesn't have the power to say yes.”

Eleanor Roosevelt

March 5 in history

Venezuelan Vice-President Nicolás Maduro assumes the presidency after the death of Hugo Chávez in 2013.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.