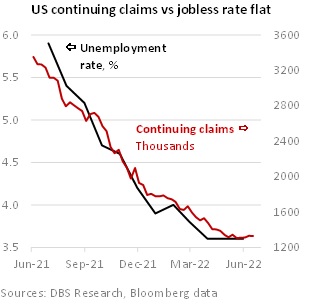

- US unemployment rate to stay low at 3.6% for the fourth month in June

- US nonfarm payrolls may drop below 300k for the first time since April 2021

- US tech companies have started layoffs and rescinding previous job offers

- The cooling US housing market will trigger more layoffs too

- The US midterm elections in November might matter to markets

Related insights

Commentary: The tight US labor market is becoming less robust

Friday’s US unemployment rate can stay at 3.6% for the fourth month in June as per continuing caims. The Fed’s latest forecast for the jobless rate to rise to 3.7% in 4Q22 appears optimistic. Initial jobless claims have been rising steadily with every Fed hike.

US nonfarm payrolls may decline below 300k in June for the first time since April 2021. The odds will increase if Thursday’s ISM Services employment slips below 50 again in June. On a 4-week moving average basis, initial jobless claims have risen with each Fed hike to its highest level this year.

Manufacturing payrolls could also turn negative after ISM manufacturing employment extended its decline below 50 to 47.3 in June, its worst reading since October. US tech companies have started announcing layoffs and rescinding previous job offers. Some of the reasons cited are high inflation and, notably, heightened recession risks amidst the worst 1H stock market sell-off since 1970.

Reuters reported that mortgage lenders, refinancing companies and real estate brokers plan to lay off thousands of workers in the coming months. The US housing market is cooling despite higher home prices. Existing, pending and new home sales have slowed this year. Rising home prices, higher mortgage rates and deeper negative wage growth have rendered home ownership less affordable. Home buyers also turned cautious on heightened US recession risks amidst uncertainties over the Russia-Ukraine war.

Consensus expects June’s average hourly earnings growth to slow a third month to 5% YoY in June. Earnings peaked at 5.6% YoY in March at the first Fed hike. In month-on-month terms, earnings were unchanged at 0.3% for three months. Slower wage growth should help ease the Fed’s worries about a wage-price spiral. As inflation and cost of living become voters’ top issues, the US midterm elections in November might matter to markets. As witnessed during Fed Chair Jerome Powell’s semi-annual congressional testimonies last month, Republicans blamed the Biden administration for stoking inflation with massive stimulus spending. Unlike the Covid recession, monetary and fiscal stimulus will be less forthcoming if a recession turns up.

Philip Wee

To read the full report, click here to Download the PDF.

Nathan Chow 周洪禮

Senior Economist and Strategist - China & Hong Kong 高級經濟學家及策略師 - 中國及香港

[email protected]

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.