- US: Trump’s election as the US President and the Senate shifting to a Republican majority signal intensifying trade war and deficit spending ahead

- Hong Kong: Growth slowed from 3.2% y/y to 1.8% y/y in 3Q; consumption remains subdued due to strong outbound travel, weak tourist spending

- Indonesia: High frequency prints point to a softer 4Q; we maintain our 5% forecast for 2024 and factor in a small improvement next year

- India: Soft incoming data prompt a trimming in growth forecast; elections, construction slowdown, and poor weather dent output

Related insights

- Digital Realty Trust Inc06 Mar 2026

- FX Tactical Ideas: Geopolitics Takes Over06 Mar 2026

- Johnson & Johnson06 Mar 2026

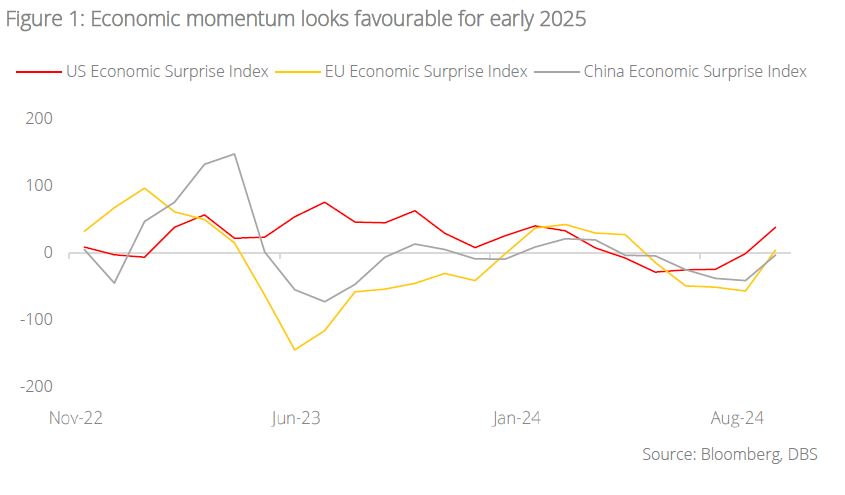

US: Trump win and the global macro narrative. The market narrative has been one of softening growth, inflation, and interest rates ahead—the Federal Reserve lowered the Federal Funds rate by 25 bps to a range of 4.5% to 4.75% this week, following the 50 bps reduction in September. However, the election of Donald Trump as the 47th president of the US poses considerable challenges to this narrative. Now, it looks as though inflation and rates may not come down as much as market pricing suggests, and there is some risk of financial instability. This would be particularly on the cards if growth and inflation prove to be higher than forecasted by Fed officials in recent months and the central bank begins to walk back its guidance for many rate cuts next year.

What Trump 2.0 means for the US is relatively clear. His stance on taxes, immigration, public spending, cryptos, and federal bureaucracy are well known. Given his executive power and an enabling Senate, he would be able to enact lasting changes in all these areas. Expect more tax cuts, headline grabbing measures to deal with undocumented migrants, a wide berth for cryptos, and sweeping changes in the top layers of US bureaucracy.

Trump would want an economy supported by low interest rates, but his fiscal policy ideas would get in the way of the Fed’s intentions to cut rates by a lot, in our view. The Fed may cut a few times in 2025, but the policy easing picture could get considerably muddy if growth remains strong and inflation begins to rebound. A clash between the Fed and Trump may then ensue, causing consternation among investors. We are quite concerned about this scenario.

Tariffs are an unambiguous negative for Asia, but the region’s strong ties with the US and China would survive Trump. The region’s openness to trade and commerce makes it more attractive to investors, especially as the contrast with an inward-looking West becomes stark. Exports will face more scrutiny and there will more regulatory headaches, but the region’s scale, excellence in manufacturing and logistics, strong corporate and public sector balance sheets will hold them in good stead through Trump 2.0. China would likely push for more stimulus to boost domestic demand. This election marks a firm rightward shift of the US and Asia has to learn to live with it.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Digital Realty Trust Inc06 Mar 2026

- FX Tactical Ideas: Geopolitics Takes Over06 Mar 2026

- Johnson & Johnson06 Mar 2026

Related insights

- Digital Realty Trust Inc06 Mar 2026

- FX Tactical Ideas: Geopolitics Takes Over06 Mar 2026

- Johnson & Johnson06 Mar 2026