- The S&P 500 sell-down last week came on the back of portfolio rotation out of AI names as capex and concentration risks intensify; this shift was amplified by speculative retail positioning in leveraged products

- Rotations into healthcare, real estate, and consumer staples reflects a broadening of the AI themes

- US earnings momentum remains supportive, with forecasted earnings outpacing price gains amid strong capex trends

- Complement tech exposure with AI adapters in traditional sectors, companies that leverage on AI to improve efficiency and drive profitability growth

US sectoral rotational shifts in motion. The sell-down on S&P 500 last week probably came as a surprise given the downshift in energy prices and government bond yields which traditionally buoy risk assets. A dissection of the market performance suggests that major sectoral shifts are underway. At the index level, the US equities sell-down was driven predominantly by the rout in AI-related plays. Elevated retail participation in speculative instruments (such as leveraged ETFs) accentuated the magnitude of this.

However, the weakness was far from broad-based. Beyond technology, several traditional US industries actually ended the week higher. Gainers include healthcare (+7.9%), real estate (+4.0%), and utilities (+4.0%), which stood in stark contrast to communication services (-6.2%) and technology (-5.4%). This rotational shift reflects two key concerns:

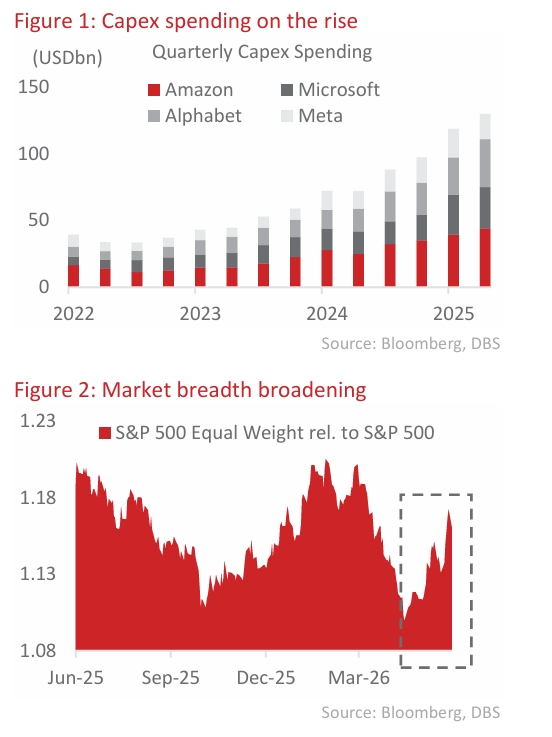

- Rising capex: Market’s scrutiny over hyperscalers’ aggressive spending plans is increasing, with the four largest hyperscalers (Amazon, Microsoft, Alphabet, and Meta) guiding to c.USD725bn combined capex for 2026, nearly doubling 2025 levels. Furthermore, these tech companies are increasingly tapping on the debt market to fund massive capital commitments. For example, Meta recently issued USD25bn of bonds in May, marking its second jumbo debt issuance in just six months.

- Concentration risk: Currently, technology companies account for nine of the top 10 constituents, representing c.38% of the S&P 500. This concentration has materially diminished the diversification benefits of US equities, leaving investors with greater exposure to a single sector and less protection against technology-specific risks.

Such concerns are also evident in fund flow data. For the week ended 24 June, technology and communication services recorded net outflows of USD12bn and USD0.5bn, respectively, while healthcare and utilities attracted inflows of USD1bn and USD0.4bn. This suggests a portfolio rotation towards less crowded segments of the market.

Complement technology exposure with AI adapters. Forecasted earnings have been increasing at a faster pace than equity prices this year underpinning the resilience of US equities. Given the strong capex momentum in place, it is reasonable to assume that the robust earnings momentum will stay intact. However, the AI investment cycle is entering a more mature phase. Given current valuation and concentration levels, we recommend that investors ride the AI wave with AI “adapters” – traditional industries that embrace AI to improve efficiency and increase profitability. This provides a better risk-adjusted way to participate in the AI theme while reducing overall portfolio concentration risk.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.