- US/Japan: We view core inflation and real wage growth as critical policy considerations for a Warsh-led FOMC, amid his reluctance to provide a dot plot; political pressures on the Fed to cut rates appear to be moderating

- Thailand: BOT is likely to stay on hold, supporting growth amid transitory inflation; the 2026 GDP growth forecast was upgraded to 2.3% from 1.5%, reflecting resilient exports and private investment tied to the AI tech cycle and government measures

- Taiwan: Taiwan's central bank kept its policy rate unchanged at 2.00% at its June meeting, while maintaining a slightly hawkish bias; we continue to forecast a 12.5 bps rate hike in 2H26, but shift the expected timing to 4Q26 from 3Q26

- India: The India–US trade framework, initially agreed upon in February, is now in the final stages of being formalised through an interim trade agreement

Related insights

- Research Library08 Jul 2026

- Macro Insights Livestream, July 2026: Wednesday, July 15th, 4pm SGT08 Jul 2026

- USD Rates: Yields reclaim key levels as USTs sold off 08 Jul 2026

US/Japan: Warsh’s dilemma. US Fed’s new FOMC Chair, Kevin Warsh, surprised markets with a hawkish tone last week but did not assign his own forecast to the dot-plots. We think two metrics will be critical for policy consideration. First, core inflation – if it heads past 3.5% in May-Jun even as energy prices correct. Second, real wage growth, which has turned negative due to rising inflation. If that begins to rebound and moves into positive real growth territory, the Fed will be out of excuses to maintain a policy pause.

Political pressures on the Fed to cut rates appear to be moderating. Addressing questions on whether Fed Chair Warsh could face pressure from Trump, Treasury Secretary Bessent noted that Trump has said Warsh will be independent. Warsh may face less pressure than his predecessor on rate decisions, given Trump’s awareness of the negative impact on bond markets from such actions.

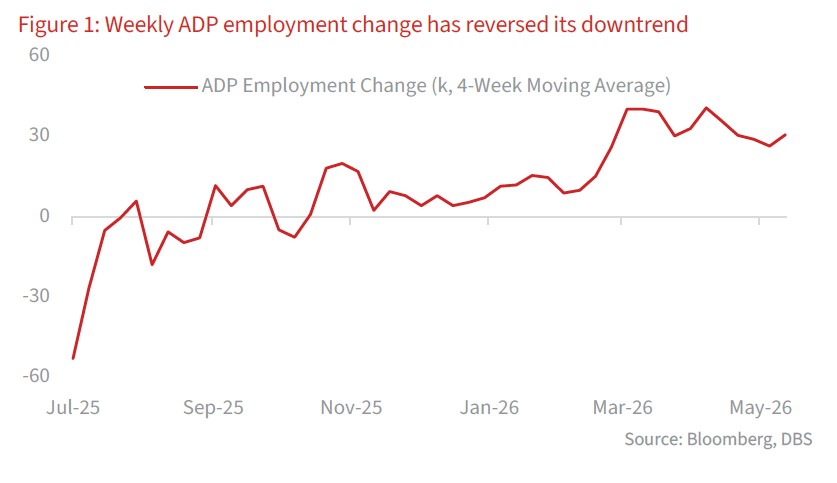

That said, the US economy continues to display resilience. The weekly ADP employment change (on a four-week moving average basis), released on 23 Jun at 30.75k, has reversed its downtrend. This indicates that private sector hiring remains sturdy. Initial jobless claims are on the rise, albeit remaining relatively low (consensus at 225k). The labour market demand-supply balance is largely steady. Thus far, both the labour force and total job opportunities (employment + job openings) stand at approximately 170mn. Beyond the labour market, both the S&P Manufacturing and Services PMIs continue their upward march and have beaten market expectations. Separately, market consensus project next week’s nonfarm payrolls release to show a 130k gain in June, with the unemployment rate remaining unchanged at 4.3%. The Conference Board Consumer Confidence Index is also projected to improve to 94.2 in June from 93.1 in May.

Market sentiments are improving on news that Middle East talks are slated to continue next week, according to a Pakistani official. Brent prices have slipped below USD70/bbl, returning to pre-conflict levels and signalling a normalisation in supply conditions.

Separately, Japan PM Takaichi has unveiled a JPY370tn (USD2.3tn) investment plan to be financed through public-private partnerships by fiscal 2040, aimed at strengthening economic security and supporting long-term growth. The plan spans 17 strategic sectors and 62 designated products and technologies, including semiconductors, AI, quantum technology, and energy. Semiconductors will receive a large allocation of JPY68tn, with further details to be finalised soon. While increased investment is necessary to support Japan’s growth outlook—and the country has historically executed effective industrial policy—its elevated public debt burden could be a constraint for ambitious initiatives.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Research Library08 Jul 2026

- Macro Insights Livestream, July 2026: Wednesday, July 15th, 4pm SGT08 Jul 2026

- USD Rates: Yields reclaim key levels as USTs sold off 08 Jul 2026

Related insights

- Research Library08 Jul 2026

- Macro Insights Livestream, July 2026: Wednesday, July 15th, 4pm SGT08 Jul 2026

- USD Rates: Yields reclaim key levels as USTs sold off 08 Jul 2026