- Early volume trend in 1Q26 is encouraging, but may not be indicative of full-year performance

- Consumers likely to increasingly prioritise value with intensifying cost of living pressure

- National brands to face pressure to narrow value gap relative to private labels

- Favour pure play beverage players with limited private label competition

Related insights

- Singapore Equity Picks12 Jun 2026

- CIO Insights 3Q26: Power Play12 Jun 2026

- FX Tactical Ideas: Staying Positive on the USD12 Jun 2026

Positive early volume recovery in 1Q26 may not necessarily be indicative of full‑year performance. While pricing remains the primary top‑line driver for most listed PFNAB companies, an improving q/q volume trend is beginning to emerge. Notably, Coca‑Cola recorded solid 3% y/y unit case volume growth in 1Q26, led by China, US, and India, improving from 1% in 4Q25. We also saw a meaningful improvement in volume trends at Kraft Heinz and Mondelez, with volume/mix declines narrowing to ‑1.2% and ‑0.5% respectively in 1Q26, compared with ‑4.7% and ‑4.8% in 4Q25. For Kraft Heinz, the improvement appears to reflect earlier brand and marketing investments gaining traction. In contrast, Mondelez’s volume stabilisation was driven by distribution expansion and its ability to respond more swiftly to evolving consumer preferences.

Value proposition remains critical in stemming volume declines. Both PepsiCo and Kraft Heinz have announced major initiatives to address ongoing volume weakness. PepsiCo introduced price cuts of up to 15% on selected brands while maintaining pack sizes. This strategy has shown early green shoots, with its North America Foods business returning to 2% volume growth in 1Q26 after several quarters of decline. Under its new CEO, Kraft Heinz has paused plans to split into two separate companies and instead announced a USD600mn investment to revitalise its brands, prioritising long-term recovery over near-term earnings. As a result, FY26 earnings are projected to decline by c.22%. Approximately half of this investment will be directed towards pricing, product quality, and packaging, with the remainder allocated to R&D, as well as incremental sales and marketing headcount and related investments.

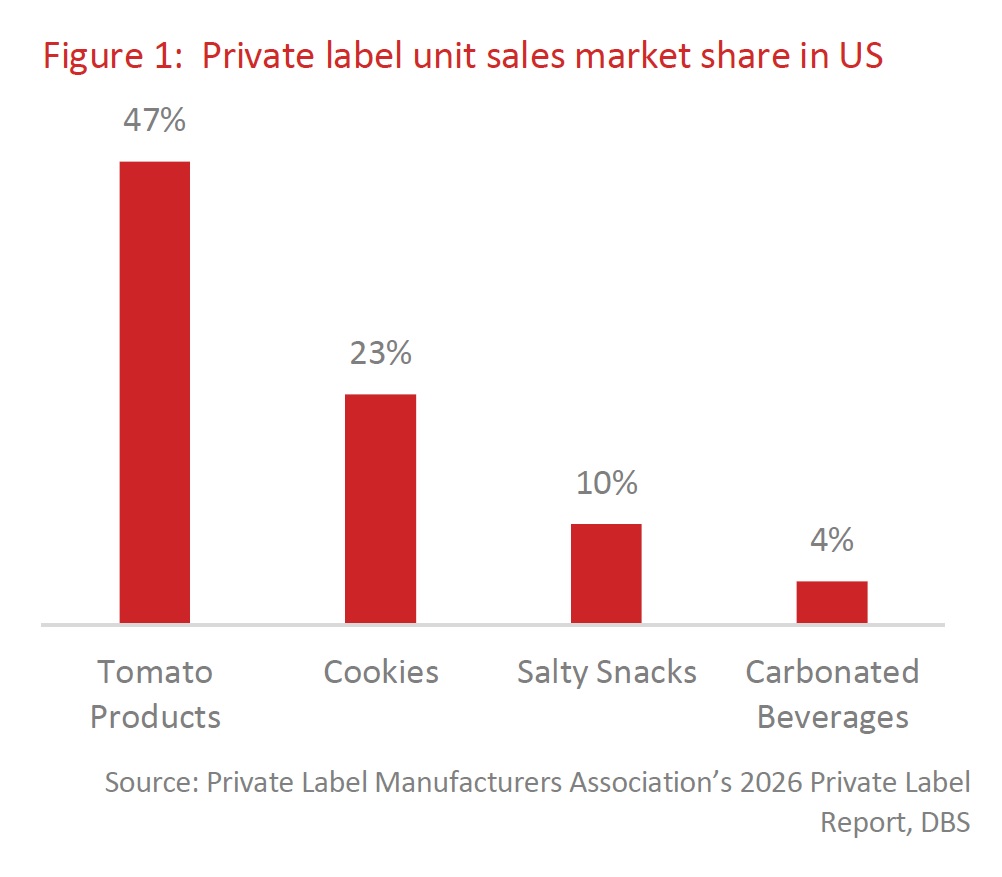

Beverage category remains the safer play with limited private label headwind. With fuel prices surging and likely to remain elevated for a prolonged period due to the ongoing conflict in Iran, expect renewed cost-of-living pressures on US consumers. As such, the strategic shifts undertaken by PepsiCo and Kraft Heinz may translate into only limited volume uplift, particularly given significant private-label penetration of 10% in salty snacks and 47% in tomato products. By comparison, branded beverage players such as Coca‑Cola are likely to face lower private-label competition, supported by relatively low private-label penetration in beverages, especially in carbonated drinks, where penetration stands at just 4%.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Singapore Equity Picks12 Jun 2026

- CIO Insights 3Q26: Power Play12 Jun 2026

- FX Tactical Ideas: Staying Positive on the USD12 Jun 2026

Related insights

- Singapore Equity Picks12 Jun 2026

- CIO Insights 3Q26: Power Play12 Jun 2026

- FX Tactical Ideas: Staying Positive on the USD12 Jun 2026