- Surgical robot industry monopoly ended in 2020 following the expiry of key patents

- Multiple surgical robot companies have emerged to tap into the highly unsaturated market

- Europe has the highest growth potential with large population and low surgical robot penetration rate of 6%

- MNCs have not seen meaningful traction as their designs differ too greatly from market leaders

- Chinese players expected to gain significant market share

Related insights

- Singapore Equity Picks15 May 2026

- Costco Wholesale15 May 2026

- Research Library15 May 2026

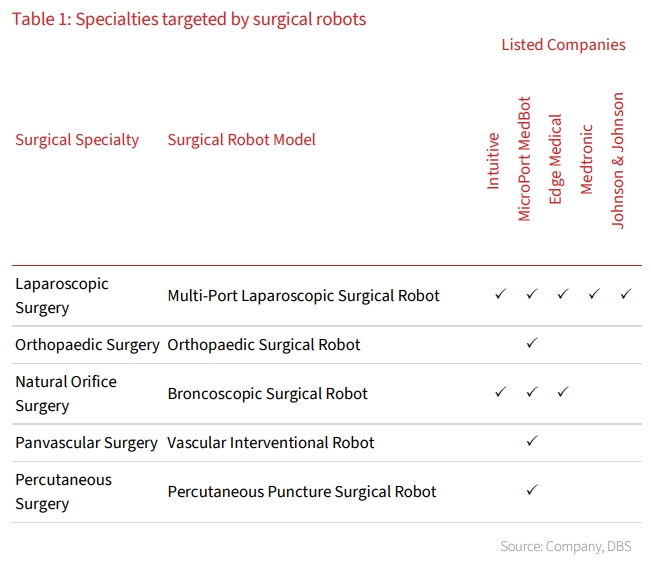

End of a monopoly. The surgical robot market was effectively monopolised by Intuitive Surgical for the past two decades. However, market dynamics have shifted since its core patents started expiring between 2016 to 2020. Since then, several surgical robot companies have emerged to tap into the highly unsaturated market, which was estimated to be worth USD11.2bn in 2025. Surgical robots are typically used in minimally invasive procedures spanning multiple specialties including urology, gynaecology, general surgery, thoracic, orthopaedic, bronchoscopic, vascular, and percutaneous surgery.

Europe set for a significant boom in surgical robots. The US is Intuitive’s main revenue driver, with >6,000 installed units and a penetration rate of 22% among minimally invasive surgeries. Europe, however, offers the highest growth potential, supported by a larger population than the US and a lower penetration rate of just 6%. Two Chinese players – MicroPort MedBot and Edge Medical – have emerged and are rapidly gaining market share in Europe, with each having sold c.100 units in Europe since gaining CE approval in May 2024 and Mar 2025 respectively. In contrast, growth is expected to be rather muted in China as the government limits the number of surgical robots sold to the market through deployment permits, only allowing 559 new surgical robots to be sold between 2021 to 2025.

MNCs are innovating but not seeing good traction. Multinational corporations such as Medtronic and Johnson & Johnson have developed their own surgical robots but have not seen meaningful traction. This is largely due to design differences that diverge significantly from Intuitives’, which surgeons have grown accustomed to. Chinese players MicroPort MedBot and Edge Medical are well positioned to gain significant market share as their designs closely resemble Intuitive’s while offering system and consumable costs that are 25% cheaper.

Overall, the global surgical robot sector remains a key space to watch within the wider healthcare space, given the significant growth prospects for Chinese companies, the vast untapped opportunities in Europe, and the ongoing impact of Intuitive Surgical's patent expiries.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Singapore Equity Picks15 May 2026

- Costco Wholesale15 May 2026

- Research Library15 May 2026

Related insights

- Singapore Equity Picks15 May 2026

- Costco Wholesale15 May 2026

- Research Library15 May 2026