Related insights

- FX Tactical Ideas: USD Gains Have Been Limited27 Mar 2026

- Research Library27 Mar 2026

- FX Quarterly 1Q 26: The USD’s war-driven haven trap27 Mar 2026

Transitioning to “Takaichi-nomics”

We see constructive implications for Japanese equities as a more assertive and coordinated economic agenda is expected under the Takaichi administration. With a strong legislative mandate, government ministries now possess the political capital to execute reform with greater speed and cohesion, anchored on a “responsible and proactive” fiscal stance.

Targeted fiscal deployment into strategic sectors should reinforce business confidence, catalyse private capex, and strengthen the investment climate. In this context, the transition from “Abenomics” and “Kishida-nomics” toward “Takaichi-nomics” could consolidate the narrative of a structurally transformed “New Japan” – characterised by sustainable growth, firmer nominal GDP momentum, and the eventual normalisation of the structurally undervalued yen.

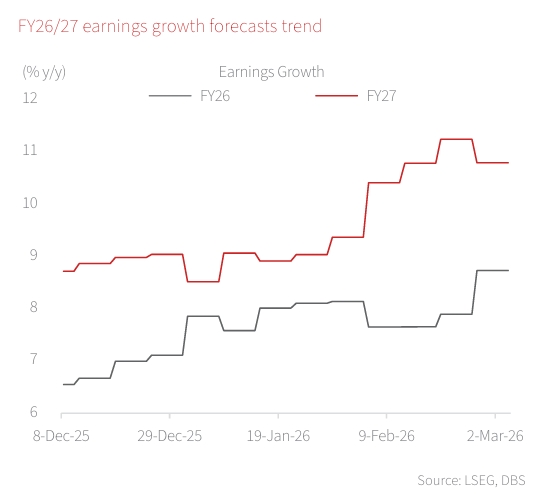

Consensus forecasts for both GDP and corporate earnings have been revised upward following the LDP’s landslide win. Foreign investors, net sellers in the prior few months, have returned meaningfully – a signal that policy clarity and growth visibility are improving sentiment.

Reform Momentum and Equity Supply Tightening

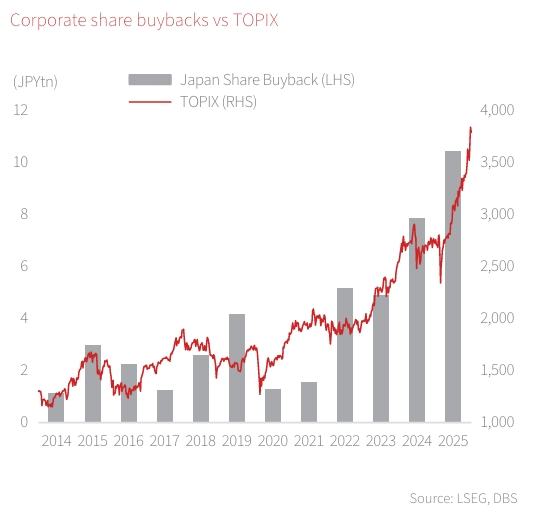

Structural reforms initiated in prior years are now manifesting in capital discipline and shareholder returns.

- Corporate share buybacks reached record highs in 2025.

- Divestments of non-core assets have accelerated.

- M&A and private equity deal volumes also hit cyclical highs.

- Companies are paying higher dividends.

This combination of improving shareholder value and governance reform has effectively tightened equity supply while improving return-on-equity metrics. More importantly, the resilience of corporate earnings and the attainment of record equity levels suggest that structural reforms implemented over the past two years are already translating into tangible corporate outcomes. We expect this momentum to persist into 2026, further underpinning market performance.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- FX Tactical Ideas: USD Gains Have Been Limited27 Mar 2026

- Research Library27 Mar 2026

- FX Quarterly 1Q 26: The USD’s war-driven haven trap27 Mar 2026

Related insights

- FX Tactical Ideas: USD Gains Have Been Limited27 Mar 2026

- Research Library27 Mar 2026

- FX Quarterly 1Q 26: The USD’s war-driven haven trap27 Mar 2026