Related insights

- Research Library13 Mar 2026

- FX Tactical Ideas: USD Supported on US-Iran Conflict13 Mar 2026

- The Cryptocurrency Handbook13 Mar 2026

US: Geopolitics and US data. Ongoing attacks on Iran by Israel and the US are at once expected and yet, still astonishing. The scale of the attack and retaliation, the damage already inflicted, the heightened uncertainty surrounding what comes next are extensive in scope. Fears of oil supply disruption—particularly the risk of an effective closure of the Strait of Hormuz which accounts for roughly 25-30% of global oil trade—have driven a sharp spike in oil prices.

In response, President Trump announced that the Development Finance Corp would provide insurance for ships transiting in the Strait of Hormuz with the US navy possibly providing escort if needed. Addressing this issue reduced the risk that oil supply in the region would be drastically reduced for an extended period due to maritime transport frictions. Media reports indicate that Iranian intelligence has signalled openness to talks to end the war. Iran has officially denied this, and a consequential decision would have to await the election of a Supreme Leader to replace Khamenei. Meanwhile, US and Israeli air superiority should lower, but not eliminate, risks of disruption to energy production.

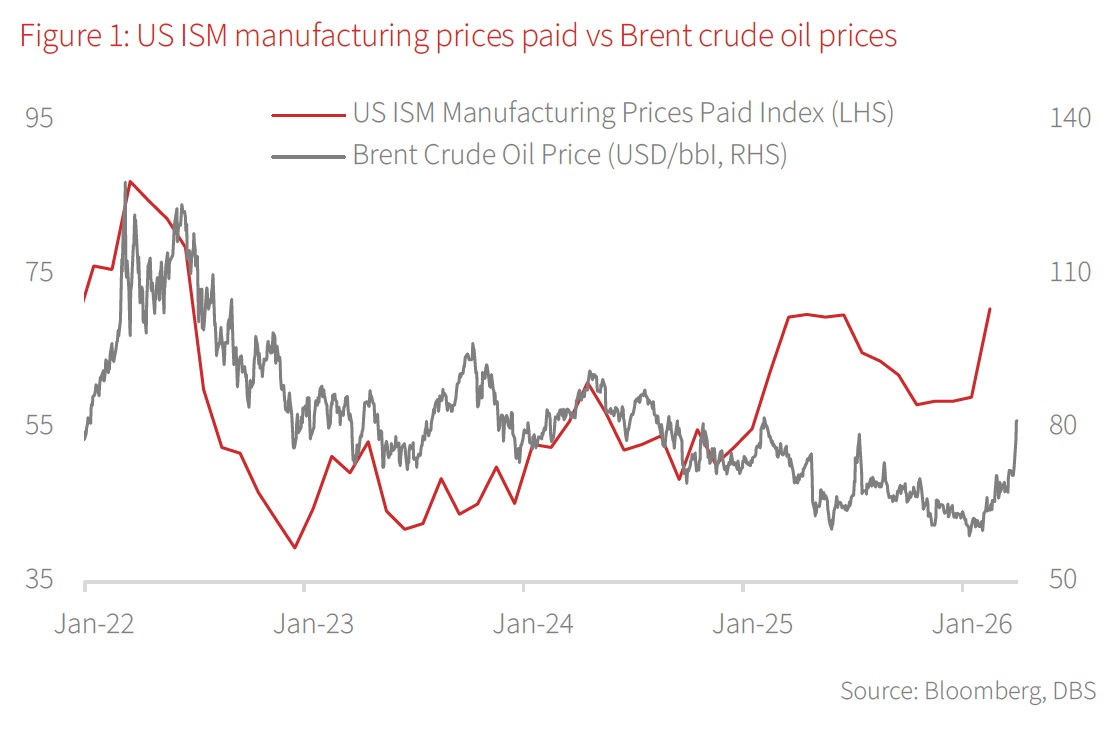

That said, investors are keeping an eye on US fundamentals as gyrations in the energy markets calm. The latest data already indicated that the US manufacturing sector may be in for a cyclical upturn with manufacturing PMI (51.6 against consensus of 51.4) and ISM manufacturing (52.4 against consensus of 51.5) figures climbing. The pop in ISM prices paid (70.5) is eye-catching and builds on the 0.5% m/m sa increase in PPI figures released last week. Moreover, the beat in ADP employment figures (63k against consensus of 50k) suggests that the labour market may have bottomed. Taken together, this mix points to underlying price pressures that came about before the recent pop in energy prices. Inflation worries are simmering. The bets on Fed rate cuts have been pared to just two this year, compared to 2.5 last Friday (27 Feb).

Labour market data (NFP due Friday, 6 Mar) will be critical. Consensus expects a moderation to 59k (130k previously). Given the volatility of this figure, it may be difficult to draw firm conclusions from a single print. Instead, a broader range of data (including jobless claims, ADP employment, and the unemployment rate) should also be assessed to provide a better gauge of the labour market. Suffice to say, the high frequency indicators, thus far, suggests that the soft patch in hiring may be behind us.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Research Library13 Mar 2026

- FX Tactical Ideas: USD Supported on US-Iran Conflict13 Mar 2026

- The Cryptocurrency Handbook13 Mar 2026

Related insights

- Research Library13 Mar 2026

- FX Tactical Ideas: USD Supported on US-Iran Conflict13 Mar 2026

- The Cryptocurrency Handbook13 Mar 2026