- US/Japan: Trump’s swift pivot to Section 122 indicated no liberation from his broad tariff policies, albeit with lower global effective tariff rates; however, with tax rates capped at 15% and requiring Congressional approval for extension, the shift lacks the fear factor needed to extract deep concessions.

- ASEAN-6 and India: Unilateral tariffs imposed by the US on the ASEAN-6 and India under IEEPA are likely to be ruled invalid; effective tariff rates should decline for India and most of the ASEAN-6, with Singapore retaining the lowest rate in the region

- Thailand: We expect a pause in policy rate cuts, with downside risks, following BOT’s surprise 25 bps cut at its first meeting of 2026

Related insights

- Digital Realty Trust Inc06 Mar 2026

- FX Tactical Ideas: Geopolitics Takes Over06 Mar 2026

- Johnson & Johnson06 Mar 2026

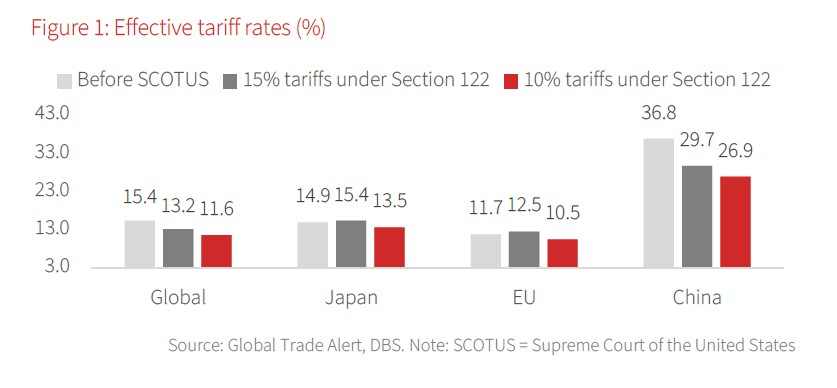

US/Japan: Tariff rebranded, power diluted. Following the US Supreme Court’s invalidation of Trump’s IEEPA tariffs, the administration moved quickly to invoke Section 122, imposing a 10% global tariff from 24 Feb, with the possibility of an increase to 15% and no clearly defined timeline. This swift pivot signalled no liberation from his broad tariff policies, albeit global tax-effective rates are estimated to be lowered by 3.8 %pts (2.1 %pts for potential 15% tariff), according to Global Trade Alert. However, capped at 15% and requiring Congressional approval for extension, the shift to Section 122 lacks the fear factor needed to extract deep concessions with major trading partners, who recognise that the administration faces a legislative dead-end on 24 Jul. The Supreme Court’s ruling also transforms prior IEEPA tariff collections into a sizable refund liability estimated at around USD175bn, potentially upending the administration’s core strategy of using tariff revenue to fund the “One Big Beautiful Bill”.

Meanwhile, the State of Union (SOTU) confirmed that the administration has entered a pre-election "campaign mode," prioritising domestic economic stability over geopolitical brinkmanship. By favouring diplomacy over military action in Iran, the President signalled a preference to prevent a spike in oil prices that would fuel cost-of-living concerns. This pivot away from escalation would also clear the way for Trump to pressure his Fed Chair nominee, Kevin Warsh, to implement aggressive rate cuts.

The US Conference Board's Feb 2026 report showed consumer confidence rising to 91.2, up from an upwardly revised 89.0 in January. The increase was driven by a rise in short-term expectations for income, business, and labour conditions to 72 from 67.2. Despite the improvement, the Expectations Index remained below the 80 threshold that has historically signalled a recession ahead. The present Situation Index decreased by 1.8 pts to 120, reflecting a more pessimistic assessment of current business and employment conditions compared to Jan 2026. Consumers remained concerned about prices, inflation, and the cost of goods. Mentions of trade and politics also increased in February.

Turning to Japan, Takaichi’s cabinet nominated two members to the Bank of Japan’s policy board on 25 Feb: Toichiro Asada and Ayano Sato. Both are viewed as supportive of reflation and looser monetary settings. Markets interpreted the appointments as a shift towards a more dovish BOJ stance, implying slower interest rate hikes. We view the market reaction as a normal adjustment to previously overpriced expectations of an April rate hike. The outgoing members, Asahi Noguchi and Junko Nakagawa – whose terms expire in March and June, respectively – were considered dovish and neutral. Their replacement is unlikely to significantly alter the BOJ’s nine-member policy board. We maintain our expectation that the BOJ will continue a data-dependent approach to monetary policy, likely delivering the next rate hike in June or July, after assessing this year’s Shunto wage negotiations, confirming wage-inflation dynamics, and evaluating the impact of China’s expanding export controls on Japan’s growth outlook.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Digital Realty Trust Inc06 Mar 2026

- FX Tactical Ideas: Geopolitics Takes Over06 Mar 2026

- Johnson & Johnson06 Mar 2026

Related insights

- Digital Realty Trust Inc06 Mar 2026

- FX Tactical Ideas: Geopolitics Takes Over06 Mar 2026

- Johnson & Johnson06 Mar 2026