Related insights

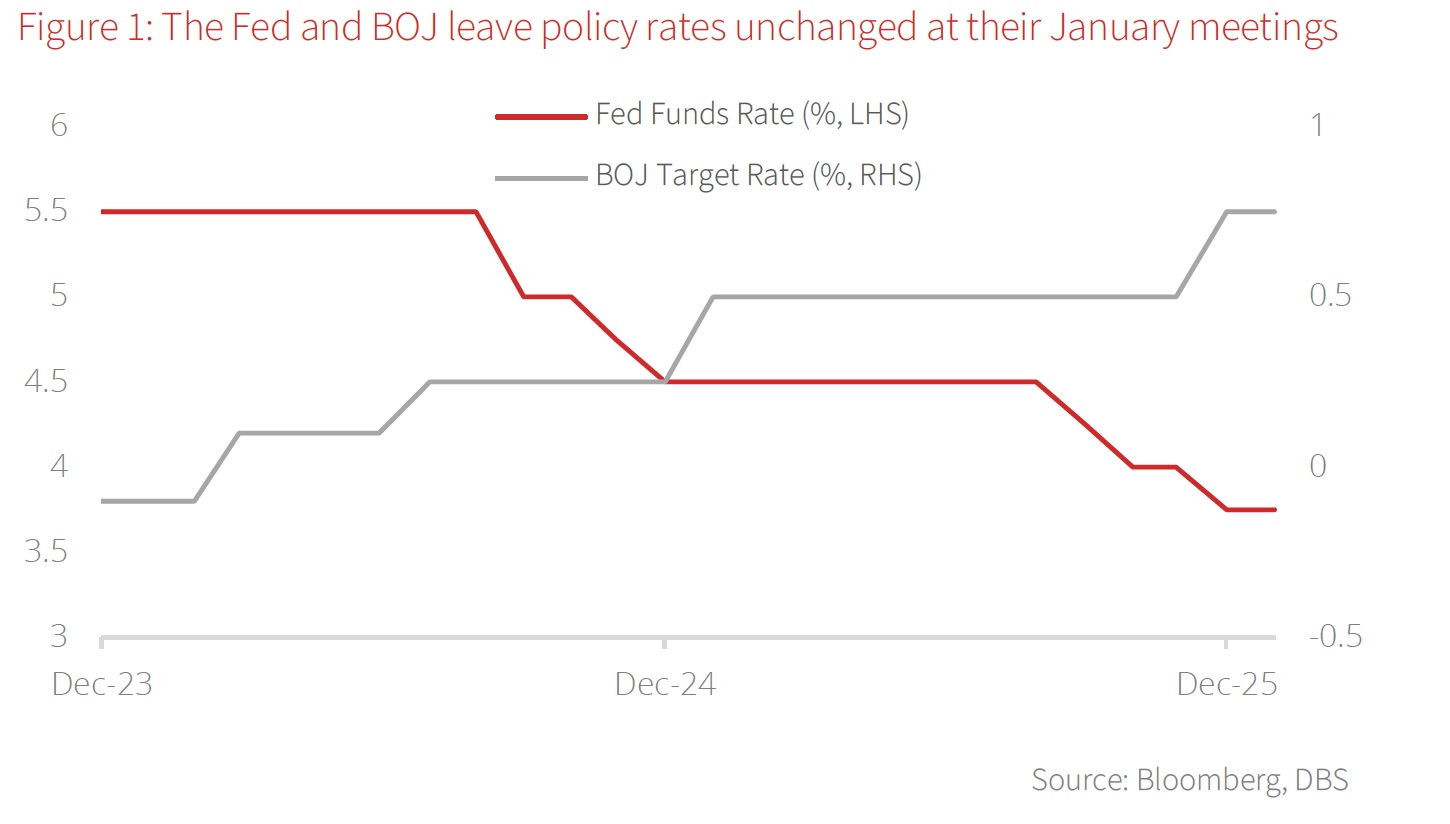

US & Japan: FOMC pause; BOJ policy dilemma. The US Federal Reserve’s Open Market Committee has chosen to leave the Fed Funds rate unchanged, marking the first pause in half a year. Having cut rates steadily, and with the economy now poised between rather strong growth, flattening inflation trends, and incipient but modest labour market weakness, Fed officials see little urgency to continue accommodations.

The market was well-placed to receive this communication and appears aligned with the Fed’s view that only additional data showing substantial labour market weakness would justify resuming rate cuts before mid-year. This is particularly the case as nominal wage growth continues to comfortably outpace inflation, while lingering risks to inflation remain (ranging from tariffs to a weak dollar, immigration tightness, and loose fiscal policy).

Political considerations are increasingly intertwined with Fed decision-making, with several legal matters still outstanding involving Fed Governor Cook and Chair Powell. We are looking for the US courts to assert Fed independence in their rulings, which we believe will be critical for Fed credibility and market perceptions on the outlook for inflation, fiscal policy, and the dollar.

Shifting to Japan, the Bank of Japan (BOJ) kept its policy rate unchanged at 0.75 at the 12 Jan meeting. On the economic outlook, the BOJ upgraded its growth forecasts, revising FY25 GDP growth to 0.9% from 0.7% and FY26 growth to 1.0% from 0.7%. Core-core CPI inflation forecasts were also revised higher to 3.0% from 2.8% for FY25 and to 2.2% from 2.0% for FY26. On the interest-rate outlook, Governor Ueda noted that wage hikes are exerting a growing influence on prices, and that April’s statistics will be a key factor in determining future rate hikes. In response to the surge in JGB yields, Ueda stated that the BOJ will conduct bond-market operations flexibly in exceptional cases to promote stable yield formation. On the weakening JPY, he added that exchange-rate movements may now have a greater impact on inflation than before and therefore warrant close monitoring.

The BOJ continues to view wage-inflation dynamics as the key determinant for further rate hikes. April looks to be the earliest plausible timing for the next hike, once initial results from the spring wage negotiations become available. However, the BOJ may choose to wait until June or July, when more comprehensive wage data are released. Rengo has publicly called for a 5% wage increase in the 2026 spring negotiations, following last year’s strong outcome of 5.25%. That said, firms are operating in a somewhat weaker profit environment, with corporate profits rising 6.5% y/y in 1Q-3Q25, down from 10% in 2024. As a result, final wage outcomes this year remain uncertain. We currently expect the BOJ to deliver the next 25 bps rate hike in July, raising the overnight call rate to 1.00%.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.