Related insights

A universal obsession. Few investment themes capture the imagination as powerfully as the pursuit of human longevity. A key obsession of mankind since historic times, it is emerging as one of the most consequential economic and technological frontiers of our time. The longevity economy with its multi-trillion-dollar market potential will see an increasingly rich and tangible investment opportunity set moving forward.

The longevity economy bifurcates into two distinct but interrelated opportunity sets:

- The pursuit of radical life extension: Encompassing frontier science and aimed at delaying, reversing, or altering the ageing process, this segment is more speculative in nature, but offers the greatest potential for innovation and growth, attracting investors seeking major breakthroughs.

- The implications of already-achieved longevity: Focused on the economic, healthcare, and social adjustments required to support populations that are living longer and healthier than ever before, this segment is firmly anchored in demographic certainty and existing expenditure patterns, unlike the moonshots of life extension.

Why now? With the longevity economy gaining momentum, we argue that today, it is at an inflection point for three reasons:

- Key technological breakthroughs. There has been a surge in medical innovations and breakthroughs in recent years. The once experimental gene editing tool, CRISPR, is now producing clinical results. CASGEVY, a gene therapy for sickle cell disease and beta thalassemia, was approved by the FDA in Dec 2023.

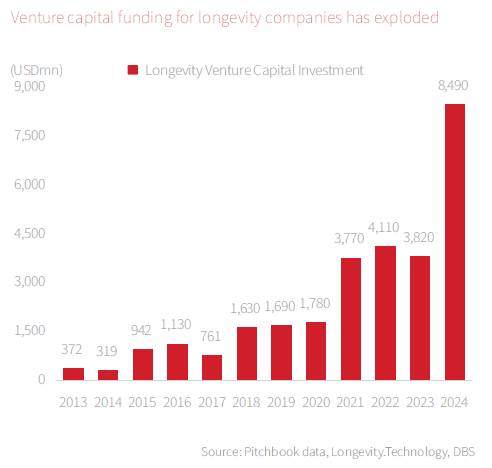

Diseases once thought to be incurable, such as Huntington’s disease, have also experienced significant advances in treatment. Huntington’s disease was successfully treated for the first time ever in Sep 2025 through novel gene therapy. These advances suggest that the science of anti-ageing is shifting from theory to application, and with it, speculation to investability. - Accelerating capital flows. Venture funding for longevity start-ups has surged, supported by dedicated longevity-focused funds and billionaire-backed foundations. Pitchbook estimates that the amount of longevity venture capital investment has increased by more than twentyfold from 2013 to 2024. This provides long-term funding necessary for high-risk, capital-intensive research development, and acts an anchor for other investors.

- Demographic tailwinds. Human life expectancy has risen sharply from around 40 years in 1900 to over 74 years today. This will not only drive rising expenditure to treat age-related ailments but also increase demands on healthcare and pension

From fringe to mainstream. This convergence of scientific progress, capital formation, and demographic inevitability creates a unique moment for investors. The longevity economy is no longer a niche curiosity; it is becoming a mainstream investment theme with both speculative upside and defensive ballast. In this chapter, we explore GLP-1 drugs and eldercare as demographic demand-side beneficiaries of longevity and gene therapy and cryogenics as longer-term prospects with both “moonshot” potential and more immediate applications.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.