- Higher-for-longer oil prices now almost a certainty

- Further oil price spikes possible in case of protracted negotiations scenario

- US shale oil plays remain well poised amid this environment, as they now prioritise efficiency over risky volume bets

- Expect rotational interest in the sector to revive

Related insights

- FX Tactical Ideas: Strengthening Positive Momentum for the USD19 Jun 2026

- Credit Strategy: Navigating the Warsh Era19 Jun 2026

- Research Library19 Jun 2026

Oil prices to stay elevated even if a resolution is reached. Under our base-case scenario of a near-term resolution to the US-Iran talks and reopening of the Strait of Hormuz within 2Q26, we expect market conditions to normalise only gradually. Clearing the Strait of Hormuz of mines could take up to six months after the conflict formally ends, and mine-clearing operations are unlikely to begin until a comprehensive deal is in place. Any residual risk is sufficient to prevent insurance markets from underwriting shipping through the Strait. Without this, commercial operators will not send vessels regardless of the political situation on the ground (ceasefire or deal). This means that even in our base scenario, the realistic timeline for full traffic normalisation has extended materially. We now think full normalisation of Strait of Hormuz traffic is realistically an end-2026 story rather than a next quarter story. Add to this, the production losses and reservoir damage in the Gulf countries, which are likely to persist even longer. Under such a scenario, we now expect Brent to average between USD85-90/bbl in 2026 (up from USD62-67/bbl forecast at the start of the year) and USD72-77/bbl in 2027 (up from USD65-70/bbl forecast).

US shale – stable beneficiaries of recurring geopolitical disruptions rather than rapid responders. The US shale industry has matured. Instead of materially lifting capex and aggressively drilling amid an oil price upturn, producers are trying to maximize returns from existing rigs through efficiency gains and tactical calls like lower hedging. Geopolitical shocks now channel more into higher free cash flow, buybacks and export monetisation than into runaway drilling growth. EOG Resources, for example, will re-allocate capital towards oil-heavy assets instead of increasing capex. Diamondback Energy was more constructive than peers on adding rigs but still limited itself to a modest 5% capex increase. Producers will also benefit from the structural surge in demand for alternative sources of LNG and natural gas liquids (byproducts of shale oil & gas) like ethane and LPG, with more volumes and long-term contracts likely to be inked for export markets.

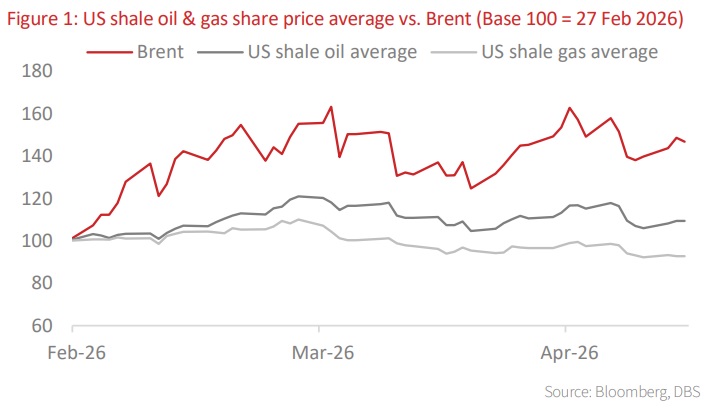

What is the market pricing in currently? US shale oil proxies present a cleaner play on elevated oil price environment than global oil majors yet share prices have only re-rated mildly (around 10%) since the crisis broke out. Compared to the 50% rise in oil prices, we think this is quite conservative, likely affected by flight of capital to the tech sector, where the AI theme continues to play out strongly, blocking out noise from elsewhere. We expect rotational interest in the energy space to revive sooner than later, especially if the US-Iran negotiations are extended even further and upside oil price risks are magnified.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- FX Tactical Ideas: Strengthening Positive Momentum for the USD19 Jun 2026

- Credit Strategy: Navigating the Warsh Era19 Jun 2026

- Research Library19 Jun 2026

Related insights

- FX Tactical Ideas: Strengthening Positive Momentum for the USD19 Jun 2026

- Credit Strategy: Navigating the Warsh Era19 Jun 2026

- Research Library19 Jun 2026