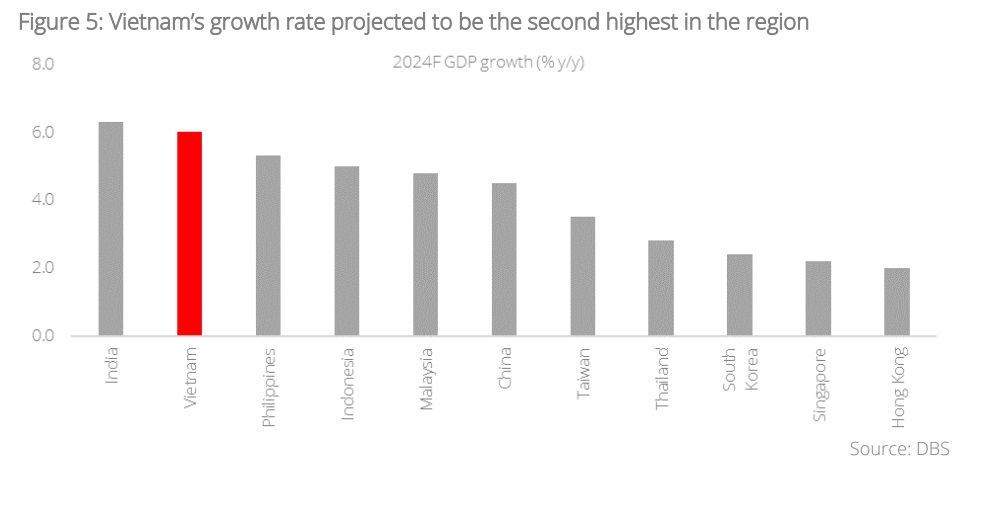

- Vietnam’s economy has been growing at 7% before the pandemic, and is expected to resume its growth path as it benefits from global supply chain diversification and the China+1 strategy

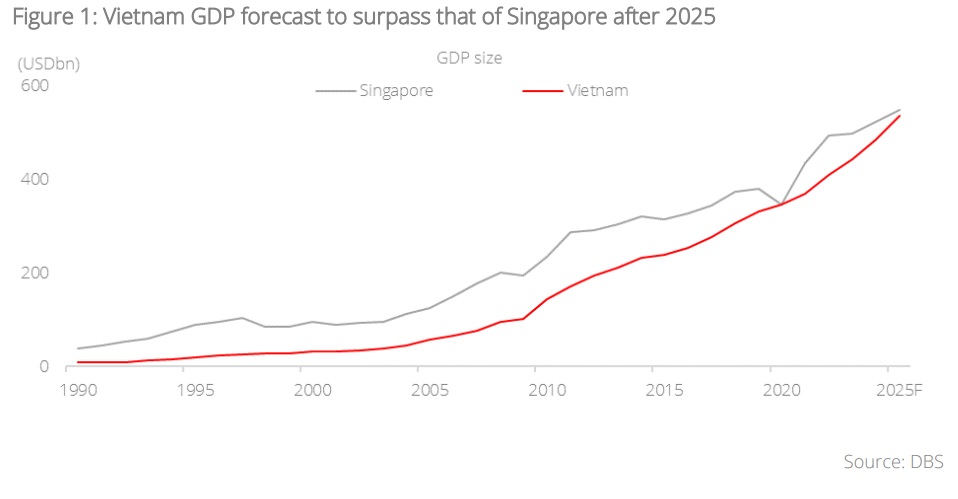

- Long-term prospects of Vietnam’s economy are positive after several reforms post crisis; it is expected to join the ranks of other countries in the region in terms of size and growth. Its GDP growth is next to India’s and size of the economy is catching up to Singapore’s.

- FTSE has placed Vietnam in a watchlist for a possible upgrade from Frontier to Secondary Emerging market status in the upcoming September review; Vietnam aims to be on MSCI’s watchlist by 2025

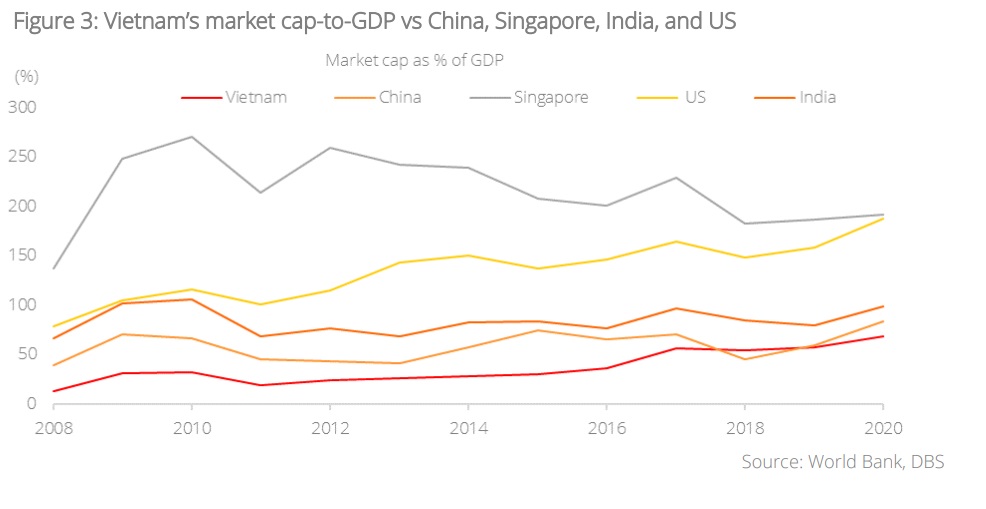

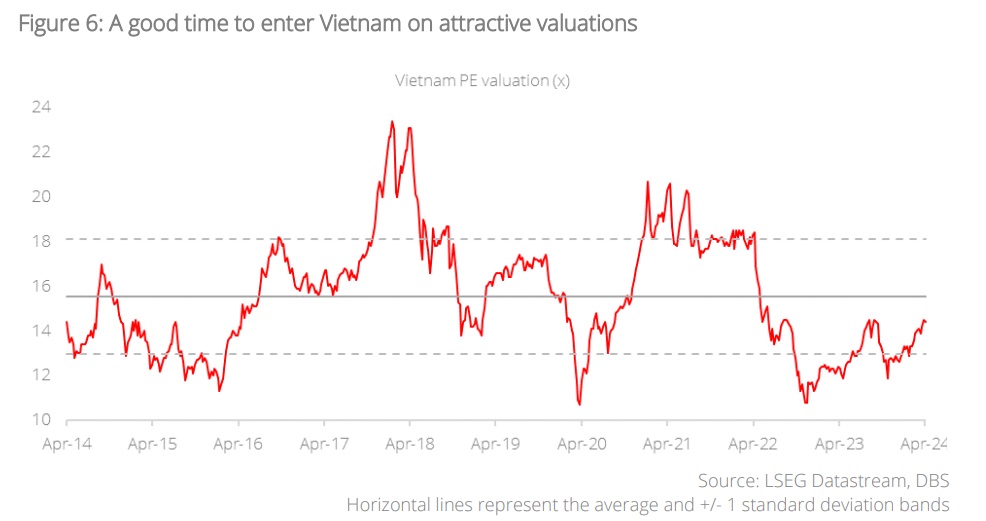

- Current low valuations and market cap to-GDP ratio make it a clear investment destination with high growth potential

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

Vietnam’s recent popularity as an investment destination continues to grow. Amid geopolitical tensions and as businesses adopt strategies aligned with China+1, Vietnam is believed to be in a good position to benefit from these supply chain shifts. In 2022, the country was a key recipient of foreign direct investments (FDI) to ASEAN, attaining an amount almost on par with Indonesia and Malaysia. Vietnam’s economy has been growing at an average of 7% in the five years before the pandemic, and its rapid growth is forecast to resume at 6% in 2024 and 6.8% in 2025. Vietnam’s GDP size briefly overtook that of Singapore’s in 2020, but on a sustainable basis, it looks set to overtake Singapore by 2025 after recording spectacular growth in the past few years.

Vietnam is not yet rated as an emerging market in global benchmarks. Vietnam currently has the largest country weight in the iShares MSCI Frontier 100 ETF (FM), at 30%. Investment opportunities are available as the government continues to move forward with market reforms. Though currently not yet classified as an emerging market under international benchmark standards, Vietnam’s capital market has been a strong contender where it comes to its global inclusion within the next few years, considering the country’s proactive market reforms. Efforts include the continuous part privatisation of state-owned enterprises, removal of the 49% foreign-shareholding cap on public companies (other than industries deemed important to national security), easing of restrictions on strategic investors who want to buy at least 10% of a firm, and the introduction of legislation to manage the banking sector’s bad debts. These reforms should pave the way for the gradual liberalisation of the securities market to foreign investors who want to ride on its remarkable growth.

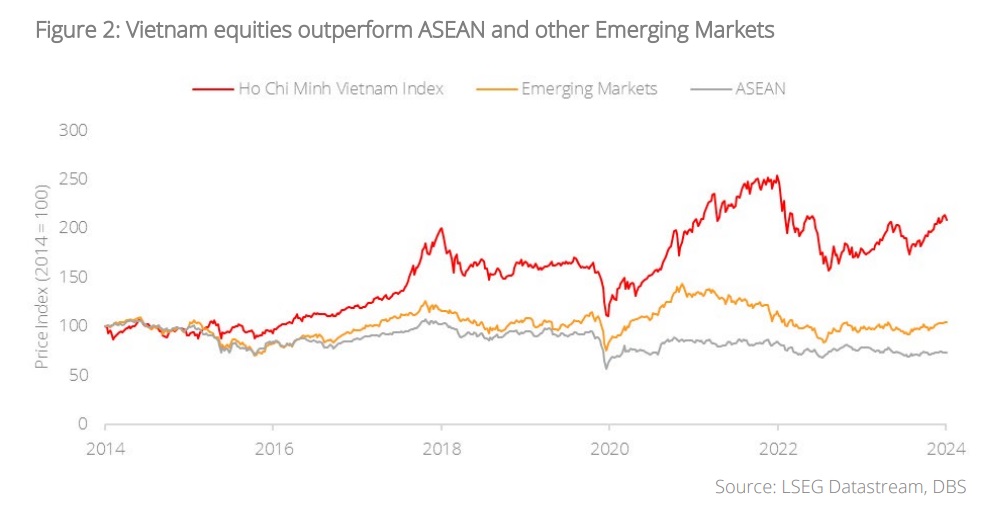

Stock market highlights. There are currently 399 listed companies on the Ho Chi Minh City Stock Exchange, the largest stock exchange in Vietnam. The VNINDEX (or Vietnam Ho Chi Minh Stock Index) reached an all-time high of 1536.45 in January 2022, and has been trading in a range of 1,000-1,300 in the past one year. It has proven to be more resilient than the MSCI ASEAN Index.

FTSE has placed Vietnam in the watchlist for a possible upgrade from Frontier to Secondary Emerging market status in the upcoming September review. The government has sped up work on the last few hurdles for consideration, which include the requirement for pre-funding, and an efficient mechanism to facilitate trading between non-domestic investors in securities that have reached, or are approaching, their foreign ownership limit. According to market reports, if successfully included in FTSE EM benchmark, Vietnam could attract about USD1.4bn inflows. It aims to be on MSCI’s watchlist by 2025, which should attract more flows.

Valuations are attractive. The Vietnam stock market is currently trading at 14.2x PE and 1.7x P/B. Vietnam’s market capitalisation is at USD266bn, which is equal to 0.7x of its GDP, making it a clear investment destination with high growth potential.

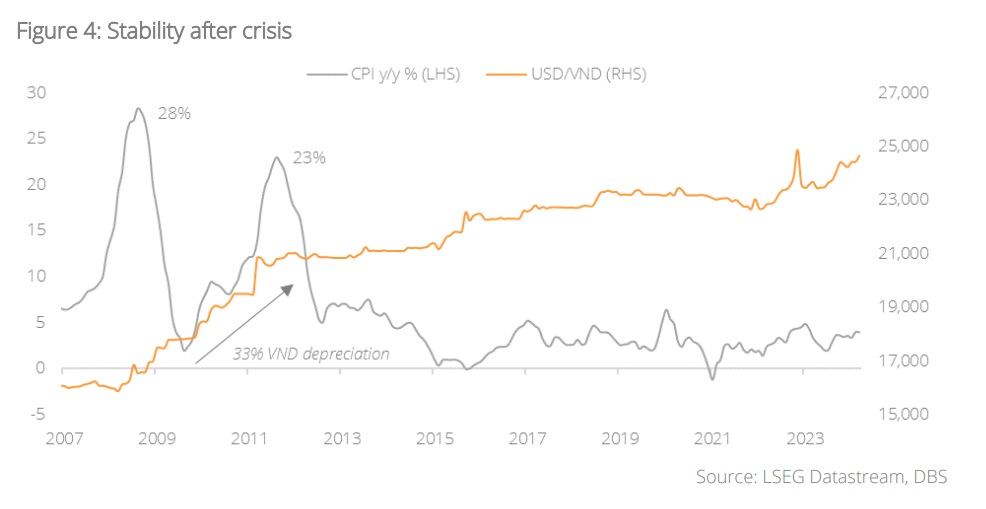

With crisis comes opportunities. Vietnam's growth trajectory has been marked by periods of both prosperity and downturn, mirroring its historical economic fluctuations and stock market performance. Following its economic opening in 2002, Vietnam grappled with formidable challenges, including soaring inflation rates, sluggish growth, significant devaluation of its currency (the VND), and the looming threat of a balance of payments crisis. The swift pace of liberalisation post-WTO accession, coupled with difficulties in managing internal imbalances and an overdependence on the US export market during the global financial crisis, exacerbated the economic turbulence during this period.

In 2022, Vietnam encountered its own property crisis after the real estate market enjoyed rapid expansion. The emergence of the pandemic shifted buyer sentiment from optimistic to cautious, and the situation deteriorated as Vietnam navigated the pandemic aftermath and grappled with economic fallout from the Russia-Ukraine conflict. However, unlike China, Vietnam's property sector was not heavily reliant on international borrowing, and the economy continued to attract significant FDI as a key beneficiary of China+1 strategy.

The continuous reform efforts undertaken by Vietnam following these crises have contributed significantly to shaping the country's current landscape. Vietnam continued its commitment to economic liberalisation and integration into the global economy, and is beginning to outperform many regional peers. Moreover, policymakers are now focusing on longer term economic stability and sustainability. The long-term prospects of this economy are positive, and in terms of the size and growth of the economy, Vietnam is expected to join the ranks of key economies in the region.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025