- Persistent strength in growth and sticky inflation signal that the path to lower rates may not be as straight forward as initially imagined

- Remain positive on bonds, but cautious with junk-rated debt and duration risks. Sweet spot remains with A/BBB credit in 3-5Y duration bucket

- Volatile yields and curve steepening given regime of fiscal dominance presents no compelling reason to take long-duration risk even on the brink of a cutting cycle

- Fiscal expansion/monetary contraction dichotomy to widen divergences across economic sectors. Stay with highest quality fixed income, although private sector strength could see selective candidates in BB+ segment become rising stars

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

It’s never this easy. It is especially tempting this year for bond investors to follow the simple prevailing narrative that one should just buy bonds when central banks cut rates. Yet the persistent strength in growth and sticky inflation should raise caution that the path to lower rates might not be as straightforward as initially imagined. This, we believe, is a complication worth untangling.

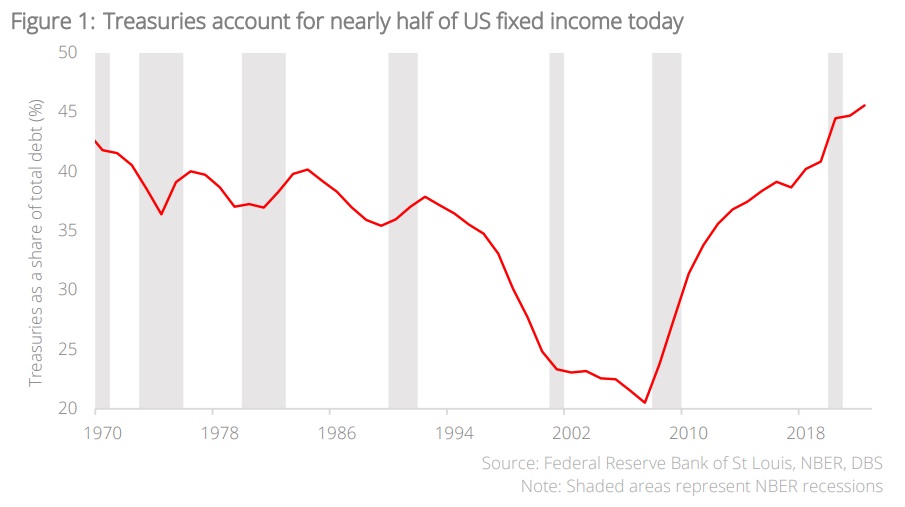

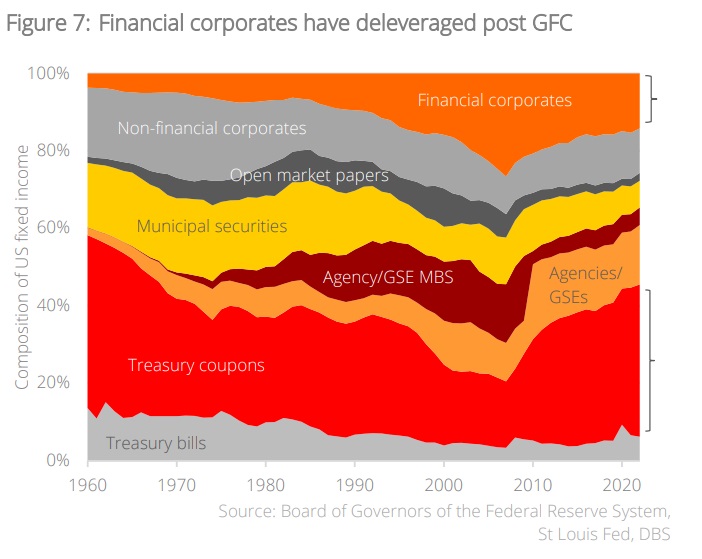

The era of big government (debt). Understanding it begins with an awareness of the shifting dynamics governing the supply-side of fixed income. Following the pandemic-era fiscal expansion, Treasuries have now reached a new record as a share of the fixed income market in the US – accounting for nearly half the total – despite the rapid development of the corporate credit markets since the turn of the millennium. As such, factors such as deficits, monetary policy, sovereign credit ratings, and central bank intervention have become as much, if not more crucial than corporate balance sheet strength and company earnings when devising fixed income strategy.

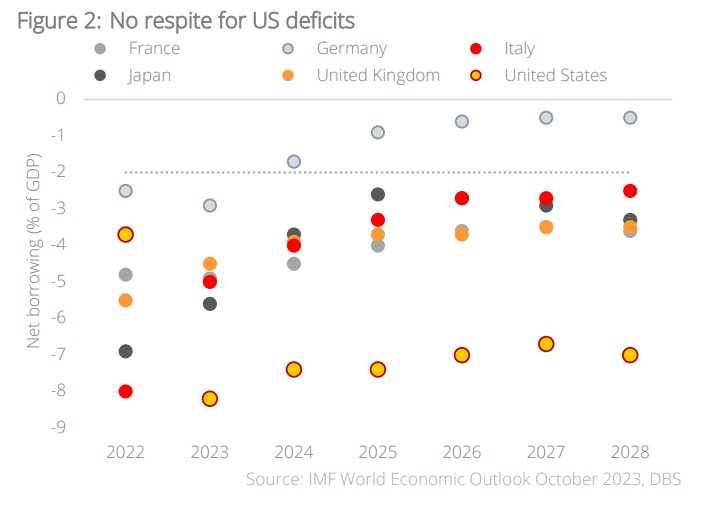

The great borrowing binge. This booming supply of US Treasuries is not surprising considering that US debt/GDP remains above 100%. What’s more surprising, is how tight monetary policy interacts with high debt to produce counterintuitive outcomes, a phenomenon we highlighted in our 4Q 2023 Global Credit outlook. Traditionally, high rates deter borrowing and money creation due to inhibitive costs of funding; but when the borrower is a price insensitive but indebted government – with mandatory spending needs such as social security, healthcare, and defence – high rates would pile onto the debt burden by raising the costs of interest servicing, resulting in a runaway train of never-ending government deficits. As such, while most developed nations are expected to reduce net borrowings in the years ahead, the IMF believes that US deficits would remain in the vicinity of 7% of GDP for much of the remainder of this decade.

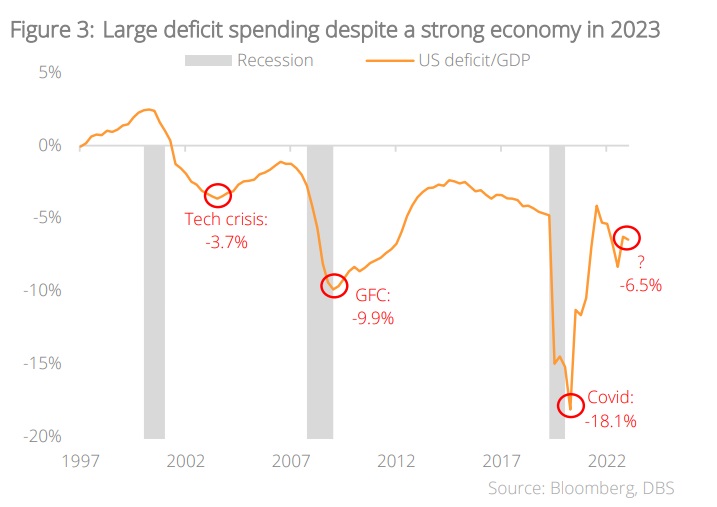

Spending beyond what is necessary. Consider how odd this situation is. Historically, the US had only embarked on deficit spending beyond 5% of GDP after a recession; logical, considering that countercyclical policy is needed to stimulate growth in a downturn. Yet in 2023 – a year characterised by strong growth and low unemployment – US deficits were 6.5% of GDP, an extravagance previously unheard of. We believe that this has played a large part in the persistent strength observed across economic indicators, complicating the path to slower growth and lower rates that was meant to catalyse the bond market recovery.

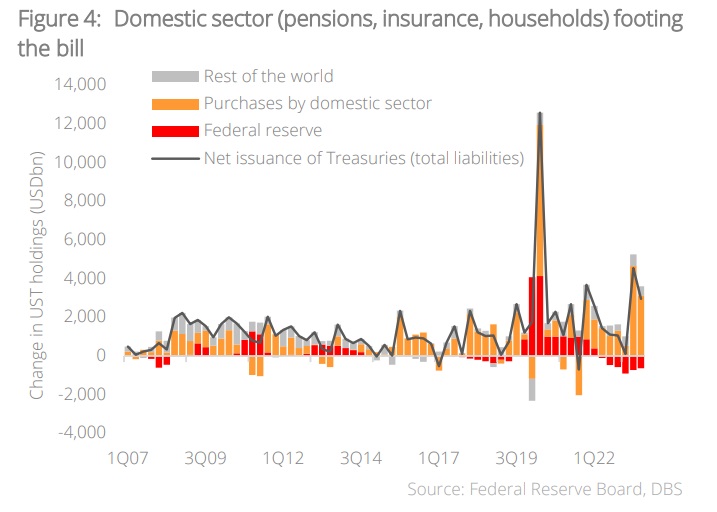

Who has been paying the bills? Such excessive deficits and Treasury issuances need equally excessive sponsors, but they aren’t your usual suspects of foreign reserves and central banks. Foreign participation in the US Treasury market has been on a steady decline since 2010; while the more recent (a) strength of the USD, (b) US sovereign ratings downgrade, and (c) deglobalisation narrative has left FX reserve managers more averse to US debt. Neither are the “buyers of last resort” in the previous crisis picking up the tab; the Fed and other global central banks are, on the contrary, busying themselves with unwinding their excessive balance sheets through QT.

The cash rich get richer. Looking at the data, the post-pandemic surge in net Treasury issuances has in fact been almost fully absorbed by the domestic sector – consisting of pension and mutual funds, insurance companies, and other household/corporate savings. This once again lends credence to the strength of US businesses and households; after all, the deficits of the public sector previously discussed are ultimately a surplus for the private sector. Moreover, these private sector savings are earning interest at the highest rates since 2008, resulting in a virtuous cycle of biblical allusion – “For whoever has will be given even more, and he will have an abundance”. We believe this public deficit-private surplus dichotomy to be a good lens to formulate credit strategy.

Dichotomies and divergences. In essence, this dichotomy of fiscal expansion (which is stimulative) and monetary contraction (which is inhibitive) would likely contribute to wider-than-normal divergences across economic sectors. Sectors that are direct or indirect recipients of fiscal handouts (e.g. businesses that rely on spending from the middle- and upperclass, or sectors with large surplus cash reserves such as Big Tech) would continue to thrive, while sectors that are most sensitive to high interest rates (e.g. commercial real estate, small banks) would continue to face further strain. From a credit standpoint, it is hence worth going through a thought exercise using this framework to highlight the potential winners/ losers under such a divergence.

Some potential winners include:

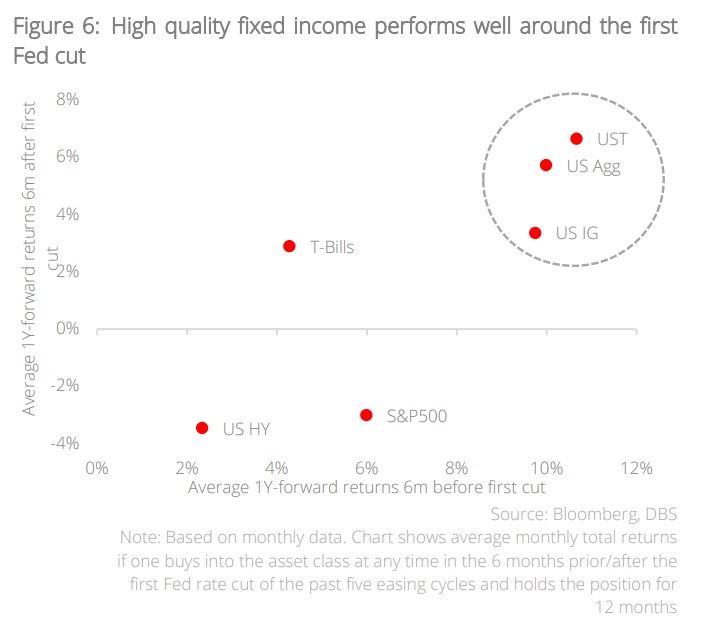

A. High quality issuers in the BBB/BB bucket. The corollary of a healthy business sector is the persistence of sanguine credit spreads. As such, we believe that fixed income investors are still better off with high-quality corporate credit due to (a) the spread premium over Treasuries, while also noting (b) more prudent financial discipline from corporates than governments in this cycle. Specific alpha opportunities could also exist for credit upgrades; a notable strategy being the picking of “fallen angels” (HY bonds in the BB+ category previously downgraded from IG) in anticipation of upside from spread compression. Investors need to be very selective, however, noting that it is only the highest quality fixed income that performs best in the vicinity of the first Fed cut after a hiking cycle.

B. Bank capital securities (IG). Seeing as spreads of financial capital instruments are still trading wide of their historical norms, it appears that the scars of the 2023 bank failures have not fully healed in the minds of investors. This we believe is an opportunity for savvy investors, noting that (a) surpluses in the corporate sector likely means fewer bad debt provisions are needed, while (b) the possibility of curve-steepening implies that high net interest margins can be maintained even in the face of rate cuts. Even so, many European banks maintain adequate capital buffers against regulatory requirements, which means that the sector remains in good health. However, we wish to highlight that more small bank failures could be ahead of us, given their concentrated exposure to the commercial real estate (CRE) sector. Investors should be selective, focusing on large banks that are solid IG names, with a preference for those with a diverse set of franchises across retail, institutional, and wealth businesses.

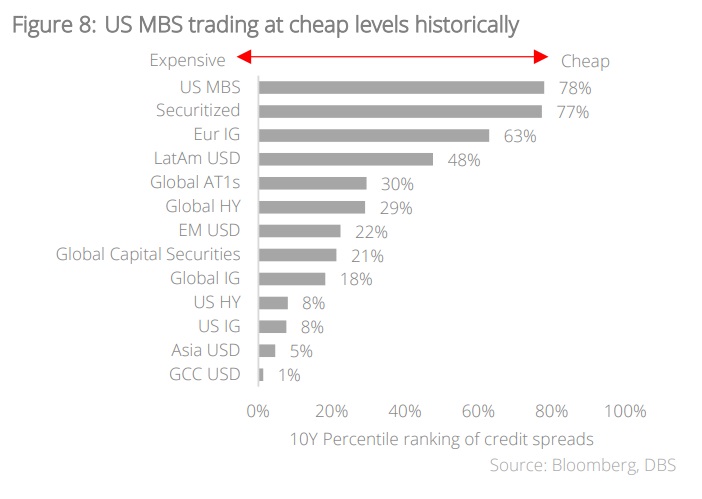

C. US Mortgage-backed Securities (MBS). We would be remiss not to mention one of the largest asset classes in the US bond market – agency MBS. Strong households would not default on their mortgages. Moreover, prepayment risk has declined as most US homeowners refinanced their mortgages in the low rates years of 2020-2021. At present, more than three-quarters of the index has coupon rates below 3.5%; homeowners would unlikely prepay these mortgages given the prevailing rates of c.7%. Even so, MBS spreads are trading at some of their cheapest levels in history, likely due to (a) the Fed running off their MBS holdings under QT, and (b) peripheral concerns on commercial MBS given the weakness in the CRE sector. We believe agency MBS to be the sweet spot, given their government backing and precedence as a Fed policy toolkit in times of severe distress.

Where we are cautious. Just as worthwhile is the endeavour to highlight where we see the most prominent credit risks in this dichotomy. As previously mentioned, sectors most sensitive to high rates would bear the brunt of monetary tightening. These include:

A. Junk-rated issuers. The strength of the private sector ultimately lies on a spectrum, and companies with weak balance sheets or interest coverage are unlikely to survive a higher-for-longer rates environment. HY issuers have much shorter-duration issuances, and the need to refinance over the next few years may present a stepwise shock to interest burdens, of which there are likely to be casualties.

B. Issuers in leverage-reliant sectors (Utilities, REITs). Similarly, issuers that have relied on higher leverage to improve equity returns under an era of lower interest rates would find their business models compromised in this new era. The structural weakness in the CRE space is symptomatic of this strain, where borrowers are more in the posture of asset disposal to shore up balance sheets than seeing debt-funded acquisitions.

C. Long duration bonds. The temptation, as always, is to take position in the bonds that have the highest beta to lower rates in a cutting cycle – long duration. Yet, bond investors need to be aware of certain technicalities regarding the financial plumbing around QT and Treasury issuances to make more informed decisions regarding this matter.

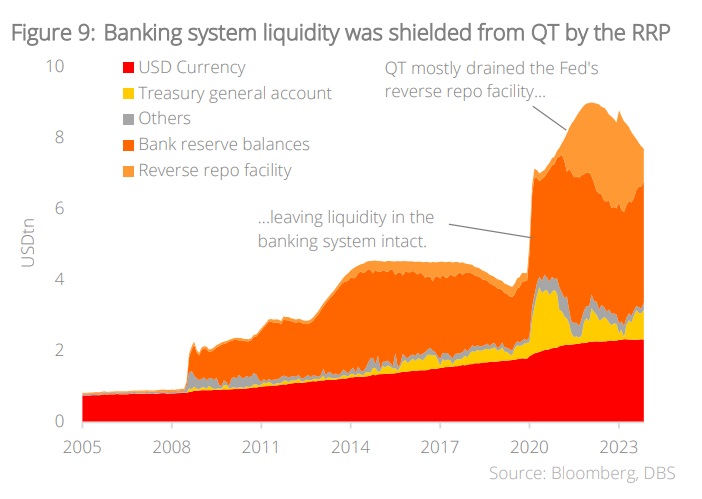

QT had a “shock absorber”. Banking system liquidity had remained unscathed since the start of QT in mid-2022 largely due to the presence of the Fed’s reverse repo facility (RRP), which shielded systemic liquidity from drawdown. This we believe has supported the functioning of Treasury markets thus far. This RRP facility is set to be drained by June 2024, and unless the Fed tapers QT, bank reserves could rapidly decline after, affecting systemic liquidity. We are cognizant that the 2019 repo crisis was caused by reserve balances dropping below viable levels in the previous QT cycle.

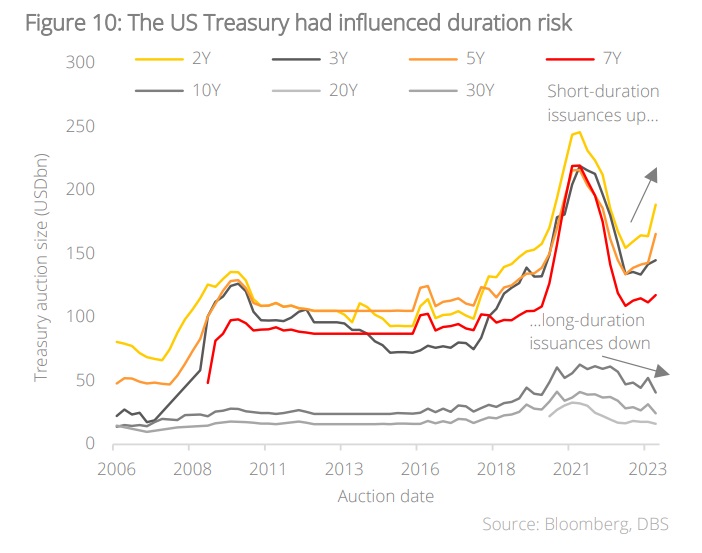

The Treasury has indirectly influenced monetary policy. Traditionally, the US Treasury had funded its deficits through the issuance of less than 20% of treasury debt in short-duration bills and the balance in long-duration notes and bonds. Since 2023 however, total Treasury issuances for bills are beyond the norm – a strange outcome considering that an inverted yield curve means shorter-duration bills are more costly than longer-duration bonds and notes. As such, the increased duration risk that QT supplies has been nullified by the reduced duration risk through Treasury issuances. This is unlikely to proceed further, given that bills as a proportion of total debt are reaching their recommended upper limits.

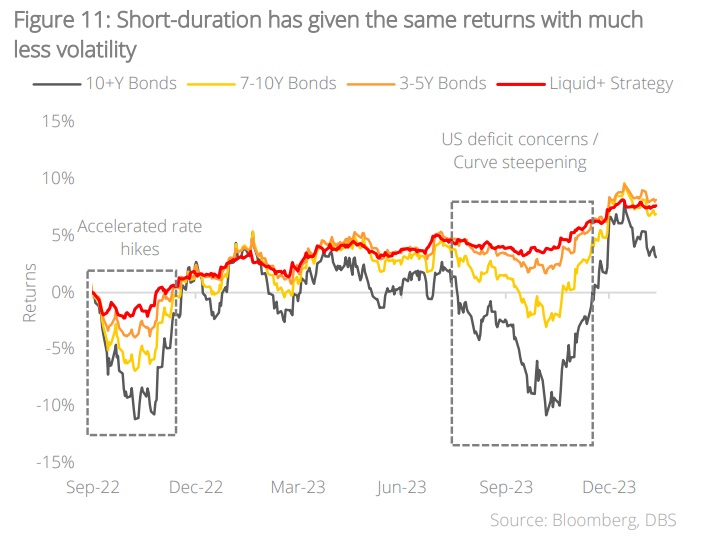

Our short-duration strategy remains relevant today. We had recommended a 3-5Y sweet spot for duration since 2022 noting this dichotomy of fiscal expansion/monetary contraction. Investors who have navigated the choppy waters of interest rate volatility since then would have recognised very similar returns with much less volatility. The Liquid+ strategy of even shorter-duration, high quality fixed income also fared relatively well in this regard. Given that this fiscal-monetary dichotomy remains at play, we find no compelling reason to take long-duration risk even at the brink of a cutting cycle.

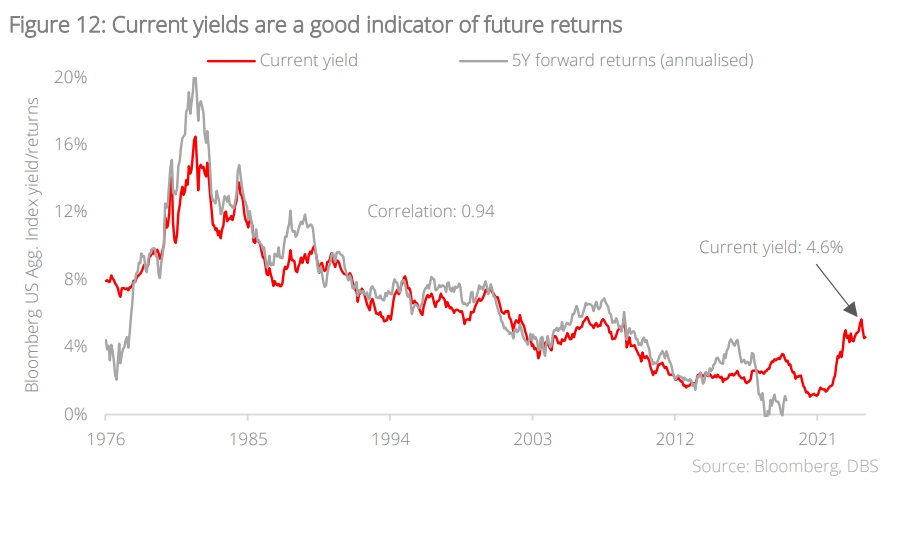

In summary, bond investors should remain positive on the asset class, but be selective with risks. Make no mistake, the high starting yields in bonds today are indicative of strong future returns. However, investors should remain cautious with junk-rated debt and duration risk. Opportunities are aplenty with IG credit, financial capital instruments, and MBS. The sweet spot remains with A/BBB credit, although selective candidates in the BB+ segment could become rising stars given the strength in the private sector. The 3-5Y duration bucket remains the best position against yield volatility and curve steepening under a regime of fiscal dominance.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025