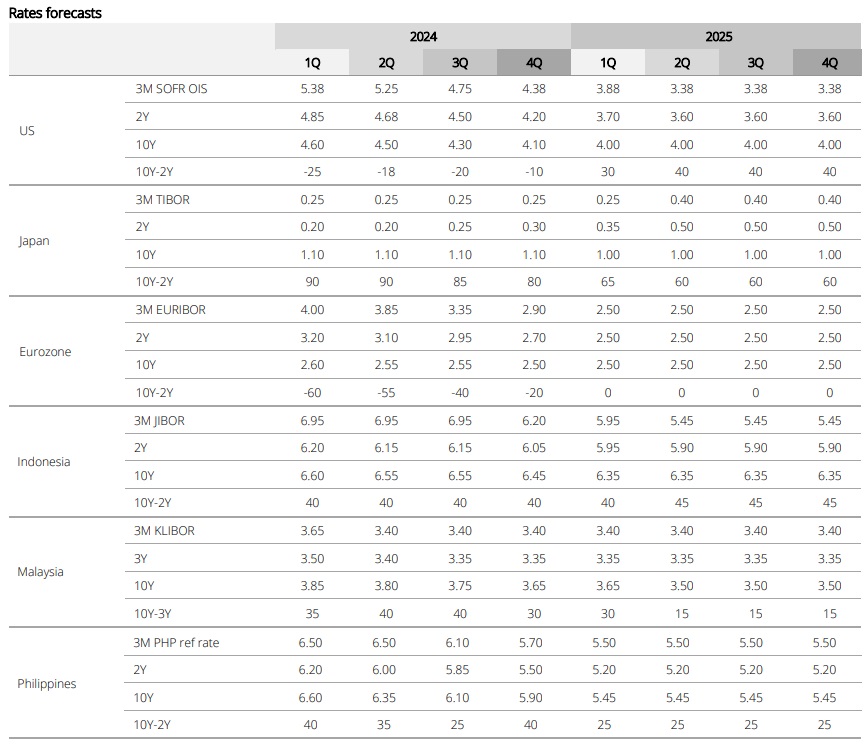

- Slower growth and moderate inflation will see G3 rates drifting lower and yield curves steepening

- Soft landing and gradual rate cuts to steepen yield curves in US and Europe

- Asia rates to remain steady as central banks await clearer signs from the Fed

- A policy shift in BOJ to lift JGB yields across the curve

- Amid firm US data and receding recession risks, expect both the Fed and MAS to stay on hold through mid-2024, keeping the 2Y SORA-SOFR spread relatively wide

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

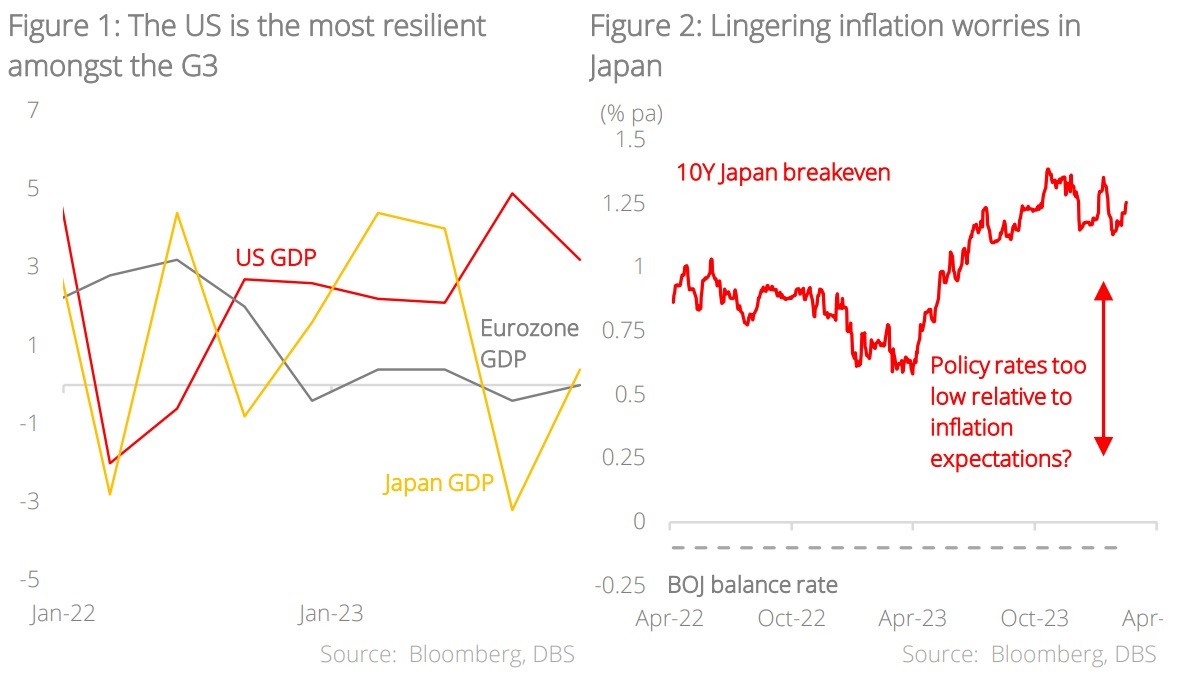

Nuanced resilience amongst the G3 economies has kept DM yields buoyant since the start of the year. In the US, market participants are struggling to price an appropriate Fed path. Between a perceived Fed pivot in December and a constant stream of data (payrolls as well as inflation) surprises on the upside, swings in 2Y yields can be significant. At the most dovish point in January, the market was pricing in more than six Fed cuts for the year. Amid firm data, easing bets have been pared with the market factoring about six cuts through 2025, in line with December’s dot plot. In the Eurozone, growth worries are more apparent with the economy entering stall speed in 2H. With inflation seemingly less of a problem and growth anemic, market speculation of European Central Bank (ECB) cutting earlier than the Fed has surfaced. Lastly, Japan’s economy barely skirted a recession in 2H23. However, we would not put that much weight on GDP figures and still see further Bank of Japan (BOJ) normalisation as likely.

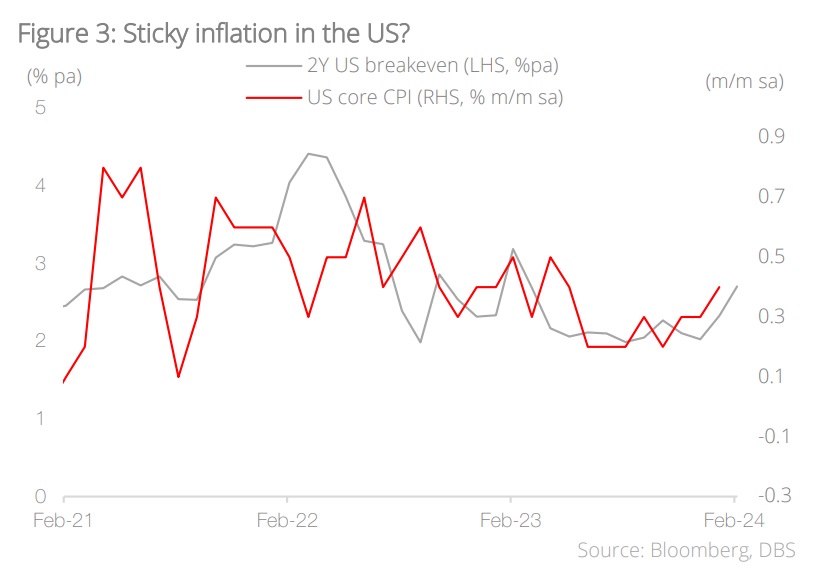

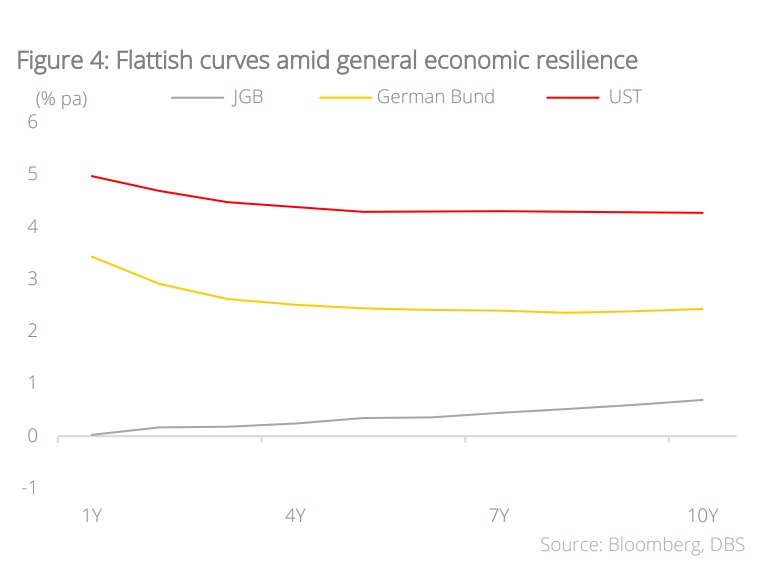

From an inflation standpoint, the US may be facing sticky price pressures. Headline y/y drifted towards 3%, with the core personal consumption expenditure (PCE) deflator running around 2% on a three-month annualised basis towards the last few months of 2023. This fueled hopes that with the price target hit, there would be room for the Fed to recalibrate rates lower even if the labour market stays strong. However, January’s data print shifted the narrative. Services inflation appears to be picking up along with core inflation. Combined with a firm labour market, conditions appear more similar to a no-landing scenario. Meanwhile, Japan’s breakevens indicate considerable worries about inflation even though the BOJ is clearly the most dovish central bank amongst the DM economies. Short-term term rates are still in negative territory while 10Y yields did not quite breach 1% even though the yield control curve (YCC) cap was turned into a reference rate. With January’s consumer price index (CPI) surprising on the upside, worries may build that the BOJ is behind the curve.

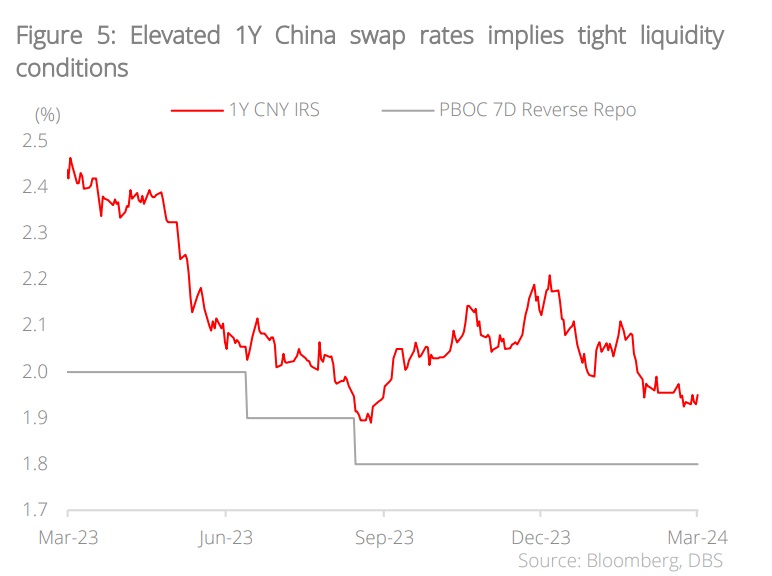

The rise in G3 yields from depressed levels in end-2023/early 2024 renders pricing more appropriate as they are no longer too low. Going forward, the verdict on the global economy is still unclear. Market pricing has swung between extreme optimism and pessimism several times over the past two years. In the absence of clarity, we are sticking to our soft-landing (slower growth, more moderate inflation) view and still see rates broadly drifting lower and Developed Markets (DM) curves steepening over the year.

Asia Rates

CNY rates: No cut ahead of the Fed

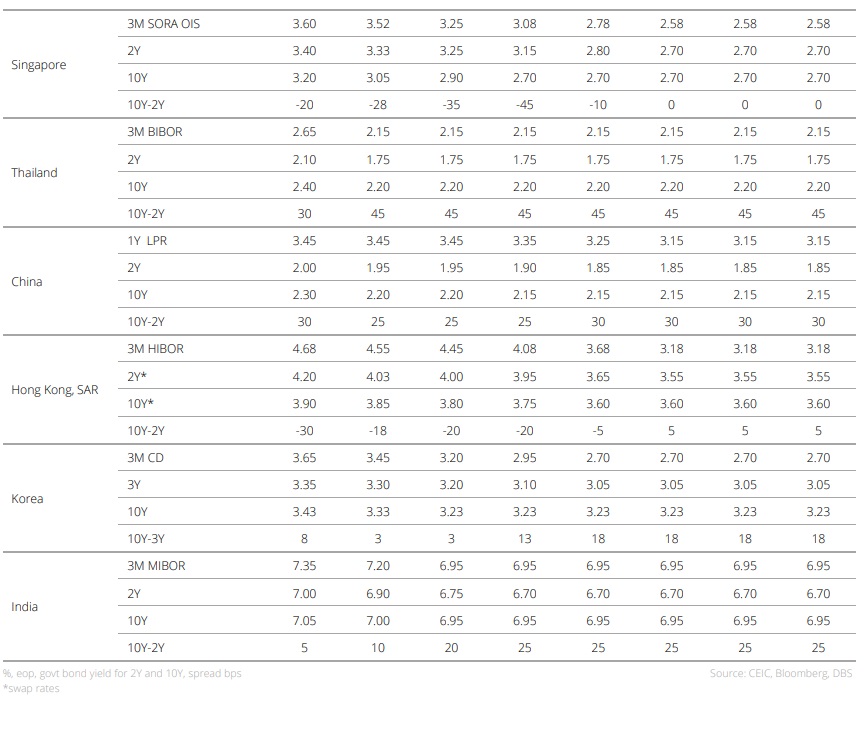

The sharp fall in 30Y CGB yields relative to 2Y and 10Y yields reflects the market pricing on urgent rate cuts. However, we think the authorities will likely keep the 1Y medium-term lending facilities’ (MLF) rate at 3.45% in the 1H24 before the first cut from the Fed. Of foremost concern, the People’s Bank of China (PBOC) aims at maintaining a stable CNY exchange rate to forestall capital outflow. Meanwhile, policymakers are waiting to discover the combined economic impact of previous policies. Over the past three months, the authorities have injected CNY1,017bn and CNY500bn through MLF and pledged supplementary lending (PSL) respectively. Additionally, the 50 bps RRR cut is expected to release another CNY1tn of liquidity into the system to offset the squeeze from special government bond issuance. The timing of the next rate cut will hinge crucially on the playout of economic data. January-February data was favourable, allowing the PBOC to refrain from rate cuts. Strategy-wise, we think China Government Bonds (CGB) yields will remain steady with downside bias.

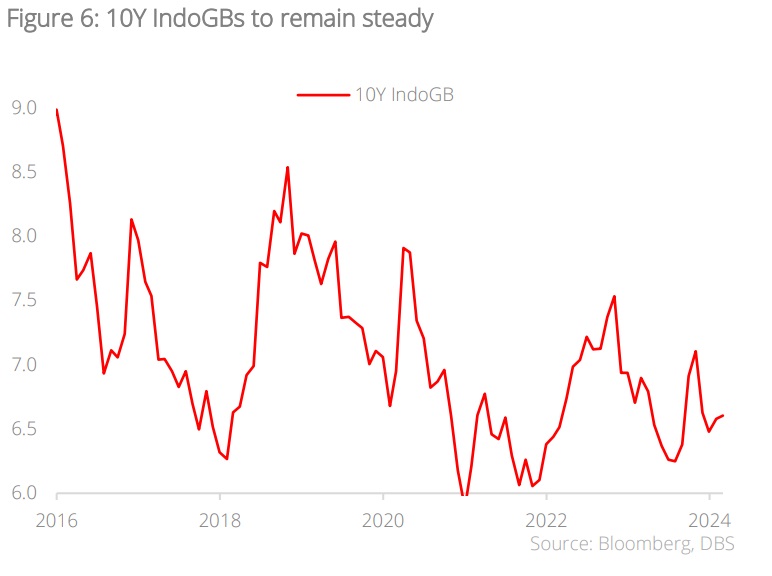

IDR rates: Stable yields on sound domestic economy

Bank Indonesia (BI) will likely keep the policy rate unchanged at 6.0% before cutting it to 5.25% in 4Q24. In other words, BI will not front-run the Fed cut due to a resilient domestic economy. The recent Presidential election laid the ground for stability and policy continuity. These include big-ticket infrastructure projects, moving up the commodity value chain, progress on the new capital, and continuation of social assistance programs, all of which point to a slightly wider fiscal deficit for the year. With inflation well within the central bank’s 1.5-3.5% range for the year, BI will be balancing external funding worries and the need to moderate upward pressure on IndoGB yields through periodic purchases. We expect IndoGBs yields to be broadly steady in the quarters ahead.

INR rates: Strong growth delays rate cuts

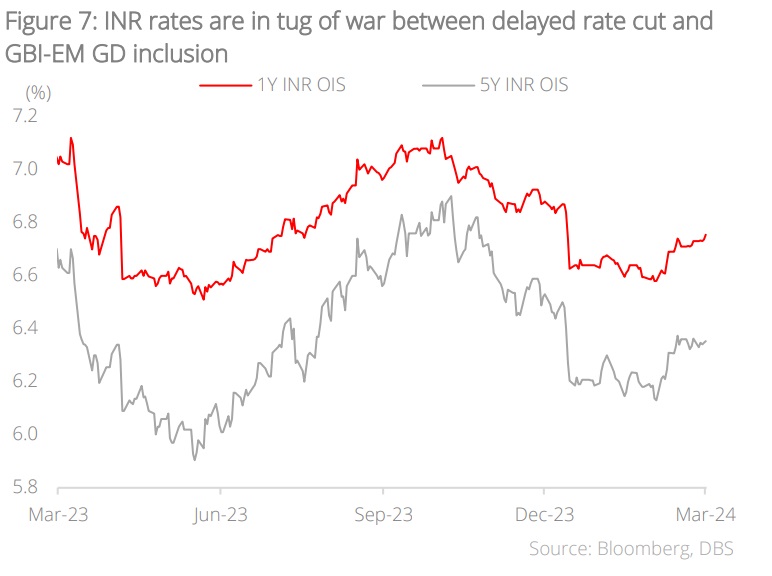

India’s relatively strong economic fundamentals leave room for the Monetary Policy Committee (MPC) to delay the timing of rate cuts. We anticipate a 50 bps cut to be implemented during the rest of the year, compared to our previous projection of a 100 bps cut. The MPC has revised the FY25 growth forecast upward to 7% from the earlier projection of 6.5%, citing the centre’s capex thrust, private sector witnessing second derivative benefits, and signs of pick up in rural demand on higher winter crop (rabi) sowing. On the external front, robust growth is evident in the narrowing current account deficit, primarily driven by rapidly expanding electronics shipments and services exports. Meanwhile, the authorities remain cautious about food inflation although core inflation is under control. Nonetheless, we continue to favour Indian government bonds (IGBs) due to noticeable capital inflows. Beyond rising foreign direct investment amid the “China+1” strategy, the inclusion of IGBs into the JP Morgan GBI-EM GD Index should keep INR rates at bay. The anticipated index inflows are substantial relative to India’s bond issuance sizes and external financing needs.

KRW rates: Mid-year cut

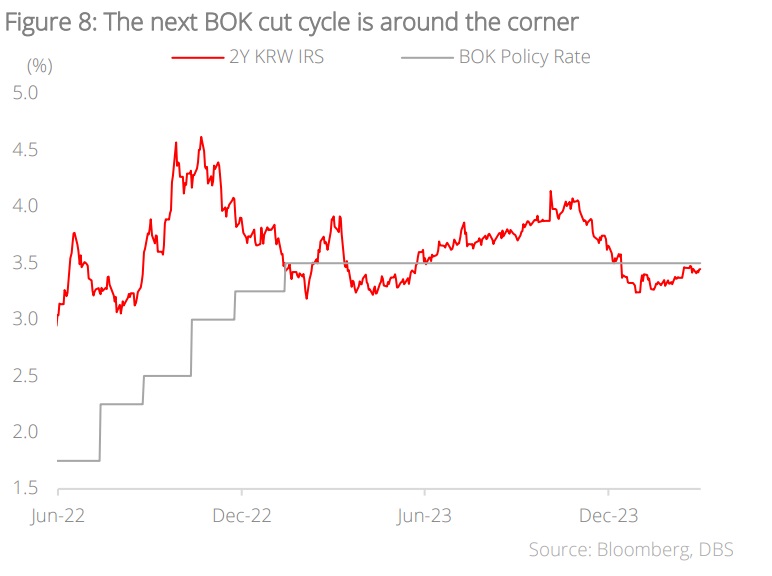

We maintain our view that the Bank of Korea (BOK) will pivot its policy stance ahead of the Fed and commence rate cuts in the middle of this year. Cuts totalling 75 bps are likely to take place this year. The softening economic fundamentals and receding inflation necessitate these rate cuts. Although the BOK met the 2024 GDP growth forecast of 2.1%, it revised downward the outlook for domestic demand, particularly private consumption. Consequently, the authorities adjusted the core CPI forecast down to 2.2% from the previous projection of 2.3%. In conjunction with other monetary stimulus measures, such as the expansion of SME lending support, short-end KRW rates are expected to see stronger downward pressure. Other bullish triggers include an increase in foreign inflows into tech stocks, and the prospect of KTB’s inclusion in FTSE Russell’s global bond index.

MYR rates: Rangebound for now

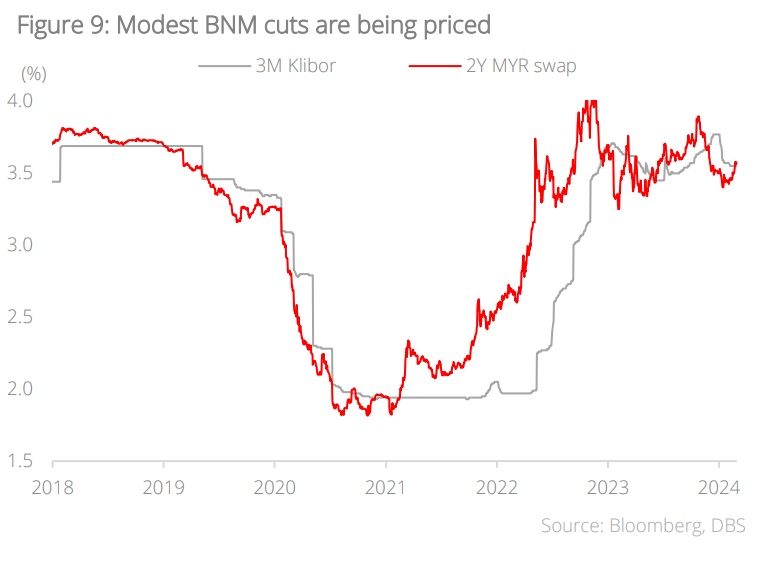

MYR rates and yields have been largely rangebound over the past few quarters as Bank Negara Malaysia (BNM) went on an extended pause. With USD rates cooling off from highs, MYR swaps are also flattish, pricing in modest rate cuts over the next two years. From an inflation front, we think that the prices have stabilised and no longer pose a threat to stability. Notably, headline and core CPI are both below 2% y/y in Dec 2023 and Jan 2024. With growth still somewhat on the low side (even with the continued rebound in tourism), we think that the case to cut will build in the coming quarters. Aside from inflation dynamics, the extent of fiscal consolidation this year bears watching. However, much of the savings from subsidy rationalisation would only show in 2H24, BNM may be inclined to watch fiscal dynamics before assessing if cuts are necessary.

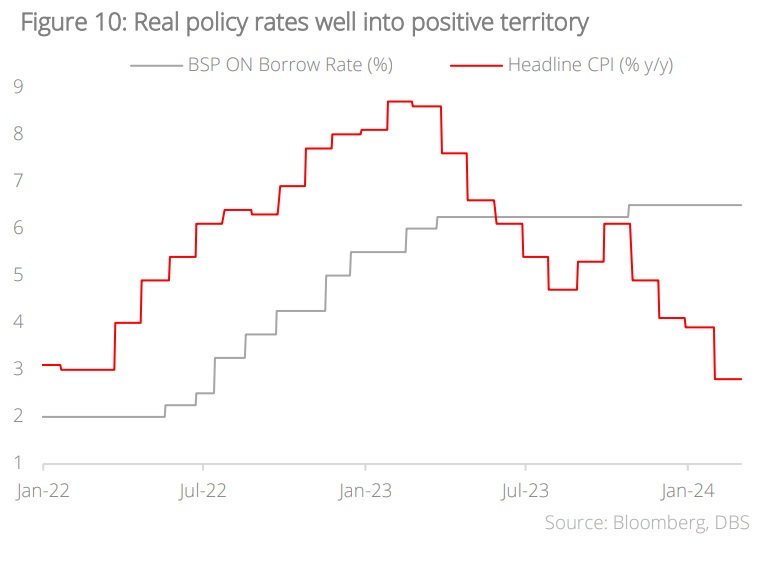

PHP rates: Aligning for less tight policy

Yields on Philippines Government Bonds (RPGB) have come off highs for the cycle and have been broadly rangebound over the past several quarters. The Bangko Sentral ng Pilipinas (BSP) has been one of the most aggressive central banks in Asia when it comes to tightening policy. Late last year, the BSP hiked after a prolonged pause amid pressure on the external front. Domestically, we think that conditions are aligning for less tight policy ahead. Headline and core CPI have dipped below 3% y/y and 4% y/y respectively in January. With the Reverse Repo Rate at 6.50%, real interest rates are now highly restrictive. With a tentative rebound in the trade balance and current account, there could be speculation of an earlier pivot from the BSP. Accordingly, we think that RPGB yields could well drift lower over the coming quarters.

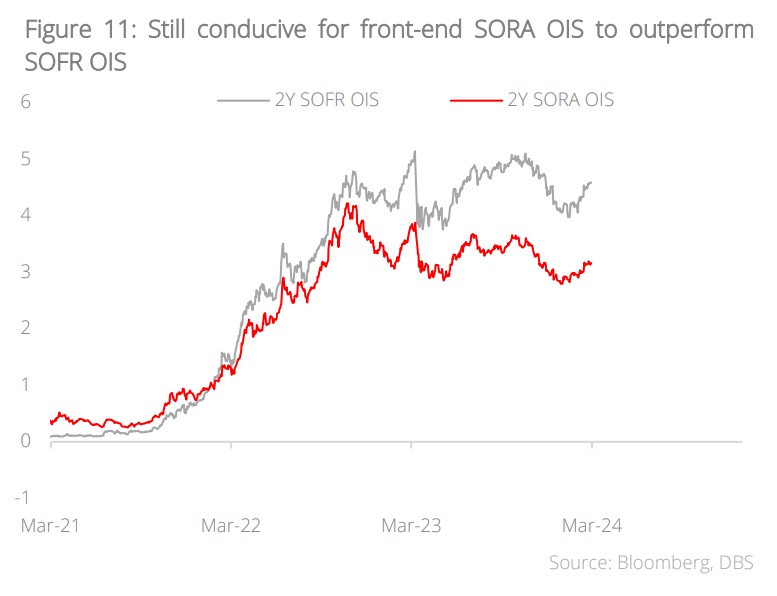

SGD rates: Sizable discount to USD rates for now

SORA OISs will continue to trade at a large discount relative to SOFR OISs in the near term. At this juncture, there should be minimal stresses in the rates space. Accordingly, the SORA-SOFR spread should reflect the estimated pace of appreciation in the SGD NEER. Arguably, this is clearest in the front of the curve where the market is still pricing in twin tightening (relatively high USD rates and a relatively steep SGD NEER slope). Further out the curve, as the Fed and the MAS normalises, it makes sense for the SORA discount to SOFR to reduce as the Fed cuts rates and the MAS reduces the slope at some point in future. Against a backdrop of rapidly shifting narratives, the 2Y SORA-SOFR spread has been volatile over the past few months. Amid firm US data and receding recession risks, we expect both the Fed and MAS to stay on hold through mid-2024, keeping the 2Y SORA-SOFR spread relatively wide.

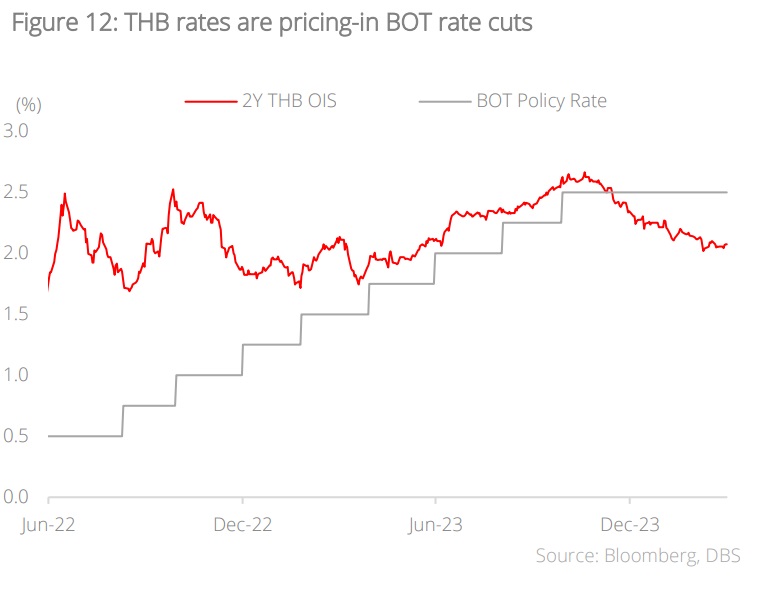

THB rates: Rate cut is imminent

We continue to see downward pressure on Thailand government bond yields. Although the Bank of Thailand (BOT) maintained its policy rate at 2.50% for the second consecutive decision, votes were not unanimous for the first time since 2022. Two out of seven Monetary Policy Committee (MPC) members favoured a 25 bps cut. This opens room for 50 bps cuts next quarter if economic data continue to disappoint. In fact, the BOT has already revised its 2024 growth and headline inflation forecasts downward to a range of 2.5-3.0% and close to 1%, respectively (from 3.2% and 2.0%). Constrained global demand and a delayed upturn in Thailand’s electronics cycle are expected to dampen Thailand’s export performance. Additionally, the multi-year-high real interest rate resulting from deflationary pressures justifies a rate cut ahead of the Federal Reserve’s.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025