- The latest developments in Japan ending their negative rate regime and US debt seeing rapid escalation are risks that we have been calling attention to since last year

- These developments continue to suggest a regime of diminishing demand and higher supply of US debt, which could lead to rising term premiums and steeper yield curves

- We continue to reaffirm the strategy to stay short-duration, against the more common inclination to take long-duration positioning in a rate-cutting cycle

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

Higher rates, higher debt. At long last, the world exits its last negative rate regime as Japan raises its policy rate – the first in 17 years – to a smidge above zero (0-0.1%). Equally, if not more significantly, the Bank of Japan (BOJ) abandoned yield curve control (YCC), leaving the door slightly ajar for market forces to influence the supply/demand of Japanese government bonds (JGBs). Across the Pacific, headlines around the US indebtedness continue to unnerve bond markets; the latest being that the US national debt is growing at about USD1tn nearly every 100 days. How are these two seemingly unrelated developments related to fixed income strategy?

The answer relates to demand and supply. On the demand side, the structural drift higher in Japan’s onshore yields and undemanding equity valuations would render domestic assets more attractive than those abroad, a risk we highlighted in early 2023. In other words, Mrs. Watanabe – the stereotypical term for retail Japanese yield-seekers – would no longer need to shop abroad for yields if onshore rates become much more desirable as Japan normalises policy. This is unfortunate news as Japanese investors are amongst the largest exporters of capital in the world. Particularly for US Treasuries, Japan as a nation is the single largest foreign holder of US debt, amounting to more than USD1.1tn at present.

It’s all about the debt. This could not come at a worse time as US debt supply continues its rapid ascent. This latest alarming spike of US debt above USD34.5tn should not surprise us any longer; we highlighted the mechanism of how high policy rates affect deficits last year, concluding that the trajectory of US debt was unsustainable.

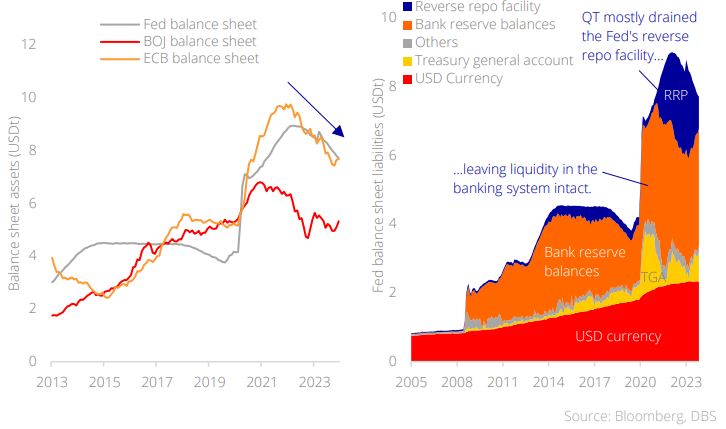

Why hasn’t QT affected liquidity? With this rising debt supply, one would have thought that the Fed’s quantitative tightening (QT) would have more rapidly drained liquidity in the system; yet financial conditions have remained comfortable thus far. Looking into the details, we see that banking system liquidity had remained unscathed since the start of QT in mid-2022 largely due to the presence of the Fed’s reverse repo facility (RRP), which has acted as a “shock absorber” shielding systemic liquidity from drawdown. This we believe has supported the functioning of treasury markets. This RRP facility is set to be drained by Jun 2024, exposing bank reserves to the full impact of QT which could impact systemic liquidity. We believe it is with this risk in view that the Fed had started to talk about tapering its balance sheet run-off in this recent March FOMC meeting.

Figure 1: Banking system liquidity was shielded from QT by the RRP

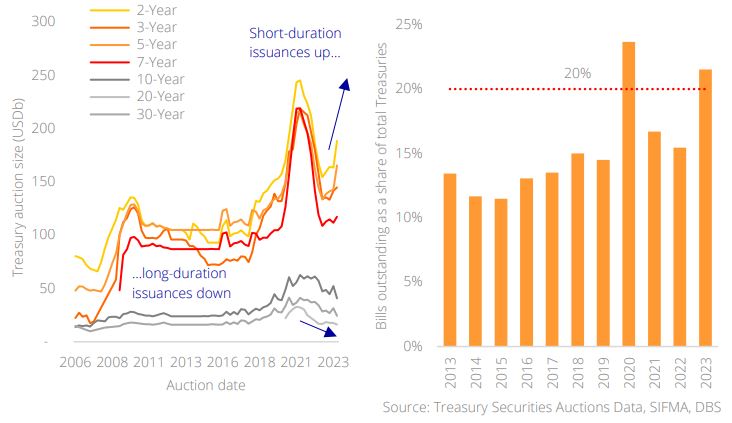

The Treasury has indirectly influenced monetary policy. Moreover, the US Treasury had also been quietly influencing the market’s exposure to duration in the background. Traditionally, the US Treasury had funded its deficits through the issuance of less than 20% in short-duration bills and the balance in long-duration notes and bonds. Since 2023 however, total Treasury issuances for bills are beyond the norm – a strange outcome considering that an inverted yield curve means shorter-duration bills are more costly than longer-duration bonds and notes. As such, the increased duration risk that QT supplies has been nullified by the reduced duration risk through Treasury issuances. This is unlikely to proceed further, given that bills as a proportion of total debt are reaching their recommended upper limits.

Figure 2: US Treasury has been funding the debt through issuing bills beyond the norm

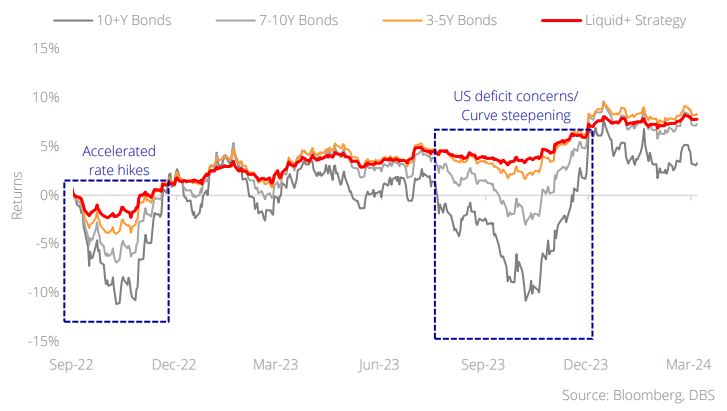

Staying short term for the long term. It was with these risks in mind that we had continued to reaffirm the strategy for fixed income investors to stay short duration to mitigate against rates volatility. The temptation, as always, is to take position in the bonds that have the highest beta to lower rates in a cutting cycle – long duration. Yet lower foreign demand and greater supply of Treasuries suggest that term premiums could rise and steepen the yield curve. Being aware of certain technicalities regarding the (a) financial plumbing around QT, (b) Treasury issuances, and (c) shifts in global demand allows one to make more informed decisions regarding this matter. Barring a clearer decline in the economic environment, we see no reason at this juncture – even in the face of rate cuts – to shift to a longer duration stance.

Figure 3: Short-duration strategies have stood the test of time

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

Related insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025